Look, I get it: many folks love ETFs, mainly because of the cheap management fees.

I mean who doesn’t love a deal? And it is true that ETFs’ fees are a fraction of those levied by the typical mutual fund or closed-end fund (CEF).

Trouble is, most ETF buyers get exactly what they pay for! Some of the worst performers in ETF-land are dividend-growth ETFs, which sound like a nice “1-click” way to load up your portfolio with soaring payouts.

Too bad they can’t stop tripping over their own feet!

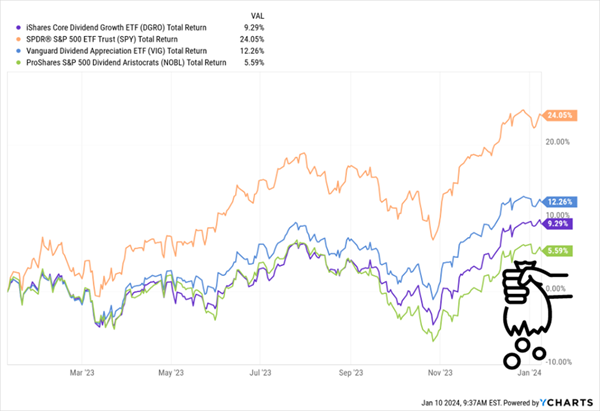

Look at how three major dividend-growth ETFs, the iShares Core Dividend Growth ETF (DGRO), Vanguard Dividend Appreciation ETF (VIG) and ProShares S&P 500 Dividend Aristocrats ETF (NOBL), have fared in the past year:

Stocks Lap Dividend-Growth ETFs

As you can see, the S&P 500 (in orange) blew past this trio, with a 24% total return.

The best our dividend-growth ETFs could do was the 12% posted by VIG, in blue above—just half the market’s gain! Particularly disappointing is NOBL, which holds the 67 S&P 500 “Dividend Aristocrats,” well-established stocks that have hiked payouts for 25 years or more.

No matter. NOBL staggered across the line with a sorry 5.6% gain. And it’s not like you’re getting big dividends for your trouble: VIG yields 1.9%, while DGRO pays 2.4%. NOBL is also a pauper, with its 2.1% payout.

Dividend-Growth ETFs Should Have a Built-In Advantage

This is particularly shocking when you consider that all these ETFs have an edge that should make them a shoo-in to top the market, and it’s right in their names: dividend growth. That’s because a rising payout is the No. 1 driver of price gains.

That might sound surprising, as most folks see dividends and share prices as different animals. But it comes down to the “stair-step” pattern of a rising payout, which pulls the share price higher at every turn.

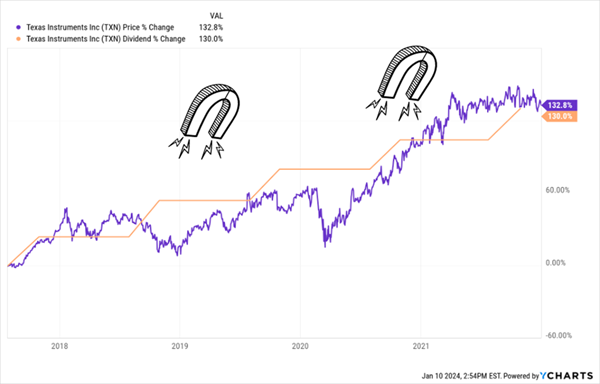

Consider Texas Instruments (TXN), which drops big payout hikes on the regular.

We held TXN in my Hidden Yields dividend-growth advisory up until January 2022. In that time, the payout popped 130%, pacing the share price to a 138% rise. The pattern is unmistakable:

TXN’s “Dividend Magnet” Powers Its Share Price …

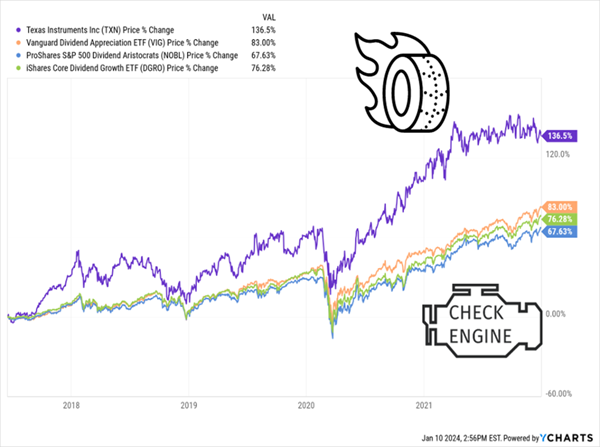

That, by the way, crushed our dividend-growth ETFs. It wasn’t even close!

…Which Demolishes Dividend-Growth ETFs

It’s a textbook example of why we look to individual stocks for strong returns. But this doesn’t mean our three ETFs are worthless—we can use them as a kind of “dividend roadmap,” sifting through their holdings to pluck out the fastest-growing payouts.

Let’s do that, drawing one ticker from each of these three ETFs. I’ve also ranked them from third to first, so you can easily see where the best value is:

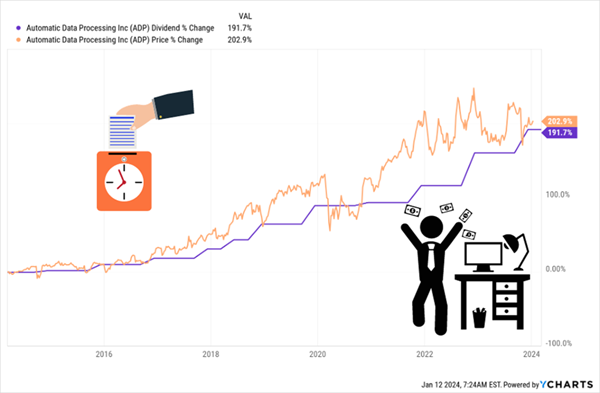

Dividend-Growth Pick No. 3: Automatic Data Processing (ADP)

Our bronze-medal pick, ADP, is the No. 10 holding of the ProShares S&P 500 Dividend Aristocrats ETF (NOBL). It’s a “near-double” Dividend Aristocrat, having hiked its payout for 49 years. As with Texas Instruments, this payroll manager has a share price that tracks its dividend higher, puppy dog–like:

ADP Cuts the Dividend “Paychecks,” Investors Buy More

The firm has come a long way from its founding in 1957, when it managed punch-card machines to track employee hours and printed the resulting paychecks. These days, its payroll software manages deductions automatically, including adjusting for tax changes.

It goes well beyond that, too, managing everything from recruitment and onboarding to benefits and retirement—essentially anything a business needs when it comes to dealing with employee compensation.

The beauty of this business model is that once a firm is in ADP’s ecosystem, it’s tough to leave—hence the company’s 92% retention rate. What’s more, the payroll-management market is fragmented, with ADP holding the biggest share at around 10%. That leaves it a lot of room to grow by acquisition.

Meantime, ADP is seeing strong revenue growth through retention, new business and higher interest rates on the payroll funds it holds for clients (which it invests in conservative assets, similar to an insurance company). Management is calling for 10% to 12% EPS growth in fiscal 2024. That, plus ADP’s 56% payout ratio, will keep the dividend popping.

So why is ADP our No. 3 pick? If we see a recession later this year, it would weigh on the share price, and I’m not sure that’s fully priced in, given ADP’s P/E of 28, just a touch below its five-year average of 31.

Dividend-Growth Pick No. 2: Chevron (CVX)

CVX, the No. 8 holding of the iShares Core Dividend Growth ETF (DGRO), is worth our attention because, as mentioned, oil stocks missed the party last year.

But that’s unlikely to last, for three reasons: continued strong consumer spending as inflation moderates; ongoing Mideast crises; and, as discussed last week, the need to refill the US Strategic Petroleum Reserve (SPR)—the nation’s “emergency stash” of oil—after the Biden Administration drew down nearly half of it to combat rising fuel prices.

Uncle Sam will drive up the goo’s price, though that’s unlikely to happen in an election year. Put this one down as a long-term catalyst.

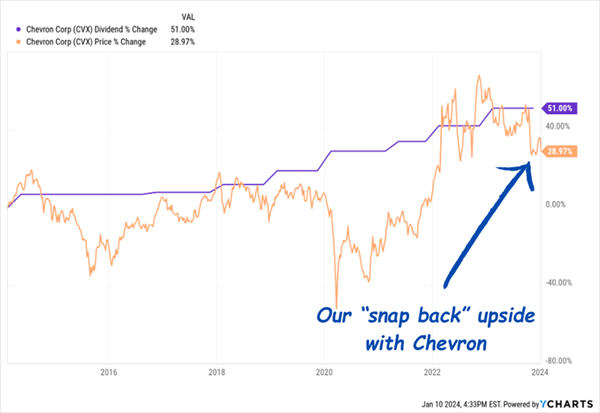

Moreover, CVX’s “Dividend Magnet” points to a bounce. As you can see below, the stock price bounces back above the dividend’s growth every time it falls off track, and we have another gap open now:

CVX’s “Dividend Gap” Points to Future Gains

Even if that bounce takes a while to materialize, CVX should get downside protection from its bargain forward P/E of 10.7. Moreover, the dividend only accounts for 44% of the last 12 months of earnings, so it’s safe.

Meantime, CVX continues to build on its position as the biggest player in US shale, including the biggest shale play of them all: the Permian Basin in Texas. CVX recently acquired PDC Energy, adding assets in the Permian and Colorado’s DJ Basin.

The only reason why CVX doesn’t take the crown? Its dividend growth—and by extension its Dividend Magnet—are a shadow of those of our “gold medal” pick.

Dividend-Growth Pick No. 1: Visa (V)

The demise of the (physical) greenback (thanks, COVID!) has been a boon to Visa, the No. 6 holding of the Vanguard Dividend Appreciation ETF (VIG).

The decline of paper money has sent more transactions flowing down Visa’s payment network. And the firm, which processes 60% of US credit-card transactions, takes a slice of each one.

Those all add up: Visa posted $33 billion of revenue in fiscal 2023, up 43% from 2019. And with US consumers still holding up as inflation (and soon interest rates) ebb, we can expect that to continue.

Meantime, Visa isn’t a bank—it just processes payments. That subtle, but critical, detail is the reason for the firm’s “ironclad” balance sheet, with $20 billion in long-term debt “cancelled out” by $20 billion in cash. That’s as spotless as it gets!

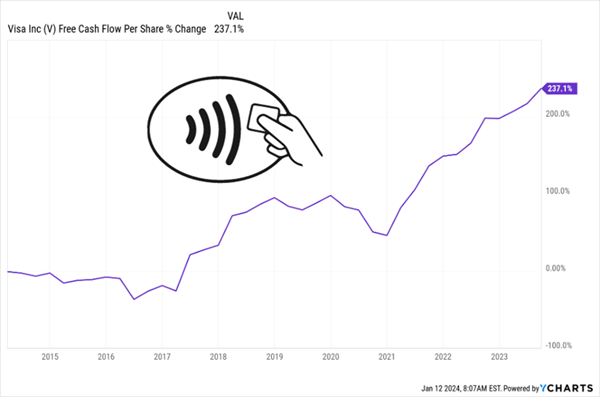

No wonder Visa is a cash cow, with free cash flow per share up 237% in a decade.

Millions of “Swipes” Add Up to a Cash-Flow Wave

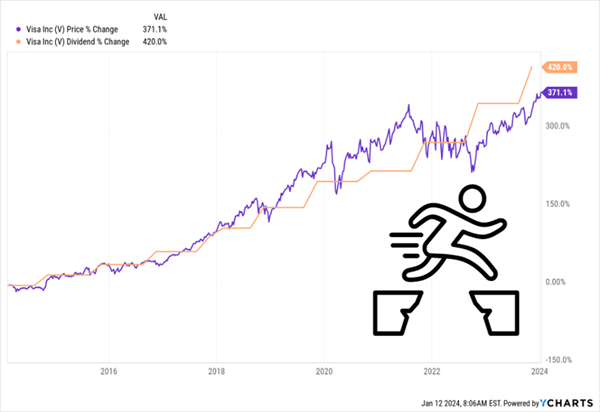

That’s boosted the payout 420% (ignore Visa’s 0.8% yield—dividend growth is where the party’s at). And as with Chevron, Visa’s stock has run ahead of its payout—until now:

Visa’s “Dividend Gap” Is a Buying Opportunity

That tells us that Visa is undervalued—and that can’t last as the firm grows revenue, thanks to the resilient economy. The topper: It’s extending its domination of “plastic” transactions to the growing number of “virtual” transfers, too.

5 Explosive “Dividend Magnet” Picks Set to Drop HUGE Payout Hikes in ’24

Dividend-growth ETFs are a perfect example of the outdated thinking we simply can’t afford in today’s market—which is unlike any we’ve lived through before.

Instead, let my “Dividend Magnet” strategy guide you to the TRUE hidden gems—those potent dividend growers with hidden advantages most people overlook.

I’ve got 5 such stocks waiting for you now. Each one, like Visa, Chevron and ADP above, boasts a soaring dividend payout that’s yanking its share prices higher. It’s a recipe for solid gains, and reliable, growing income, in ANY market.

Click here to get the full story on my Dividend Magnet strategy and download a FREE Special Report revealing my top 5 dividend growers for 2024.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Discover the 10 best stocks to own in Spring 2025, carefully selected for their growth potential amid market volatility. This exclusive report highlights top companies poised to thrive in uncertain economic conditions—download now to gain an investing edge.

Get This Free Report