Nice to see our friends over at Barron’s finally catching up to us on the big dividends sitting right under our noses in oil and gas!

It’s almost like the magazine’s writers are sharing a subscription to our Contrarian Income Report service, because the six stocks they cited in an article they ran last week are almost all picks in our portfolio—specifically our “crash ‘n rally” energy bucket.

(It’s not the first time’s Barron’s has shadowed us. In April, they put out a strategy for retiring on dividends, a subject we literally wrote the book on two years ago.)

How We Scooped Barron’s on Monster Energy-Sector Payouts

I say Barron’s “finally” caught up because we’ve been profiting from big dividends since April 14, 2020, when we jumped in following the depths of the energy sector’s faceplant, snapping up natural-gas pipeline operator ONEOK (OKE) when it was yielding just under 12%. (That high yield resulted from OKE’s decimated share price following the March 2020 catastrophe.)

Since then, our OKE position has doubled (including its mammoth dividend).

We Bought Energy When Energy Wasn’t Cool

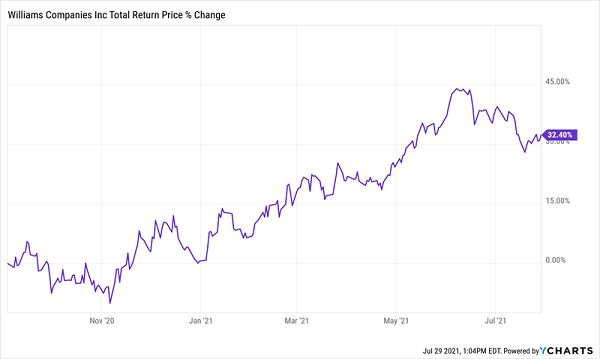

Then there’s fellow gas shipper Williams Companies (WMB), which we picked up later in the energy rebound (when it yielded a gaudy 7.7%), in September of last year. We’ve bagged a nice 32% return since:

WMB: Another Resource Pick That Paid Off

I’m flattered to have a secret admirer at Barron’s, and the truth is, the magazine is right: the energy space is still a great place to hunt for high-yield bargains.

Oil and Gas Prices Are Volatile—Except When They’re Not

My only critique is that Barron’s failed to mention why these energy stocks are still such great deals today. That’s too bad because this really is the meat of the story.

Here’s the upshot: as you and I both know, the business media loves to go on about how volatile oil prices can be, and to a large extent they’re right: hands up if you predicted oil prices would go negative in March 2020.

But as with many things in investing (and in life!), there are two sides to this story. And the truth is, oil and gas prices also go through times of great predictability. That’s especially true in the wake of a crisis like the COVID-19 pandemic.

Our “Crash ’n’ Rally” Dividend Play Explained

Take oil. If history is any guide, the goo—and shares of the companies that produce and ship it—should rally for another two or three years, at least. Energy prices tend to “crash ’n’ rally.” The crash is quick, while the ensuing rally lasts for years. Here’s how it played out in 2008 and 2020:

- Demand for oil evaporates and its price crashes (2008 and 2020).

- Energy producers scramble to cut costs, so they cut production aggressively (2009 and 2020).

- The economy slowly recovers (2009 and late 2020), energy demand picks up, but supply lags.

- And lags. And lags. And the price of oil rallies until supply eventually meets demand (2009 to 2014 and 2020 to present).

America’s shale producers are playing into this storyline by not rushing to throw the taps open: last week, oil-services provider Baker Hughes (BKR) said it sees only modest growth in shale production for the rest of 2021 as producers take a disciplined approach. Meantime, the IEA says it sees oil demand hitting pre-COVID levels in mid-2022.

The bottom line here is that $100 oil is certainly on the table in the next two or three years, meaning we should buy oil stocks with strong dividend histories, especially now that we’ve had a bit of a pullback in prices, with oil sitting around $73 a barrel as I write this, down a bit from over $75 in mid-July.

Energy CEFs Can Generate Bigger Yields—and Bigger Gains

Actually, I have another critique of the Barron’s piece: they could have gone a little deeper into the various dividend-paying investments available in the oil market. If they had, they’d have come up with some very high dividends trading at some truly unusual discounts.

I’m talking about energy-focused closed-end funds (CEFs). As we speak, there are CEFs in this sector yielding upwards of 7% and trading at deep discounts to net asset value (NAV, or the value of the stocks in their portfolios). These discounts are a major source of upside for CEFs, and you can easily spot them on any CEF screener.

This makes our job easy: we look for a CEF trading at an unusual discount and then ride along as that discount disappears, propelling the price higher as it does.

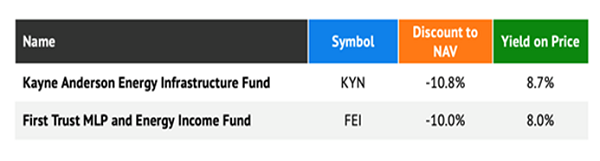

And I’m going to make it even easier for you with two CEFs to put on your list: the Kayne Anderson Energy Infrastructure Fund (KYN) and First Trust MLP and Energy Income Fund (FEI).

KYN is a holding of my short-term trading service Dividend Swing Trader. As you can see in the table above, it yields a sky-high 8.7% today and trades at a huge 11% discount.

In other words, you can pick up its portfolio of energy stocks—mainly master limited partnerships (MLPs) that operate oil and gas storage facilities and pipelines—for 89 cents on the dollar!

KYN gives you ONEOK and Williams among its top holdings, as well as other leading oil and gas shippers, like Enterprise Products Partners (EPD) and Energy Transfer LP (ET).

We can thank the recent pullback in oil prices for this deal: KYN traded at a discount as narrow as 5.8% in early July. I expect it to break back over that level in the next few months as it makes a run for par.

FEI, for its part, boasts a similar dividend—8% in this case—with the added bonus that it comes your way monthly, rather than quarterly. You also get a bit more geographic diversification, with Canadian firms accounting for 15% of the portfolio.

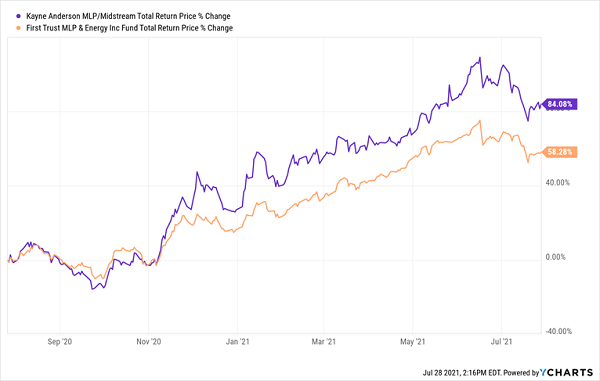

As with KYN, we’ve got a nice discount opportunity here, with FEI trading at 10% below NAV, down from its 2021 high of around 6%. However, KYN outperformed FEI in the last 12 months on a total return basis.

KYN Runs Ahead Following the March 2020 Disaster

While both funds have strong outlooks, KYN’s strong performance, plus its wider discount, could attract more investors in the next few months, giving it an extra upside boost.

This Incredible Portfolio Lets You Retire on Dividends Alone

These bargain-priced energy funds are just the start. You can actually build an entire balanced portfolio with closed-end funds (and other high-yield investments) that pays you 7% dividends, pays you every month—and sets you up for steady price upside, too.

You’ll find everything you need in my “7% Monthly Dividend Portfolio.” As the name says, it’s designed to pay you 7% yields—enough to deliver $42,000 in yearly dividends on a $600K investment—and pay you every month, too.

That monthly frequency lines up perfectly with your bills. And with just a $600K investment, you can get a retirement-ready income stream on a lot less than the million bucks most analysts say you need.

The whole story—including a complete guided tour of every stock and fund in this cash-spinning portfolio—is waiting for you here. Don’t miss this rare opportunity for massive dividend income and strong gains.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Unlock your free copy of MarketBeat's comprehensive guide to pot stock investing and discover which cannabis companies are poised for growth. Plus, you'll get exclusive access to our daily newsletter with expert stock recommendations from Wall Street's top analysts.

Get This Free Report