The yield on the 10-year Treasury has rallied near 3%. Yet there’s no way you and I are retiring off that pittance!

Hence the appeal of closed-end funds (CEFs), which regularly pay 7% or better. That’s the difference between a paltry income below $30,000 on a million buck nest egg or a respectable $70,000 annually.

And if you’re smart about your CEF purchases, you can even buy these funds at discounts and snare some price upside to boot!

With the markets in flux (to say the least), now is a good time to review the principles of successful CEF investing. They are more nuanced than classic stock picking because we’re analyzing managers, strategies and holdings versus simple businesses models.

It’s easier to count on dividends via the number of cellular subscriptions Verizon Communications (VZ) has than it is to determine how much interest income the DoubleLine Income Solutions Fund (DSL) generates.

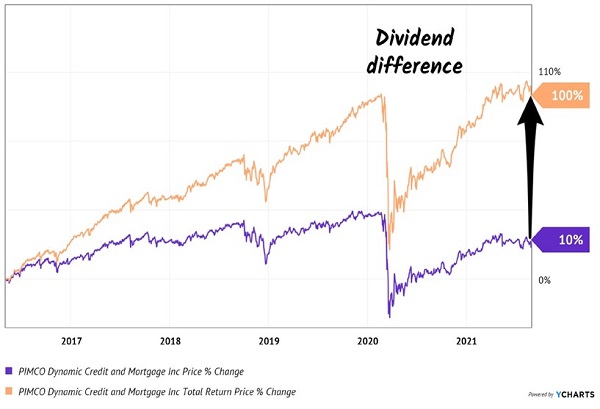

CEF Rule #1: Be Careful with Price-Only Charts

The PIMCO Dynamic Income Fund (PDI) has been a strong performer since its 2012 inception. Its sister fund PIMCO Dynamic Credit and Mortgage Fund (PCI), which was recently absorbed into PDI, was equally great to my Contrarian Income Report subscribers.

Traditional analysts miss the beauty of PCI because they miss the payouts. The dividends make the difference.

PCI: A Dividend Double

A non-payout chart of PCI—purple line—would miss this dividend double—orange line. Be careful about price-only charts when evaluating CEFs. Brokerage statements typically report price-only returns, too.

CEF Rule #2: Collect Your Cash Quickly

In less than six years we collected 70% of our original purchase price in dividends from PCI. Plus, the fund gained value while it was paying us! It was like an annuity, but better. It paid more, and our capital kept growing. (We earned 98% total returns from this purchase in our CIR portfolio!)

CEF Rule #3: Demand Alpha

Past performance can be an indicator about the quality of the management team and its strategy. PCI and PDI have had the benefit of the brightest bond minds on the planet calling the shots from retired “Bond King” Bill Gross to current superstar Dan Ivascyn).

They have consistently beat the bond benchmark SPDR Bloomberg Barclays High-Yield Bond ETF (JNK). Since inception, PDI has pummeled JNK, delivering total returns of 188% versus 46%!

CEF Rule #4: Know What’s Funding Your Distributions

A closed-end fund can pay you from some combination of:

- Investment income,

- Capital gains, and/or

- Return of capital.

Of the three, investment income is preferable because it’s usually the most reliable. Many CEFs pay monthly distributions, so it’s best if they match up their payouts with steady income streams.

Capital gains from rising bond or stock prices can further boost distributions. But they are at risk of disappearing if the markets drop.

Finally, everyone assumes that return of capital is bad because it’s simply shipping your money back to you. But if the fund trades at a significant discount, this can actually be a savvy way to kick-start the closing of a discount window. More on this shortly.

CEF Rule #5: Don’t Be Cheap About Fees

Most investors are conditioned to a fault by their experience with mutual funds and ETFs to search out the lowest fees. This makes sense for investment vehicles that are roughly going to perform in line with the broader market. Lowering your costs minimizes drag.

Usually, but not always. Closed-end funds are a different investment animal, though. On the whole, there are many more dogs than gems. It’s an absolute necessity to find a great manager with a solid track record. Great managers tend to be expensive, of course – but they’re well worth it.

The stated yields you see quoted, by the way, are always net of fees. Your account will never be debited for the fees from any fund you own. They are simply paid by the fund itself from its NAV. You receive the yield you see—a rare and very happy case of truth in packaging!

CEF Rule #6: Demand a Discount

One aspect of the CEF structure lends itself perfectly to contrary-minded investing: a fixed pool of shares.

Mutual funds issue more shares whenever they want, fixed each day at NAV. But closed ends have a fixed share count, with their funds trading like stocks. As a result, from time to time a fund will fall out of favor and find its shares trading at a discount to its NAV.

This is basically “free money” because these underlying assets are constantly marked to market (unlike mutual funds). If a fund trades at a 10% discount, management could theoretically liquidate the fund and pay everyone $1.10 on the dollar. Or it can buy back its own shares to close the discount window (and boost the share price).

A discount is a great start but do make sure that management has a plan to close that window! Sometimes, the discount is for a reason, so we dig deeper.

CEF Rule #7: When Possible, Buy Along Insiders

It’s rare to see any fixed income manager put his or her own money on the line at all, unfortunately. Barron’s research showed that, out of 558 closed-end funds at the time of its study, nearly half (269) had no insider ownership whatsoever. And only 70 have insider ownership above $500,000.

I’ve seen no evidence that insider ownership is any higher today, which raises the question: why would we want to own any of them, if the managers have no skin in the game?

What we want is a Bradford Stone, one of the managers at the Flaherty & Crumrine Dynamic Preferred and Income Fund (DFP), whose 27,000 shares of DFP is worth around $756,000 today.

CEF Rule #8: The “No Withdrawal” Retirement Strategy

Closed-end funds are a cornerstone of my 7% “no withdrawal” retirement strategy, which lets retirees rely entirely on dividend income and leave their principal 100% intact.

Well that’s not exactly right.

Their principal is more than 100% intact thanks to price gains like these! Which means principal is actually 110% intact after year 1, and so on.

To do this, I seek out closed-end funds that:

- Pay 7% or better…

- Have well funded distributions…

- Trade at meaningful discounts to their NAV…

- And know how to make their shareholders money.

And I talk to management, because online research isn’t enough. I also track insider buying to make sure these guys have real skin in the game.

Today I like three “blue chip” closed-end funds as best income buys. And wait ‘til you see their yields! These “slam dunk” income plays pay 8.1%, 7.8% and even 6.3% dividends.

Plus, they trade at 10 to 15% discounts to their net asset value (NAV) today. Which means they’re perfect for your retirement portfolio because your downside risk is minimal. Even if the market takes a tumble, these top-notch funds will simply trade flat… and we’ll still collect those fat dividends!

If you’re an investor who strives to live off dividends alone, while slowly but safely increasing the value of your nest egg, these are the ideal holdings for you. Click here and I’ll explain more about my no-withdrawal approach – plus I’ll share the names, tickers and buy prices of my 3 favorite closed-end funds for 8.1%, 7.8% and 6.3% yields.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Options trading isn’t just for the Wall Street elite; it’s an accessible strategy for anyone armed with the proper knowledge. Think of options as a strategic toolkit, with each tool designed for a specific financial task. Get this report to learn how options trading can help you use the market’s volatility to your advantage.

Get This Free Report