Don’t worry—we haven’t missed out on the bargains from the August 5 “flash crash.” We’ve still got a sweet setup for surging dividends in a sector most people completely misunderstand.

Misunderstood, unloved and soaring dividends? We’re interested!

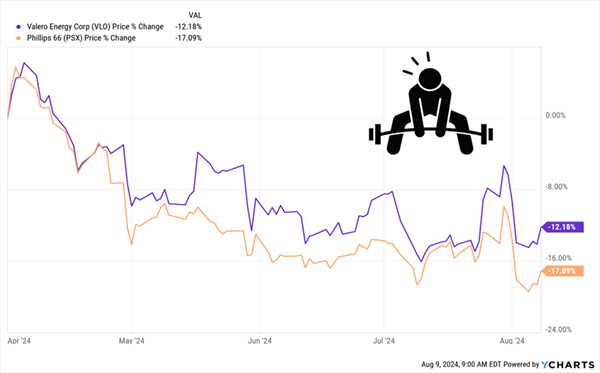

I’m talking about refinery stocks. We’re going to zero in on two of my favorites today: Phillips 66 (PSX) and Valero Energy Corp. (VLO). As you’ll see below, I like one more than the other in the market in front of us now.

I say refiners are misunderstood because most investors confuse them with energy producers, who drill for oil and natural gas, then sell the raw products.

Refiners buy that crude oil and turn it into gasoline, diesel fuel and heating fuel.

That “middleman” position puts them in a sweet spot now. Let’s rattle through the reasons why, starting with that August 5 market nosedive. Refiners—like pretty well everything else—tumbled, setting up another chance to buy them at a discount.

Refiners’ “Cruel Summer” Makes Them Overlooked Bargains

As you can see above, both VLO and PSX have only started to crawl back from the summer smackdown. And they’re far below where they were back in April, before the summer driving season started.

That’s important because between them, VLO and PSX hold a big slice of the gas-station market: Phillips, for example, has 7,500 stations operating under the Phillips 66, Conoco and 76 brands. VLO, too, has some 7,000 branded stations.

We don’t have the final numbers on the summer road-trip season yet, but we do know that it got off to a hot start. For the Memorial Day weekend, for example, AAA forecast the second-highest number of Americans hitting the road since 2000.

Reasonable gas prices—around $3.45 a gallon now, versus $3.82 a year ago, according to AAA—likely kept the cars rolling, especially as flying remains, generally, a nightmare.

Overdone Recession Fears Could Cap Refiners’ Costs

That’s the demand side—but what about costs? Crude oil is, after all, a major feedstock for refineries. Here too, we’ve got a nice “Goldilocks” setup, with crude trading around $76 a barrel as I write this, well below the $83 we saw just three weeks ago.

Overblown fears around a recession—especially when last week’s crash was mostly the result of gamblers who were short the surging Japanese yen—should put a near-term cap on oil prices, boosting refiners’ profits.

Now let’s talk dividends and upside, starting with our No. 2 refiner.

Valero Is a Smart Play on Our “Goldilocks” Refiner Setup …

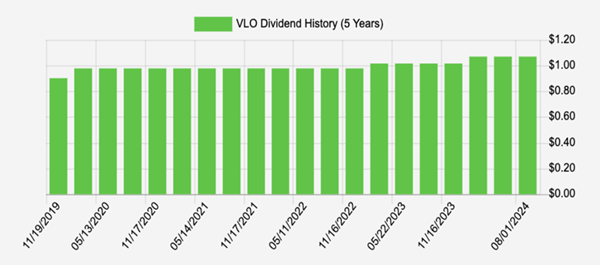

VLO, the third-biggest US refiner by market cap, is in second spot because, while it’s usually my “go to” stock in the space, it trails PSX on both current yield (2.8% for VLO, 3.4% for PSX) and dividend growth. As you can see below, VLO’s payout has slowed down of late:

Valero’s Payout Growth Downshifts

Source: Income Calendar

Historically, Valero was a rabid raiser—its payout popped 289% in the past 10 years! Most of that growth is in the past, however, with the divvie only up 19% in the past five.

That said, Valero is a big player—the third-largest refiner by market cap, behind Marathon Petroleum (MPC) and Phillips 66. These stocks tend to rally together and, if that happens, VLO, as always, will attract serious money. Regulators aren’t approving more refineries, and this blue chip already owns the “beachfront properties.”

… But PSX Is the Better Buy

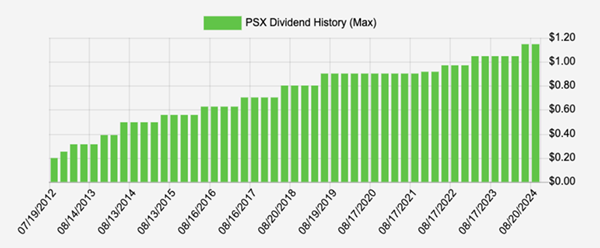

Meantime, PSX, which has 13 refining facilities that can process 1.9 million barrels of crude per day, sports a payout that’s jumped 28% in the past five years and 130% in the past 10.

PSX’s Helium-Powered Payout

Source: Income Calendar

Despite those more recent dividend hikes, the stock has trailed VLO this year and trades at just 11.6-times its last 12 months of earnings.

Eleven point six! In a world where the S&P 500 trades at 24-times earnings. The latest P/E is also way behind the 16.7-times earnings at which the stock has traded, on average, over the last five years.

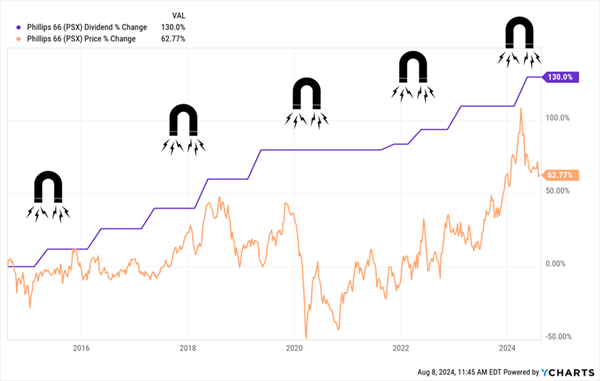

Then there’s the Dividend Magnet, or the tendency of share prices to track payouts higher over time. PSX’s payout/share price tie-up gives us yet another indication of just how cheap it is these days:

PSX’s Dividend Is Set to “Reel In” Its Stock Price

As you can see, PSX’s share price largely tracked its payout higher until late 2018 (when interest rates were rising). Then COVID kneecapped oil prices before the stock started grinding back toward its (surging) dividend.

The shares fell short again on renewed inflation worries in the spring. And now, thanks to last week’s crash, they’re still pinned down. That sets up the possibility of a double-digit pop, especially with rates primed to drop. (A possibility made even more likely by the disappointing August 2 jobs report, which many on Wall Street saw as the trigger of the early August crash.)

Moreover, the PSX shares, as we mentioned above, are still behind where they sat in April.

Finally, management is putting upward pressure on the stock through its buyback program: In the last decade, PSX repurchased a whopping 24% of its shares.

PSX Is a Perfect “Recession-Resistant” Buy. It’s Just the Start

If the early August market crash taught us anything, it’s that it won’t take much to trigger the next pullback—just another “so-so” economic report could do the trick.

When that drop comes, we’ll be ready to buy the deals on the other side. But we’re not waiting around for that to happen. Right now, we’re grabbing stocks like PSX, which are hideously undervalued (making it hard for them to get a lot cheaper in a downturn) and grow their payouts in any economy.

I’ve got 5 more “recession-resistant” bargains I see as even better buys than PSX now. Like our fave refiner, they’re cheap (so much so that I’m calling for 20%+ price upside in the next 12 months). Plus, their dividends aren’t only growing but accelerating.

My editor won’t give me the room to tell you about them in this article, so I’ve written a full investor briefing on these 5 picks you can access right here.

In addition to the full briefing on these 5 “ironclad” stocks, you’ll get to download a copy of a free Special Report revealing their names, tickers and my latest research on each one. Don’t miss this opportunity for fast-growing dividends—and price gains, too!

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Discover the 10 Best High-Yield Dividend Stocks for 2025 and secure reliable income in uncertain markets. Download the report now to identify top dividend payers and avoid common yield traps.

Get This Free Report