Me: “Let’s find companies with lots of debt and buy them. And make a lot of money.”

You: “Wait, what?”

(Nod as always to the late, great Norm Macdonald.)

Hear me out. Last week, plain vanilla investors threw a midweek fit when Federal Reserve Chairman Jay Powell said something we contrarians assumed already: No rate cut coming in March.

The Fed decides the Fed funds rate. This often cues the two-year Treasury yield to follow. (Yes, sometimes, the two-year leads. As always in economics and relationships, it’s complicated.)

We can debate who leads who, but the key is that the Fed controls short-term rates, but the bond market determines long-term rates.

These peaked last October when Mr. and Ms. Market achieved peak insanity. The 10-year rate soared above 5% and, on its journey to the stars, clipped equities. A high long rate upsets every applecart in finance.

When companies refinance debt, their new rate is some function of the 10-year (not the two-year). Which is why the highly-indebted companies that I joked about at the outset had such a rough autumn. When the 10-year is popping, nobody wants to own these names because refinancing is more costly and dangerous.

Such bearish certainty piqued our contrarian interest.

Back in October, we called “BS” on the broader narrative that long rates were heading to the moon:

Here’s the thing. This is not a sustainable move.

Inflation isn’t really in a spiral higher. In fact, it’s the opposite. Core PCE (personal consumer expenditures)—the Federal Reserve’s preferred measure of inflation—is dropping like a rock.

Wall Street has come around to our way of thinking, with big tech stocks pushing to new all-time highs. But many stocks have not participated in the move—especially companies with lots of debt.

Which is the aisle where we’ll go shopping.

Highly-leveraged utilities look particularly interesting here. First, these companies generate secure, consistent cash flows. They are so steady that they often carry high debt levels, which is generally fine, unless we’re talking about years like 2022 and 2023 when interest rates rose relentlessly.

Fortunately this ain’t 2022-23 any longer. This is 2024 (and already February, believe it or not!). Two years’ worth of rate hikes will eventually kick in. The Fed’s policy of holding rates “higher for longer” has a mission: to slow the economy.

It’s unlikely that the Fed cuts rates until we see signs of slowing. Which may mean that we are already in a recession because most of the Fed’s data is time delayed.

An eventual economic slowdown is quite bullish for utilities. Whether they rally now or later they are going to rally. Utes benefit from slowdowns two-fold.

First, investors flock to utility stocks for safety. And second, utes command higher valuations when long-term interest rates decline. Which always happens when the economy slows.

So let’s hold our noses, dear reader, while we consider Ameren Corp (AEE). It’s as hated as any utility stock on the board today. Nine analysts cover the stock, and only two have it rated as a Buy. This is quite bearish for Wall Street suits who generally make more money when they say buy, buy and buy.

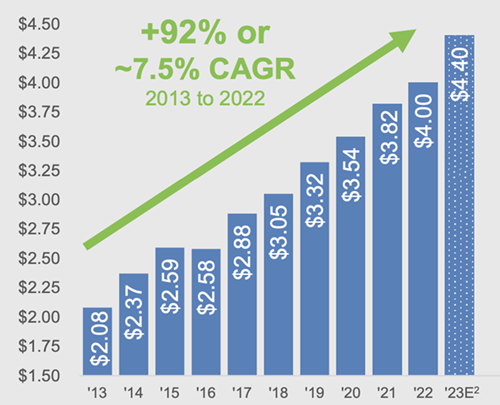

Ameren has 2.4 million electricity customers plus over 900,000 gas customers in Illinois and Missouri. This “captive audience” is helping power 7.5% earnings growth per year.

Earnings per Diluted Share

This cash flows through directly to Ameren’s dividend. Over the past five years, this overlooked player has raised its payout by a wonderful 33% to pay 3.6% today. Pretty sweet, right?

Yes—but most vanilla investors disagree. They’ve dumped AEE shares while interest rates have risen, concerned that higher interest rates will weigh on the company.

Fair enough, but interest rates are now on the way back down. Yet AEE appears to be in the final stages of a selling washout.

We’ll take the fire sale prices while they are available.

Once interest rate worries abate, this stock should bounce quickly. It’s the type of “recession-resistant” payer we want to own when the economy slows and rates fall.

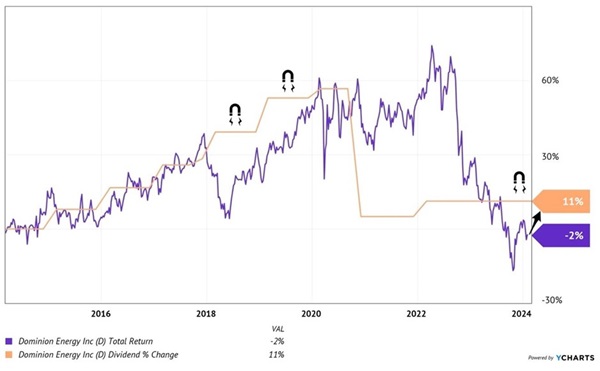

Same goes for Dominion Energy (D), the cheapest blue-chip utility today. Dominion yields 5%. It rarely pays this much!

Why the deal? D’s in the dividend doghouse because the company cut its payout in late 2020.

Why the chop? Too much debt back then. Dominion sought growth through an acquisition binge. It backfired.

The result was a rare payout slash from a utility—an income investor’s worst nightmare. That’s why first-level investors keep Dominion in the doghouse today.

Which intrigues us here at Contrarian Outlook. Did we hear doghouse? And a dividend cut in the rear-view mirror?

You have our full attention, D!

Chief financial officers (CFOs) are like carpenters. It’s best to measure twice and cut only once.

As a result, the safest dividend is often the one that has recently been cut. Unless management is a complete clown show, the last thing they want is to have to cut twice when they had to be strapped to the gurney to do it once!

Which is why the recent dividend raise from Dominion is encouraging. It shows confidence that the current dividend is being paid comfortably.

From a “dividend magnet” standpoint, the stock has more upside from here. Over the past 10 years, even net of the cut, Dominion’s dividend is up 11%. Not great, but the stock has been unfairly punished. From a price-only standpoint, the stock trades below where it did a decade ago!

D’s Dividend Magnet is Due

Over the long run, stock prices track their payouts—higher and lower. They can overshoot and undershoot for months, sometimes years at a time. Eventually they find their way home.

As we speak today, Dominion’s price lags its payout. Which is why we want to lock in its 5% yield. We’ll enjoy a bit of upside, too, when this stock gets up off the mat.

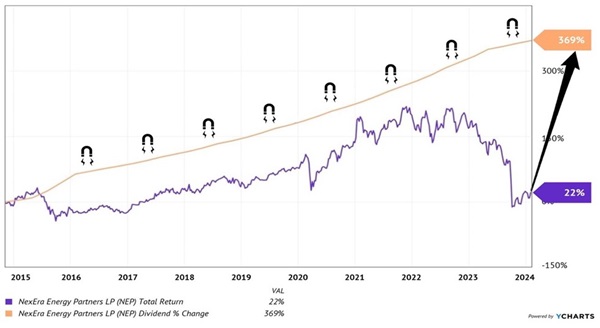

Finally, let’s give a nod to NextEra Energy (NEE) and NextEra Energy Partners (NEP). NEP was particularly bludgeoned in October, prompting a special “stay calm” alert to Hidden Yields subscribers from yours truly.

I don’t often send these types of emails and, when I must, it is typically a sign that we are near a major market low. Best to hang on and make a buy or sell decision months later after a rebound.

Well NEP has rebounded off those lows and also rewarded our patience with a dividend raise that will be paid on Valentine’s Day.

Which keeps the company’s insane streak of raising its dividend every single quarter since 2014 alive. That’s 37 in a row. And again, we’re talking quarters. Not years. Every three months.

Is This Stock Due, or What?

Oh, the irony! The “reason” NEP sold off so furiously last year was that armchair observers feared a dividend cut. But today management wouldn’t be boosting if they believed their dividend math was bad. Somebody call a cop because this 11.8% payer is a real steal here.

Same goes for NEE, which only yields 3.2%, but is a steadier stock than its dramatic child NEP.

That said, this is a compelling setup to go long dividend drama, especially in the utility sector. With long rates on the decline, scary debt loads are quickly becoming quite manageable. Let’s grab these utility dividend deals before Wall Street wakes up!

Beyond these utilities, I like this safe “toll bridge” stock that is yielding a sweet 7.3% and likely to raise its payout further in the years ahead. The details are in the February edition of Contrarian Income Report.

Unfortunately, I just checked my notes and we don’t have you as a current subscriber. No problem, you can sign up (or resubscribe) and receive my #1 income investing secret right here.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Enter your email address and we'll send you MarketBeat's list of seven best retirement stocks and why they should be in your portfolio.

Get This Free Report