These small business lenders trade publicly—and offer payouts between 10.5% and 13%.

You have our attention.

We’ll discuss three stocks in the space in a moment. First, let’s address why these companies exist.

When small businesses need cash, they typically don’t dial up their banks. Increasingly, they turn to a small subset of private equity-esque companies for help. These unique companies throw off double-digit yields and can often be found trading for less than they’re worth. Not bad when we’re talking dividends up to 13%!

My Favorite Way to Collect Big Checks From Small Businesses

Once upon a time, when small businesses held out their hands for much-needed growth capital, banks were the only game in town. The problem? Small businesses make for risky investments. These days most banks are allergic to risk—so, they don’t provide growth capital.

But small businesses often need cash to grow. Some of that void has been filled by private lenders, but that’s no help to individual investors. Private credit, much like private equity, requires a virtual suitcase full of cash to get involved, and is way too illiquid for our tastes.

Enter business development companies (BDCs), the stocks we are interested in.

BDCs provide a variety of financing solutions to private small businesses. They’re private equity-esque, but they trade on public exchanges, allowing us to jump in for as little as $10 or $20 per share.

Most important is the dividend opportunity. BDCs share traits in common with real estate investment trusts (REITs). Both were creations of Congress. Both were meant to spark investment in certain assets. And both are required to pay out at least 90% of their taxable income back to shareholders in the form of dividends.

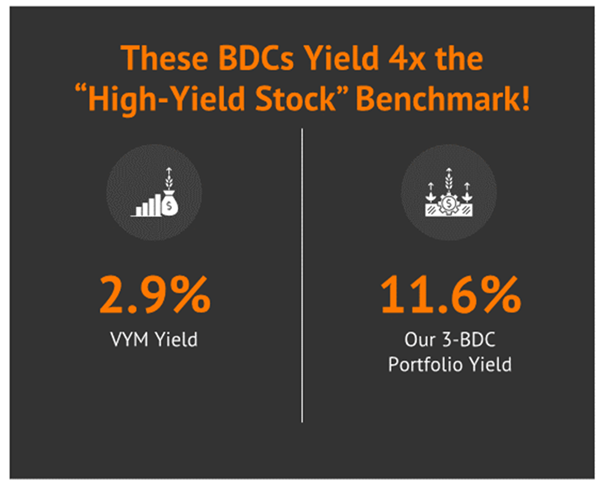

BDCs are more intriguing because they pay more. In fact, the three-pack we’re chatting about today yields roughly 4x more than the typical high-yield fund.

Prospect Capital (PSEC)

Dividend Yield: 13.0%

Let’s start with Prospect Capital (PSEC), which is emblematic of the discounts possible in the BDC space. Today, it trades at an eye-popping 62% of NAV. Put differently, its price is less than two-thirds of what it arguably should be.

But should we expect any less from one of Wall Street’s most hated stocks?

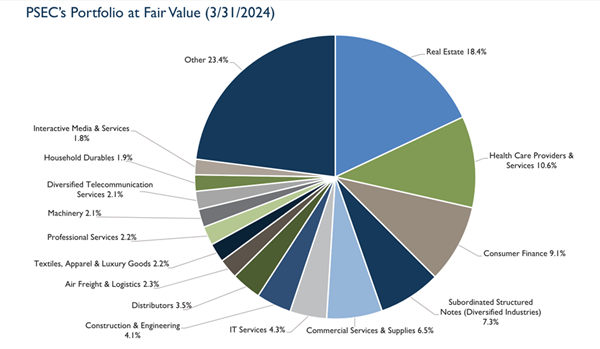

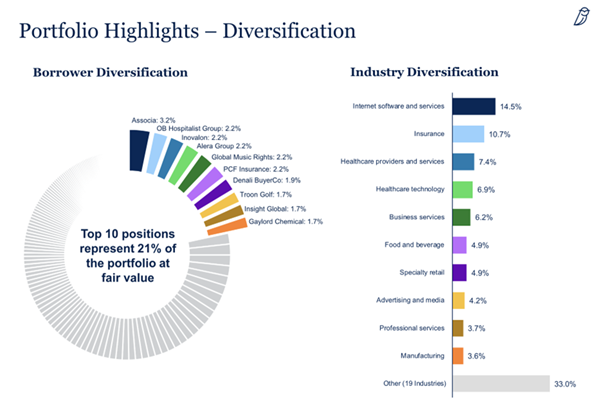

Prospect Capital, at least by market cap ($2.3 billion), is one of the BDC industry’s blue chips. Its portfolio includes 122 investments across 36 industries, and the majority (81%) of those investments are first lien, secured, or underlying secured debt. The bulk of its business is in middle-market lending to companies with EBITDA of up to $150 million, though it also participates in real estate (typically multifamily properties) and subordinated structured notes.

Source: May 2024 Investor Presentation

Based on many of its bona fides, PSEC is tough to resist. It’s highly diversified. Its portfolio boasts a low non-accrual rate (just 0.4%). It pays monthly dividends. And the dividends have been well-covered for a while now, at roughly 85%-90% of net investment income (NII).

The problem?

Prospect Capital has a lousy track record that’s marred by several dividend cuts and underperformance compared to its better-managed peers. That’s why PSEC’s deep discount to NAV is so deceiving: This isn’t a sudden fire sale; the stock has traded at a fat discount for years.

As I said recently, investors should be cautious betting against PSEC, because if it can keep stringing together rosy reports as it has for the past couple quarters, it could shake out a lot of bearish hands. But the burden of proof of a more permanent positive change in fortunes is squarely on PSEC’s shoulders.

Barings BDC (BBDC)

Dividend Yield: 10.5%

Not as cheap, but certainly more promising, is Barings BDC (BBDC)—a sunny reform story in the BDC space.

Up until August 2018, Barings was actually Triangle Capital—a BDC that served lower- and middle-market firms, and that repeatedly wrote off bad investments and hacked away at its dividend. Eventually, the company would not only rebrand, but also pick up a new external adviser—global financial services firm Barings, which would set to work overhauling BBDC’s portfolio.

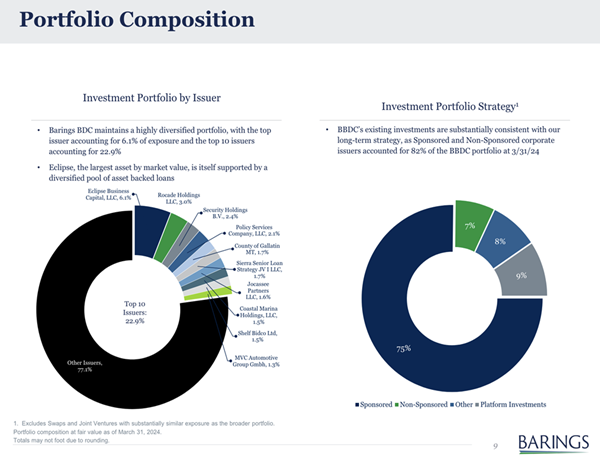

Today, Barings primarily invests in senior secured private debt investments in “well-established” middle-market companies across numerous industries. It currently boasts 337 portfolio companies across a number of industries. Two-thirds of its investments are first lien loans, though it also has second lien, mezzanine, equity, structured, and joint venture investments.

Source: Q1 Conference Call Presentation

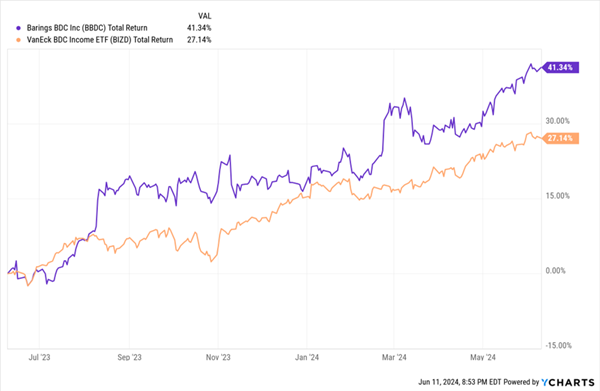

BBDC shares currently trade at a 14% discount to NAV—a surprisingly low valuation given that Barings has whooped its BDCs peers over the past year.

Barings Makes the Most of a Great Stretch for BDCs

There’s little to criticize here. Barings runs a high-credit-quality portfolio with few non-accruals, and it has covered its dividend for years without breaking a sweat.

Blue Owl Capital III (OBDE)

Dividend Yield: 9.4%

Blue Owl Capital III (OBDE), which falls under the umbrella of alternative investment manager Blue Owl Capital (OWL), is one of the newest BDCs we can get our hands on. It came to life in 2020 and hit the public markets in January 2024.

OBDE predominantly invests in senior secured debt (89% of fair value), though it also will participate in deals that involve unsecured debt, common equity, and preferred stock. Virtually all of its investments are floating-rate in nature.

Its current portfolio is a broad 190 companies, scattered across a couple dozen industries.

Source: May 2024 Investor Presentation

There’s little track record to go on here, but there are a few reasons to keep OBDE on our radar.

Credit quality is great—it boasts the lowest non-accruals as a percentage of fair value (0.3%) of the three BDCs mentioned here. Despite the short trading life, OBDE shares have already started to fall into value territory, at a modest 4% discount to NAV. And OBDE can also tap a deep bench of investment professionals within Blue Owl, which is a leading name in private credit.

The dividend situation, at least in the short term, is surprisingly concrete, too. Blue Owl currently pays a 35-cent quarterly dividend, but it has also announced a series of five special 6-cent dividends extending out into 2025. That’s a lot more certainty than we typically get with special dividends.

Just be mindful of potential drags. For one, OBDE charged just 50 basis points in management fees while it was private—but once it went public, that jumped to 1.5 percentage points, plus incentive fees on top of that. In its most recent quarter, expenses jumped from $35.1 million to $64.7 million as a result. Also, OBDE has three lock-up expirations—July 23, Oct. 21, and Jan. 24 (2025)—that could bring on some selling pressure.

Give Me 5 Minutes, And I’ll 5X Your Retirement Income

I love the sky-high potential of BDCs, which can churn out both fat yields and strong price returns when the American economy gets going.

But in a cooling economy—which we’re already seeing several signs of—the pain tends to be worse for the small businesses that BDCs hold.

So the question is: What are you looking for?

If you need a can’t-miss retirement cash machine that you want to hold for decades, you need stocks and funds that will stand on their own.

That means no relying on the Fed.

No relying on oil prices.

No relying on a Cinderella economy in perpetuity.

And if you’re thinking “No way those kinds of stocks exist,” think again. Because these are exactly the kinds of names I hold in my “Perfect Income” portfolio.

We don’t chase trends. We don’t time the market. In my “Perfect Income” portfolio, we simply target high-yield investments (roughly 5x the S&P!) and hold on to them, no matter what the Fed, Congress or the rest of the world throws their way.

Perfect, right?

In addition to having high-single-digit and even double-digit yields, every single holding must check off several crucial boxes:

- They DO pay consistently, predictably and reliably.

- They DO survive—and even thrive—in market crashes.

- They DO deliver double-digit returns, with safe, secure investments.

- They DO require minimal management time—just a few minutes every month!

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Take control of your financial legacy today. Click here for my newly updated briefing on the Perfect Income Portfolio!

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Wondering where to start (or end) with AI stocks? These 10 simple stocks can help investors build long-term wealth as artificial intelligence continues to grow into the future.

Get This Free Report