Closed-end funds (CEFs)—our favorite 8%+ yielding investments—have a new (and popular!) fan. And he’s making a big move I see sending CEF prices higher.

Bill Ackman Discovers What We’ve Known for Years

I’m talking about Bill Ackman, one of the best-known activist investors out there. You’ve probably seen the head of Pershing Square Capital Management, a hedge fund with $18.3 billion in assets, in the media. He’s a regular commentator.

Ackman has scored some big wins in his career, such as his 2005 investment in The Wendy’s Co. (WEN). But he’s probably better known for his dramatic misses, like his losing bid to change the board of directors at Target Corp. (TGT) and his high-profile short position in Herbalife Ltd. (HLF) back in 2012.

On the plus side, Ackman’s investors do point out that his current fund has returned about 200% in the last decade.

Now, Ackman aims to launch a new CEF that will have $25 billion in assets under management, raised from investors. That would be the largest CEF ever, by a huge margin. It would also be the largest IPO in America this year. To put it in context, the largest CEF right now is the Physical Gold Trust Unit (PHYS), with $7.4 billion in assets.

As you’d expect, Ackman’s move is getting more people talking about CEFs. Reuters has suggested the fund will widen the pool of money going to these funds, and I fully agree. In fact, that’s the starting point we’re working from in our move to piggyback on Ackman’s move here.

More on that in a moment. First, let’s talk more about the scale of the opportunity this is creating for us.

Our “Back to the ’90s” CEF Play

This talk of activists moving into the CEF realm will probably ring a bell if you’re a member of my CEF Insider service. In our May issue, we discussed the moves activists recently made into CEFs, most notably Saba Capital Management’s effort to add its members to the boards of certain CEFs run by BlackRock.

This, too, has resulted in more CEF coverage from the Financial Times, Bloomberg and even The Economist, which previously hadn’t talked about these funds in years.

This could all mean that CEFs are facing another 1990s-like renaissance that could span the next decade.

Why am I mentioning the ’90s? Back then, CEFs exploded in popularity, as the stock market was doing well, and more people were looking to stocks to grow their wealth. Many fund managers responded by launching CEFs that gave investors significant benefits, such as:

- Access to fund managers’ ability to borrow to invest cheaply. Since many CEFs use leverage, this is a big edge, allowing us to, say, buy $1 of shares and borrow an additional 20 cents at the institution’s discounted rate.

- Professionally managed portfolios and distributions. This helps reduce volatility, lower risk and gets us a higher income stream, with 10% dividends common in CEFs.

- Quick and easy diversification, as one CEF can hold hundreds of different stocks, bonds, real estate investment trusts (REITs) and other assets. And CEFs are quite liquid, trading on the markets and available through any brokerage.

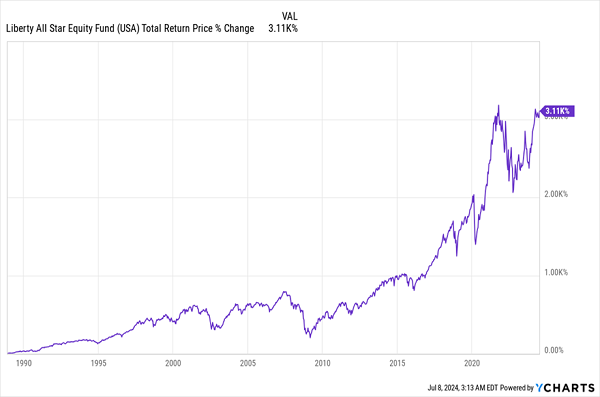

There were other benefits the industry discovered along the way, such as ways to minimize taxes and hedge market exposure through options trading. Some CEFs are darlings of the ’90s, like the Liberty All-Star Equity Fund (USA), a relative latecomer that launched in 1998. As of now, it yields 9.6% and has earned its first investors a 3,000%+ return!

USA Soars From IPO Onwards

These great days for CEFs didn’t last, though. When the dot-com crash caused people to turn to real estate in 2001, CEFs struggled alongside the rest of the financial world. Then, when stocks slowly began to recover in the mid-2000s, all that focus on skyrocketing house prices meant equity CEFs, and the rest of the market, couldn’t catch much attention.

Then, after the Fed raised rates in the mid-2000s, guaranteed investments offered a rate that was high enough to take some interest away from the 7% to 8% yields CEFs offered.

It took the stock market’s strong recovery in the 2010s, fueled by healthy growth in corporate profits (which nearly doubled in that decade) and the rapid expansion of the US economy for CEFs to gain some interest. But as I said a second ago, they’re still under the radar for most folks.

But thanks to Ackman and other activists, that’s changing.

How We’ll Play Ackman’s CEF Move (Without Buying His Fund)

The easiest way to play along with Ackman would be to buy his fund, but that’s probably not a good idea. Most CEFs trade at a discount to net asset value (NAV, or the value of the assets in their portfolios) for the first few years they exist. Ackman’s fund is likely to do the same.

Its discount may fade in time, but it will take time, and you’ll be stuck if Ackman decides to keep dividend payouts low. CEFs currently yield 8.2% on average, but Ackman could set the yield on his fund very low if he wants to, which would make the discount bigger.

Better to buy Ackman’s fund when it’s trading at a healthy discount. Until then, other CEFs could easily see their discounts narrow, propelling their share prices higher. Our top picks are the buy recommendations in our CEF Insider portfolio, of course. But let’s talk about a couple other, more speculative options that could see upside, too.

What about the fund we mentioned earlier, USA? This 26-year-old CEF has a nice domestic focus, with top holdings including Microsoft Corp. (MSFT), UnitedHealth Group Inc. (UNH), Visa (V) and lab-equipment maker Danaher Corp. (DHR).

Truth is, USA could see its discount narrow, but as the fund’s discount is just 2.6%, I wouldn’t expect a lot of upside here.

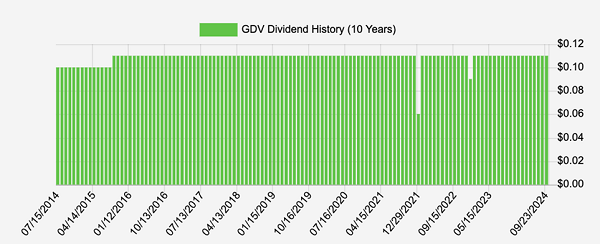

Instead, a deeper-discounted CEF like the Gabelli Dividend & Income Fund (GDV) could be better positioned to catch a bid on activist-driven interest in CEFs. GDV also holds US large cap stocks—American Express (AXP), Mastercard Inc. (MA) and Alphabet (GOOGL) are top holdings. It also trades at an alluring 14.7% discount to NAV.

The dividend yield is a little low by CEF standards, at 5.8%, but GDV does offer a monthly payout that only either holds steady or goes up. (Management also drops special dividends—the dips in the chart below—from time to time):

Solid Monthly Payout Makes Up for “Low” 5.8% Dividend

Source: Income Calendar

Moreover, as interest rates fall, that 5.8% yield will start to look more attractive to more folks.

Markdowns like the one on GDV could get whittled down, or vanish entirely, if more investors realize these discounts should not exist, and only do because CEFs were Wall Street’s best-kept secret. That is, until Bill Ackman let the cat out of the bag.

5 More “Hidden” 8.5%+ Yielding CEFs Primed to Soar 20% (Thank Bill Ackman)

The critical thing to remember about this opportunity is that we don’t even need Bill Ackman’s new CEF to launch! Just the chatter around it is enough to drive more folks into these high-paying funds.

And there are plenty more deep-discounted CEFs out there set to profit. I’ve zeroed in on 5 I see soaring 20%+ in the next year, due to their ridiculous discounts and more activist attention for CEFs in general.

What’s more, these 5 CEFs yield an outsized 8.5% on average, too!

Click here and I’ll tell you more about why CEFs have been off the radar for so long, and I’ll give you immediate access to a free Special Report naming all 5 of these cheap 8.5%-yielding CEFs.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Discover the top 7 AI stocks to invest in right now. This exclusive report highlights the companies leading the AI revolution and shaping the future of technology in 2025.

Get This Free Report