In my CEF Insider service, we focus exclusively on buying strong, 8%+ yielding closed-end funds (CEFs). It’s our MO! And there are a lot of CEF bargains now, as cautious income investors remain skittish following the 2022 correction.

But today I want to talk about when it’s time to sell a CEF. You might recall the old Warren Buffett quote that his favorite holding period is “forever.” Of course, Buffett was talking about blue-chip stocks, which are his forte.

With CEFs, our play is a bit different. Sure, we want to hold these high yielders (the average CEF tracked by CEF Insider yields 7.9% today) for as long as we can, to make the most of their high—and often monthly—dividends.

But we need to constantly watch other indicators too, especially the discount (or premium) to net asset value (NAV, or the value of a fund’s underlying portfolio).

Which brings me to the Brookfield Real Assets Income Fund (RA), a CEF that recently cut its dividend by a whopping 40%! It was disappointing, to say the (very!) least. Although cash flow was an issue, management didn’t have to bring in such a large cut all at once; it could’ve done smaller ones. Or it could have at least warned the market.

But let’s look past that and see what RA, which has never been a CEF Insider recommendation, by the way, mainly because it usually trades at a premium (more on that below) can tell us about when to sell a fund.

Let’s start with the name, which could lead you to believe that RA holds shares of infrastructure companies: pipelines, utilities, telecoms and the like. And it does have a small clutch (about 30% of the portfolio) in equities. But the vast majority is in bonds issued by these firms.

That’s takeaway No. 1 from this tale: always look past a fund’s name and make sure you know what you’re buying. You’d be surprised at how many investors make this mistake; and in fairness, CEFs’ names can be somewhat nebulous.

Anyway, onward. Let’s talk about April 2023, when many corporate-bond CEFs (and I’ll include RA here) rose during the banking crisis.

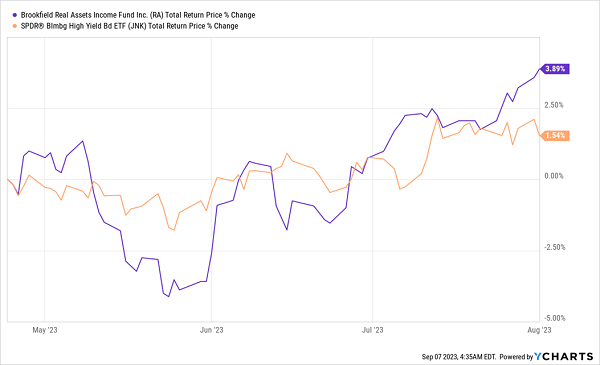

Investors Flocked to RA During the Banking Scare

Back in late April, in the heat of the crisis, I wrote, “The regular interest payments from bond issuers … offset the panic you get in short-term selloffs. That makes them a good alternative in uncertain markets.”

That’s why both the junk-bond market, shown by the performance of the benchmark SPDR Bloomberg High Yield Bond ETF (JNK), in orange above, and RA (in purple), climbed, with RA outperforming by a wide margin.

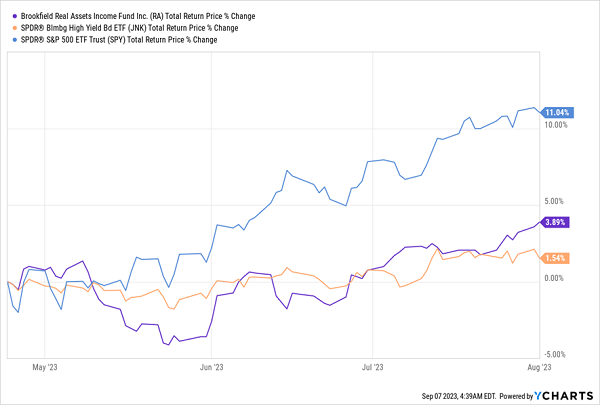

It made sense at the time … except the crisis wrapped up much quicker than I expected when I wrote that weekly article on our website, and stocks went on to outperform bonds by a wide margin:

Banking Crisis Eases Fast—and the Script Flips

With that mea culpa stated, this gives us takeaway No. 2: while we love to play trends like these, we need to be ready to change our thinking at a moment’s notice.

It’s why, in CEF Insider, we look to build a “base” portfolio of high-yielding funds we can hold for the medium to longer term, while taking opportunistic swings at shorter-term trends when we can.

Anyway, back to RA: The shift back into stocks became apparent in early May, as the banking crisis faded and people realized the S&P 500 was undervalued, as it was still way down from all-time highs (and remains so now, to the tune of around 6%).

A rotation back into stocks from corporate-bond funds like RA made sense based on the data. But there was something else happening that was more unique to this fund that was worth paying attention to:

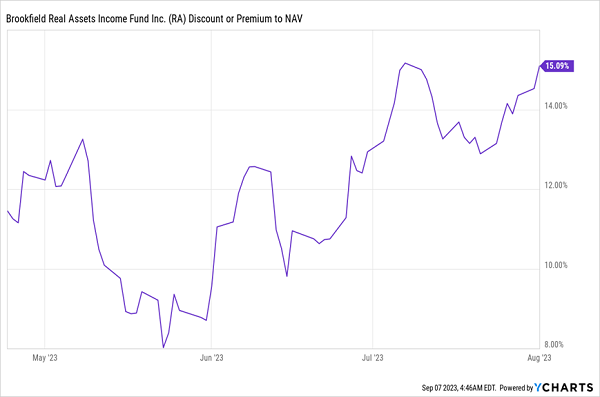

RA’s Premium Soars—at the Wrong Time

In 2023, total price returns have lagged total NAV returns for a plurality of CEFs, sustaining these funds’ discounts as demand remained low after the 2022 correction.

This is typical in non-bull markets. It wasn’t the case for RA, though, as its market-price return outran its NAV return, pushing its premium up to 15%, high even for this fund.

That’s takeaway No. 3: if your CEF’s premium or discount is moving in a different direction than other funds in its asset class, take note. And funds with premiums that are rising counter to the trend in their asset class are at particular risk.

While RA has had a premium for a long time, its premium soared to 15%, which itself is a sell sign, not just because you’re overpaying but because it pressures the dividend, which is takeaway No. 4 from our RA story.

Here’s why: let’s say a fund sports a 15% discount and yields 8%, based on its discounted market price. That means its yield on NAV (or the yield based on its underlying portfolio value, which management needs to cover the payout) is only 6.8%.

But that gets flipped when a fund trades at a wide premium: with a 15% premium, management needs a 9.2% yield on NAV to sustain that 8% yield on market price.

Post-cut, RA trades at a 13.6% discount, which has made its dividend (which yields 11.2% on a forward basis, based on its market price) safer, since that translates to a 9.7% yield on NAV—not far above the average 8.8% yield RA’s class of corporate bonds pays out. And RA is unlikely to cut again, given the 20%+ price hit it took.

RA’s story underlines the importance of diversification among CEFs—our final takeaway. When you aim to build a portfolio of medium- to longer-term holds (as we do in CEF Insider) while working to tap shorter-term trends (and letting funds’ discounts be our guide across the board), you’ll be less affected by duds like RA. And you’ll collect a high income stream the whole time.

5 More “Hidden” Funds Trading Cheap (and Yielding 10.2%)

I call CEFs “hidden” funds because the big investment houses (which often manage CEFs and ETFs) put almost zero marketing muscle behind them.

There’s a reason for that: if investors discovered the income (and profit) power of CEFs, they’d likely never buy an ETF again! But if we want to retire well—and on dividends alone—8%+ paying CEFs really should be part of our strategy.

To learn more about these high-yield funds, click right here to read my Special Investor Bulletin. In it, I’ll reveal my CEF-investing strategy and give you the opportunity to download a free Special Report naming 5 of my top bargain-priced CEF picks (current yield: 10.2%!).

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Growth stocks offer a lot of bang for your buck, and we've got the next upcoming superstars to strongly consider for your portfolio.

Get This Free Report