This has been a great year for stocks—and a great year for our 8%+ yielding closed-end funds (CEFs), too.

That makes sense: Many CEFs invest in stocks, and many more hold bonds issued by publicly traded firms, so what’s good for stocks tends to be good for CEFs.

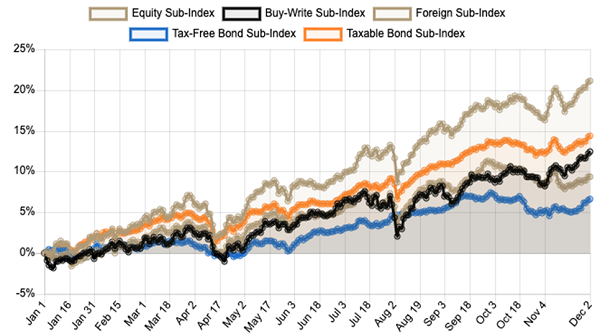

CEFs March Higher in ’24

Source: CEF Insider

When we look at the proprietary indexes we use to track CEFs at my CEF Insider service, we see that the equity sub-index has done the best, with a 21% year-to-date total return. Corporate bonds are second at 14.3%. Municipal bonds, known for lower volatility and risk, have gained a bit less, as you’d expect, at 6.6%. Foreign assets are up 9.4%.

So on the whole, CEF investors have done well across the board, and the high yields—an average of 8.2% across the space—sure haven’t hurt, either!

Even so, there are some CEFs that are down this year. Since 2024 has seen growing profits pretty well everywhere, it’s worth looking at why those funds have slumped.

Looking at weaker funds can benefit us in a couple of ways: First, it gives us a sense of what to avoid when picking CEFs in the future. And we can see if these beaten-down CEFs are worth buying now, or if they have further to fall.

CEF #1: A South-of-the-Border Fund Goes … South

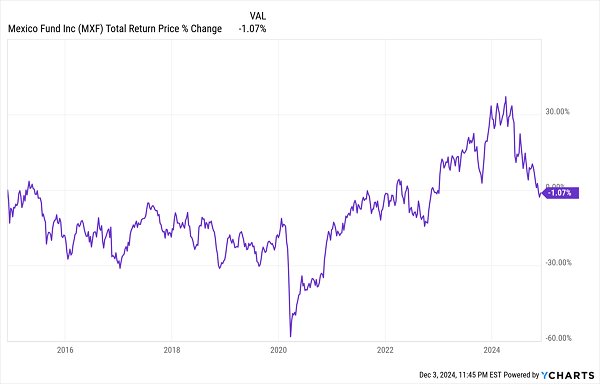

Let’s start with the best aspect of the Mexico Fund (MXF), a CEF I don’t talk about often: the dividend, which yields 6.5% and has been rising since the pandemic. That’s a good sign, but it’s been offset by a drop in the fund’s market price this year, dragging its overall total return lower.

MXF Quickly Reverses Its Recent Gains

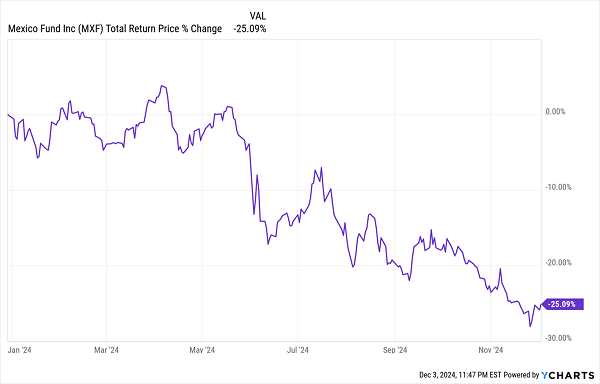

MXF has struggled over the last decade, and after finally earning a 2.7% annualized return earlier this year after years of losses, the fund seemed like it might be turning the corner. Then it erased that profit and is now sitting on a 25.1% annualized loss for 2024, even accounting for its generous payouts.

MXF Shows Early-Year Promise, Then Drops

This decline began in the spring and is all about Mexico’s low growth, which is expected to drop from 3.3% in 2023 to 1.6% for 2024.

Add the headaches Mexico is likely to have with potential tariffs on exports to America, and it’s clear that a fund like MXF is loaded with risks. Investors are right to avoid it.

CEF #2: A 40% Discount That Could Get Bigger

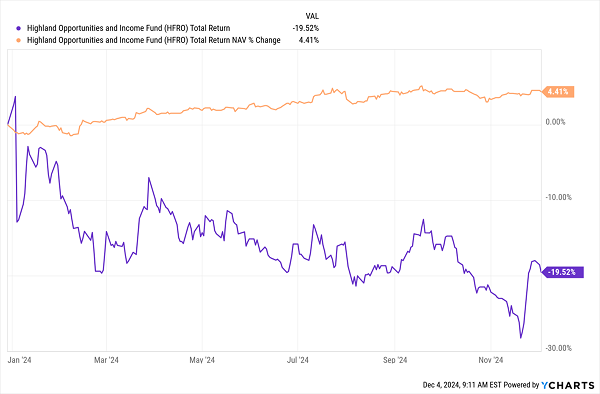

MXF’s weakness is largely due to trends outside its control. But management of the Highland Opportunities and Income Fund (HFRO) is partly responsible for the fund’s 19.5% year-to-date price decline, based on the fund’s market price–based total return, as of this writing (see the purple line below).

That drop comes even though HFRO’s total return based on net asset value (NAV, or the value of its portfolio, including dividends collected) has been positive (orange line). (Because CEFs’ share counts are generally fixed, their NAV and market price can differ, resulting in discounts or premiums we can exploit.)

HFRO Gains and Slumps at the Same Time

Funny thing is, the fund’s market price–based return has mostly been flat since the summer, even though management has a range of options to boost returns. That’s where the “opportunities” in the name comes from: HFRO can invest in a variety of real estate and debt instruments (alongside equities when it sees opportunities). So what’s going on here?

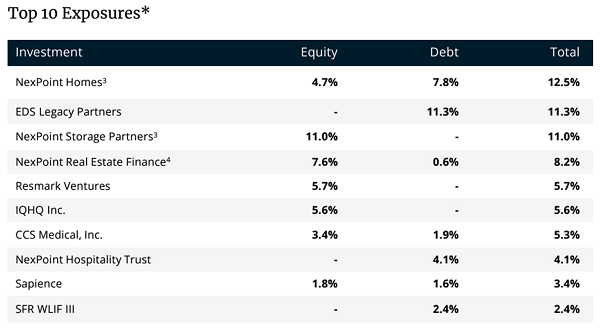

If we look at HFRO’s top holdings, we see that its management firm, NexPoint, has invested significantly in NexPoint properties:

Source: NexPoint Asset Management

While NexPoint may see NexPoint assets as the best places for HFRO’s investments, I’m concerned that these haven’t, in fact, helped investors much. The market agrees, as HFRO’s shockingly wide discount of 40% at the start of 2024 is over 50% now.

Yes, this 8.7% yielder could get a bid, especially since its payouts aren’t likely to be cut soon. But the odds of a big gain are low unless management changes course.

CEF #3: A China Fund That’s Lagging Chinese Stocks

Going back to the theme of international exposure, the third-worst-performing CEF of 2024 has been Morgan Stanley China A Share Fund (CAF), which is down 2.7% as of this writing. (Oddly among CEFs, this one isn’t a major income play, offering one distribution a year that can vary. Based on the last 12 months, CAF yields just 1%.)

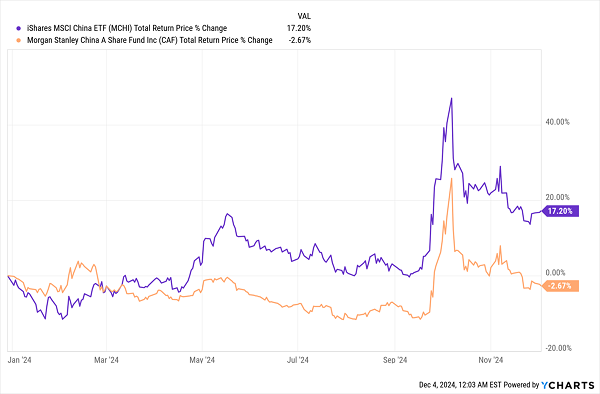

CAF’s decline isn’t the result of poor macroeconomic luck, as is the case with MXF: CAF (total return in orange below) invests in a country whose stock market (shown by its benchmark index fund in purple) has done well this year.

CAF Trails Its Benchmark

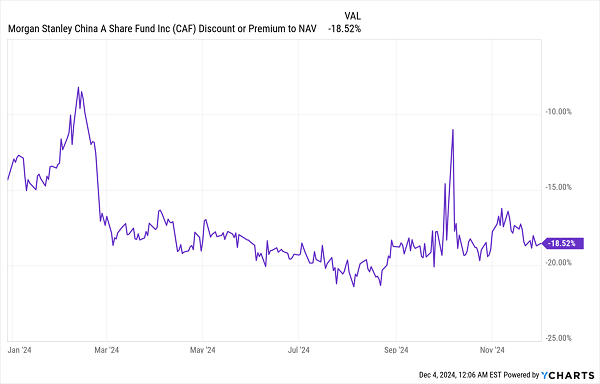

Management decisions are part of the problem, but CAF’s total NAV return is up nearly 3%, so that’s not the only issue. Again, as with HFRO, the issue is that CAF has swung to a bigger discount during the year, though its 18.5% markdown isn’t as severe as that of HFRO:

CAF Gets Cheaper

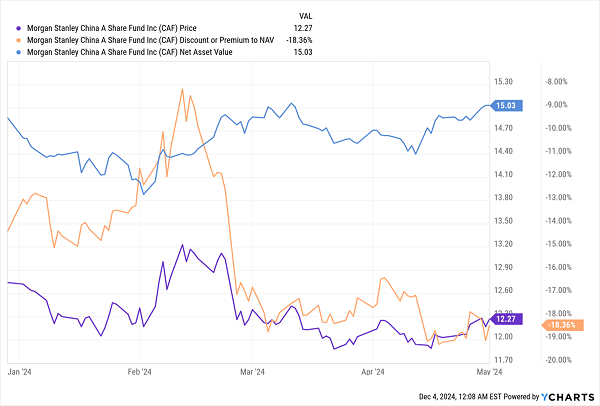

The dramatic closing of CAF’s discount in February, followed by its sudden drop later that month, tells us everything we need to know about the risks here: Some speculation drove CAF’s market price up earlier this year (see the orange line below), but with the fund’s NAV remaining flat (light blue line), CAF’s market price (purple) couldn’t keep up and the fund’s price dropped.

CAF Fails to Meet Expectations

The fact that this fund attracted so much interest is a warning sign. Without changes, there’s no reason for CAF to be bid up above where it was. Yet that’s what happened as the trade in CAF got crowded. When it was unwound later that month, the fund’s losses stuck, and it hasn’t recovered since March.

Conclusion

These funds aren’t the worst CEFs out there, but they’re definitely struggling. And the truth is, the issues surrounding them were easy for investors to avoid; 2024 was a great year to buy American, as we discussed late last year, making CAF and MXF funds to stay away from. And while I have seen (and continue to see) some light at the end of the tunnel for HFRO, we prefer the 21.8% average total return, as of this writing, we’ve seen in the four corporate-bond funds held in our CEF Insider portfolio for 2024.

Shock Bargain Alert for 2025: 4 AI Funds Paying Huge 9.8% Yields

I know AI has been talked to death over the last couple years, and if you didn’t buy, say, NVIDIA (NVDA) before it took off, you might think you’re too late to the party here.

Not true.

In fact, through the 4 CEFs I’m urging investors to buy today, you can still profit from the power of this transformative technology at a bargain—and collect an incredible 9.8% dividend in the process.

But there’s no time to lose: As AI embeds itself in more apps and devices, more investors are going to be looking at overlooked bargain funds like these four. Don’t miss out. Go here to learn more about these 4 unique “AI-Powered” dividends and get a free Special Report revealing their names and tickers.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Wondering where to start (or end) with AI stocks? These 10 simple stocks can help investors build long-term wealth as artificial intelligence continues to grow into the future.

Get This Free Report