Worried about the trade war and your retirement portfolio? Then I have two words for you: monthly dividends.

Today we’ll fawn over four monthly payers that yield up to 17.4% annually. That’s no typo. Hop in my favorite income vehicle and we’ll motor over this market carnage together.

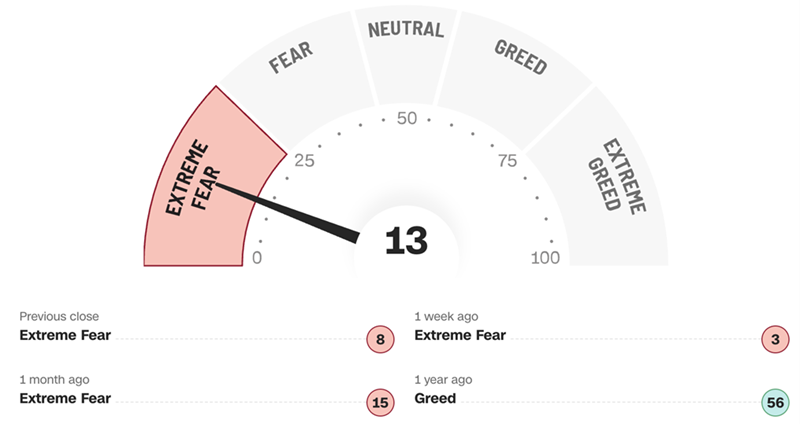

The current market environment is nearly perfect for contrarians like us. How is that possible with tariff policy still, ahem, unfolding? Well the market is still full of fear and the weak hands have washed out.

If Everyone Wants to Panic-Sell to Us, We Should Let Them!

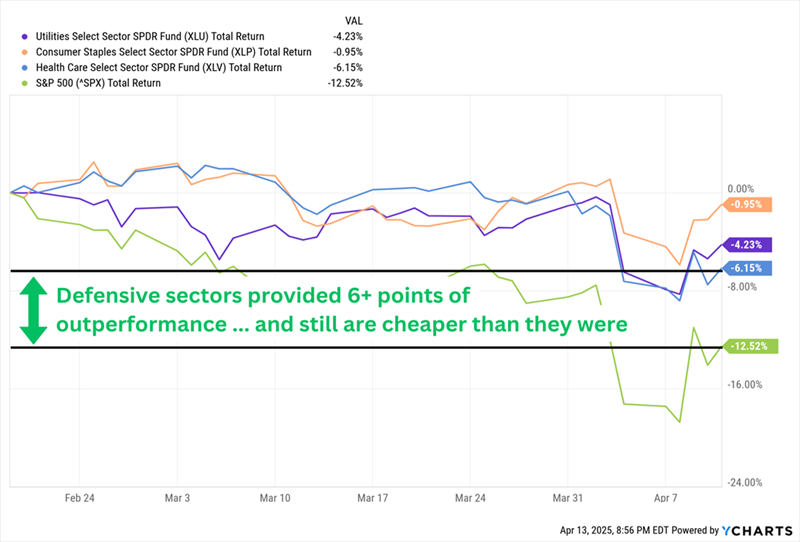

If you’re worried that the fear is justified because we are heading for a recession, let’s consider defensive stocks. They tend to be bear-resistant as their prices fall less than the market-at-large during a downdraft:

Health Care, Staples and Utilities Fell Less Than the Market

In other words: We contrarians should be looking to load up on anything that looks good in this environment, aggressive and defensive alike! That means buying more of the monthly dividends we already believe in, and looking for new opportunities.

Monthly dividend stocks have a number of qualities we want during market turbulence:

- They usually belong to specific high-yield categories, such as REITs, BDCs, and CEFs. That’s more income offsetting losses in a bear market.

- They pay more dividends more frequently, which means their income is more likely to buoy our portfolios when we need to see those returns the most.

- They often have a higher level of cash-flow stability that allows them to make those more frequent distributions.

I say “usually” and “often” because they don’t always sport these properties. Monthly dividend stocks need just as much due diligence as any other to make sure we’re not buying up portfolio time bombs.

Still, the relative strength and 5.6%-17.4% distributions of these four monthly dividend stocks are a great starting point. Let’s see how they stack up.

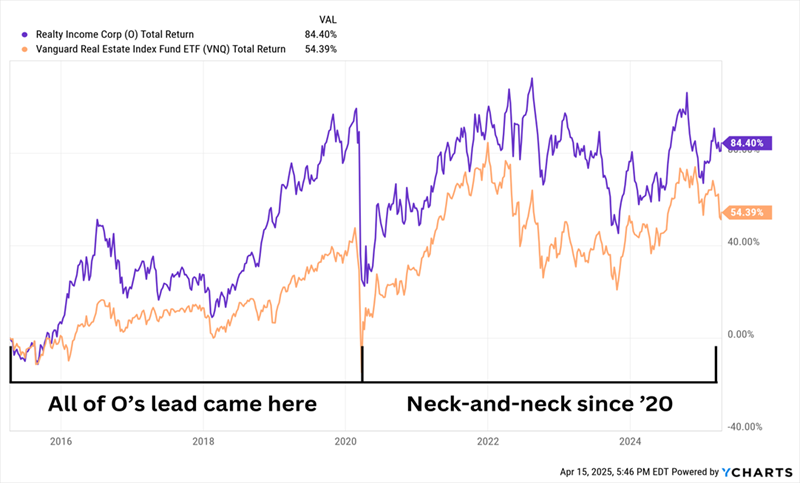

Realty Income (O)

Dividend Yield: 5.6%

Realty Income (O) is one of the bluest real estate blue chips—a $50 billion net-lease specialist with 15,600 commercial properties leased out to more than 1,500 clients in nearly 90 industries. It’s also increasingly an international player, with more than 500 of those properties spread across a half-dozen European nations.

A lot of that scale (of late) has come from large acquisitions, such as VEREIT in 2021, a large portfolio of properties from CIM Real Estate Finance Trust in 2023, and Spirit Realty Capital in 2024. But those acquisitions haven’t yet yielded much fruit for shareholders, who are sitting on a mere 5% cumulative total return in a rocky four years and merely par real estate performance since COVID.

Great Organization, But What Have You Done for Shareholders Lately?

It’s tough. On the one hand, Realty Income delivers a monthly dividend yielding nearly 6% (that it has raised for 110 consecutive quarters), has an extraordinarily diversified tenant base, enjoys the relative income stability of triple-net leases, boasts an outstanding balance sheet and, thanks to its scale, benefits from one of the best costs of capital in the space.

On the other hand, its growth in a good year is middling. And expectations for 2025 aren’t even middling—Realty Income’s own guidance for 2025 AFFO is $4.22-$4.28 per share, which represents just a 1.4% uptick at the midpoint.

If anything, Realty Income has held up too well this year. It’s flat since the Feb. 19 market high, with the recent dip all but evaporating. So we’re buying its yawn-worthy growth for 13 times AFFO estimates. Not ideal, at least for now.

Main Street Capital Corp. (MAIN)

Dividend Yield: 7.8%

Business development companies (BDCs) allow average investors like us to invest in private companies without having to pony up a million bucks. All we need is the money to cover at least a single share—often just $20 to $30.

The downside of the industry? It’s a dogfight. Financing risky small businesses is, well, risky; many BDCs have put up shoddy returns over time. In fact, it’s one industry I refuse to buy via funds because so many losers weigh down the winners. We just want the individual winners.

MAIN has long been one of those winners—a true blue chip in a niche industry with generally small market caps. At roughly $5 billion, it is one of the largest BDCs we’ll find.

Main Street’s primary investments are debt and equity capital solutions to lower-middle-market companies, as well as private loans to privately held companies. However, it also provides debt financing to middle-market firms and has an asset management advisory business. Its ideal portfolio company will generate revenues of between $25 million and $500 million annually, and EBITDA (earnings before interest, taxes, depreciation and amortization) of between $7.5 million and $50 million.

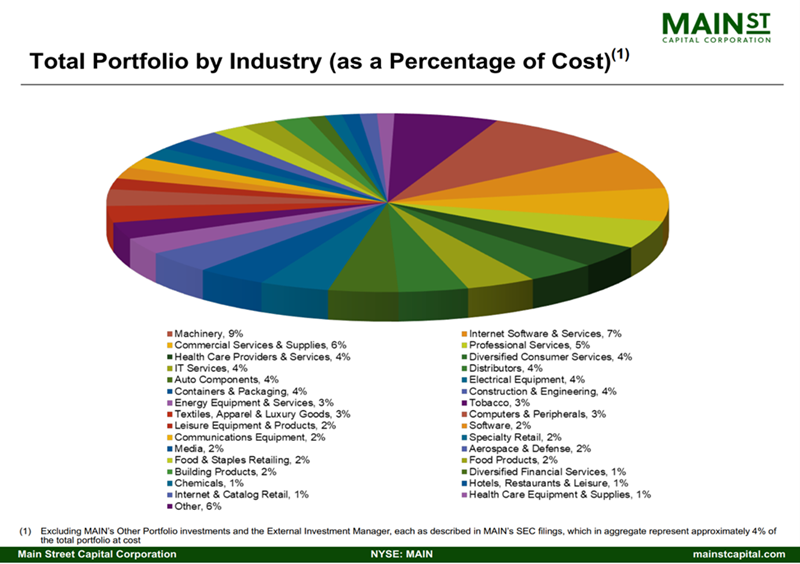

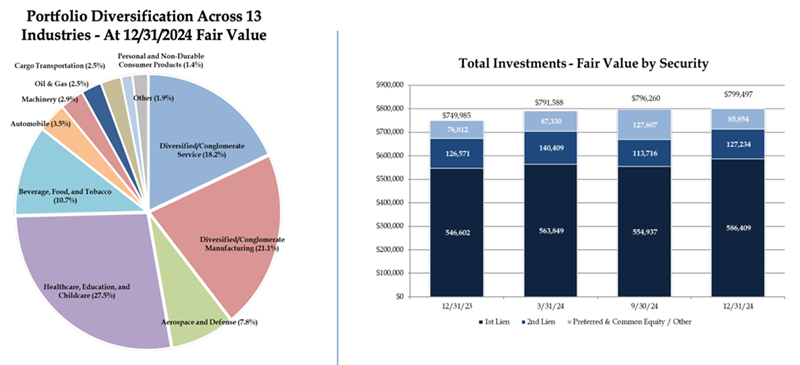

Portfolio breadth is high. MAIN currently is invested in 190 companies. Its largest holding represents just 3.8% of the total portfolio at fair value, and most investments are less than 1%. And those holdings are spread across several dozen industries, none of which make up more than 10% of the portfolio at cost.

MAIN Shareholders Enjoy Wide Exposure to the Small Business World

Source: Main Street Capital Corp. Q4 Investor Presentation

MAIN’s headline data gives us a lot to love. It has a nearly 8% dividend, 5.6 points of which come from its regular monthly distribution, and the rest of which comes from fairly regular quarterly specials—and both types of dividends have been on the rise. The stock historically clobbers the BDC industry, too; it’s not outperforming the pack by much in the current downturn, but it is ahead. Liquidity is usually strong, leverage tends to be conservative,

The issue with Main Street almost any time we look at it is that it’s laughably overpriced. Right now, it trades at a 70% (not a typo) premium to its net asset value (NAV), which makes it the most expensive BDC—by nearly 20 percentage points! I could argue that MAIN is always overpriced, but even by its own lofty standards, Main Street is priced for perfection.

But I’ll also point out that, at the moment, Main Street’s portfolio looks a little shaky. Non-accrual loans (not accruing interest because the loan is past due, usually by 90 days or more) are higher than the BDC average as a percent of the debt portfolio at both cost and fair value. This, heading into a potentially difficult economic environment, isn’t making me boil over with optimism.

Gladstone Capital Corp. (GLAD)

Dividend Yield: 9.7%

Gladstone Capital Corp. (GLAD) is one of the five investment funds that make up the Gladstone family of companies, all of which deal in alternative investments (namely real estate and private equity/debt). This particular Gladstone name is a business development company that invests in lower middle-market businesses.

Gladstone’s ideal portfolio companies generate $20 million to $150 million in annual revenues, $3 million to $25 million in annual EBITDA, have a proven business model, limited market and/or technology risk and a few other criteria. The BDC will provide financing in just about any way, too, though its primary focus is on first lien debt, which makes up roughly three-quarters of its portfolio.

That Preference for First Lien Debt Has Grown of Late, Too

Source: Gladstone Capital Q4 2024 Investor Presentation

The BDC industry spent much of the past couple of years in recovery mode once the Fed took its foot off the interest-rate pedal. But Gladstone stood out as one of the industry’s biggest winners, tripling the return of the VanEck BDC Income ETF (BIZD) and nearly doubling up the broader market. It’s deserved—Gladstone has been among the industry’s best in NAV-per-share growth and return on equity. A combined yield of nearly 10% (~8% regular monthly dividends, ~2% special dividends) furthers the appeal.

Understandably, GLAD had some froth to lose entering 2025, and it did. However, its drop into bear-market territory hasn’t been nearly so bad as other BDC names.

Despite the declines, Gladstone’s shares still aren’t a “bargain,” trading at a 14% premium to their net asset value. The company is one of the best operational performers in an industry peppered with duds, and its shares typically trade like it. However, Gladstone does tend to come back down to earth every so often, so let’s keep an eye on it. We might eventually be able to pick it up at a slight discount.

Dynex Capital (DX)

Dividend Yield: 17.4%

Dynex Capital (DX) is another REIT, but one that deals in “paper” real estate. It’s a mortgage real estate investment trust—one that invests almost exclusively (98%) in agency residential mortgage-backed securities (RMBSs).

Agency MBSes, which are issued by government-sponsored enterprises such as Freddie Mac, Fannie Mae and Ginnie Mae, are generally considered “safer” than non-agency mortgages, but they also generally pay lower rates. So, how does Dynex deliver a double-digit yield? In a word: leverage. Dynex closed out 2024 with leverage of 7.9x, which is simultaneously quite high and yet not too far above its historical average.

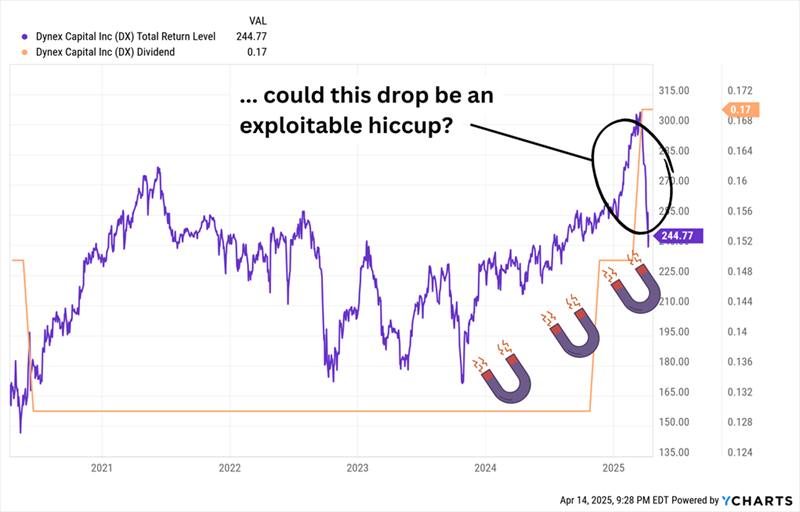

As I predicted in 2024, the steepening of the yield curve (that is, the gap between short- and long-term rates getting wider) over the past couple of years has been a boon for Dynex, which has made more of the environment than many other mREITs. I mentioned in December that Dynex finally reversed a history of dividend cuts with a 15% distribution hike, to 15 cents per share. And just a few months later, DX added another 13%, to 17 cents per share.

Shares have responded accordingly, right up until the tariff scare.

The Dividend Magnet Is Clearly Engaged, But …

An issue for DX from here is rate uncertainty, though most expectations have been for more rate cuts than previously expected for 2025. Generally speaking, that should benefit mREITs because it provides a lower cost of borrowing and could improve the mortgage lending environment, but it could also spark prepayments (primarily through refinancing).

The short-term dip has made it more appealing to would-be buyers, though, with DX now trading at roughly 10 times earnings estimates.

How to Collect a $48,000 “Portfolio Paycheck” When You Retire

The current market environment puts a giant spotlight on the importance of security—but fortunately, it also allows us to buy that security for less than we normally could!

I look to the best high-yielding monthly payers to offer that peace of mind because they can provide me with cash returns even if nothing else is working.

This recent slump has given me the perfect opportunity to stash away even more quality in my “8%+ Monthly Payer Portfolio”—a “who’s who” of companies and funds that check off the “3 H’s”:

- High yields

- High quality

- High durability

A lot of dividend portfolios try to offer up names that you know, and that you’re comfortable with. But Wall Street’s over-trodden blue chips tend to deliver relatively modest yields at high valuations … not to mention, they always pay quarterly.

My 8%+ Monthly Payer Portfolio is filled with names that many investors have (wrongly) slept on—despite kicking out 8%+ dividends that roll our way each and every month.

That dividend schedule means when you’re done collecting a regular workplace paycheck, you can quickly transition to collecting a regular “portfolio paycheck” of roughly $48,000 annually on just $600,000 invested—and that paycheck will still sync up with your monthly bills!

Don’t miss out on these terrific income plays while you can still get in at a bargain. Click here for details, including how to get a free Special Report revealing the names, tickers and research behind my favorite 8%+ monthly dividends.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Enter your email address and we'll send you MarketBeat's guide to investing in 5G and which 5G stocks show the most promise.

Get This Free Report