Election. Recession. No landing. Social unrest. Election contest.

Low beta, anyone?

Today we’ll talk calm in a sea of manic. A six-pack of tranquil dividend payers yielding up to 8.9%.

How do we know they’re tranquil? Beta, baby.

A stock with a beta above 1 is considered more volatile than “the market.”

A stock with a beta below 1 is considered less volatile.

Let’s say a stock had a beta of 0.5. This means it’s half as volatile as the market. If a 30% bear market swipes, this safety stock only loses 15%.

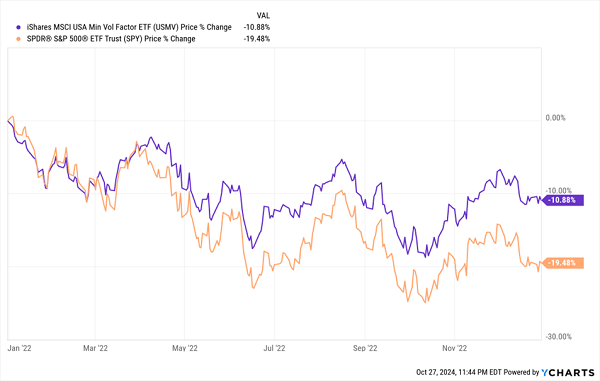

It’s an inexact science—I wouldn’t build projections per se around current beta. But, directionally, it works. Low-beta stocks tend to offer protection during downturns. Let’s review how one popular minimum-volatility ETF fared against “the market” during the bear market of 2022.

USMV: Only Half as Bad

Can we take low beta and make it better? Of course. We want companies with sustainable business models. We also want to collect meaningful dividends while we hunker down.

Let’s see which of these six low-beta stocks, which offer fat payouts of between 5.3% and 8.9%, fit the bill.

Some Old Friends

Several low-beta stocks pop up on my radar on a regular basis—a good sign that they’re maintaining their low-vol ways. I’ll take a quick look at a few of these first:

Northwest Bancshares (NWBI, 5.9% yield): This is the holding company behind Northwest Bank, a regional bank that operates 131 full-service community centers in Ohio, Pennsylvania, Indiana and New York.

Regional banks feel a little hoppy at times (SVB’s 2023 collapse pressed that into our heads), but they’re often no more volatile than the rest of the market. But NWBI is far less volatile than regionals and the market alike, boasting one- and five-year betas of 0.28 and 0.61, respectively. You can thank a sterling balance sheet, as well as a deep positioning in lower-risk loans across many more rural locales. And a yield of nearly 6% is enough to give most investors patience.

In theory, there should be some growth potential—the business boasts a number of specialized lending programs, including sponsored finance, equipment finance, and SBA loans. But profits seem to have peaked in 2021; even after a blowout Q2 raised expectations for the next two years, profit estimates still work out to down or flat compared to 2022. Unfortunately, I think that means the dividend—which is decently covered but also hasn’t budged since 2021—will remain unmoved.

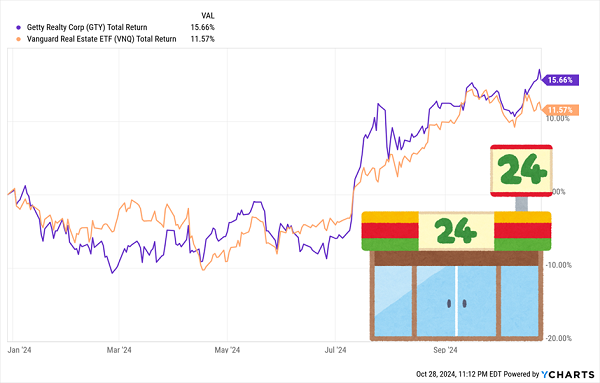

Getty Realty (GTY, 5.8% yield): That’s not a concern at Getty Realty, which is fresh off a 4.4% hike to its payout, continuing a dividend-growth streak going back more than a decade.

This real estate investment trust (REIT) owns more than 1,100 freestanding (read: single-tenant) retail properties in 42 states and the District of Columbia. I know it’s tough to trust brick-and-mortar retail, but it’s the type that matters: 63% of annualized base rent comes from convenience stores, followed by car washes (21%), legacy gas and repair (8%), auto service (6%), and a smattering of auto parts, drive-throughs and others.

Third-quarter occupancy was 99.7%, and collections were at 100%. Getty likely won’t need any funding for at least 12-18 months. It raised its full-year adjusted funds from operations (AFFO) expectations.

Stability is the name of the game here. That’s further cemented with a well-covered dividend and low one- and five-year betas of 0.25 and 0.94, respectively. And it’s outperforming the REIT sector this year to boot.

Low Volatility and Great Returns? That’s Convenient.

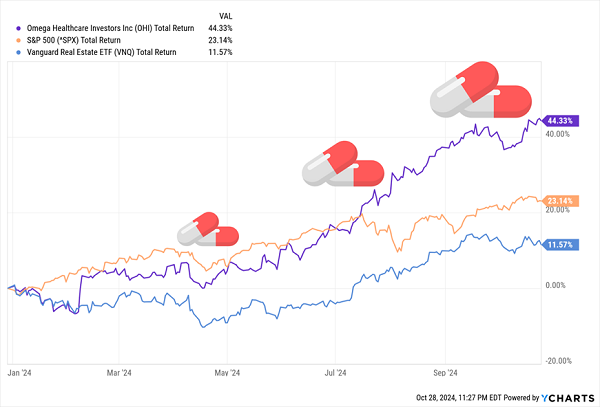

Omega Healthcare Investors (OHI, 6.3% yield): Omega, another REIT, provides financing and capital solutions to skilled nursing facility and assisted living facility partners. It’s also an oddball, beta-wise. Its five-year beta is 0.99, putting it almost on par with the market. But its one-year beta is negative 0.17.

In theory, that means when the market zigs, OHI actually zags, albeit by just a little. In practice, though, OHI has simply marched to the beat of its own drum—a good thing, in this case.

Low-Beta Omega Has Been Delivering That Alpha

I mentioned a few months ago that while OHI is operationally on the mend, the real impetus behind shares has been the interest-rate story. As expectations for the Fed’s first rate cut of the cycle grew—and became reality—so too did enthusiasm for rate-sensitive stocks like Omega.

I’ll put a little more enthusiasm behind the mend. Lower rates are indeed reducing OHI’s costs of debt and equity, and Medicare/Medicaid reimbursement is above trend. Growth expectations are rising.

The stock’s on the pricey side, though, at 15.5 times FFO estimates.

Dividends on “The House”

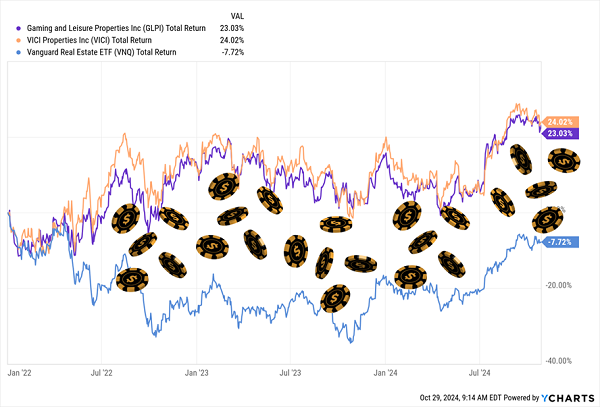

Gaming and Leisure Properties (GLPI, 6.0% yield): Yes, yes, what’s more chancy than a casino stock? But GLPI isn’t a casino stock. That is, rather than being a casino operator, it’s a REIT—a rent collector—boasting 65 casino- and gaming-related properties across the U.S. It’s also a triple-net lease REIT, which means its leases are net of maintenance, taxes, and insurance. That results in more stable, predictable income streams, which GLPI uses to fund its generous and growing dividend.

Its five-year beta is about on par with the market, at 1, but it has an extremely low one-year beta of 0.32, meaning it has been about a third as volatile as the S&P 500 in that time.

VICI Properties (VICI, 5.3% yield): There’s a similar argument to be had with VICI Properties, whose real estate portfolio includes 54 gaming facilities—including Caesars Palace Las Vegas, MGM Grand, and the Venetian Resort Las Vegas—as well as 39 non-gaming experiential properties. Same deal as GLPI: They’re collecting rent, and they’re doing so on that stable triple-net basis. Volatility is similar, too, at 0.35 and 0.96 one- and five-year betas, respectively. And the dividend has been rising for years as well.

Hasn’t Felt Like a Gamble: A Much Smoother REIT Ride for Years

Low-Beta Dividends in Energy?

Chord Energy (CHRD, 8.9% yield): You won’t often see traditional energy operators in a list of high-yield, low-beta plays. But this independent oil-and-gas producer, which operates in the Big Sky’s Williston Basin, is quite the exception, boasting a 5-year average beta of 0.83, and a one-year of 0.71.

Chord added to its size and scale earlier this year, when it completed a merger with Canadian E&P Enerplus, which brought with it a raft of high-quality Bakken Shale assets. It has also brought higher expectations for cash flow not just this year but next, which could result in both a quicker pace of buybacks (CHRD is currently working off $750 million buyback authorization) and better dividends.

The dividend effect is much more direct here, too. That’s because Chord has a fixed-plus-variable payout. CHRD automatically pledges $1.25 per share per quarter, which comes out to a decent 4% on its own. But those variable payouts over the past four quarters have added up to nearly 5% in additional yield!

The One 12% Dividend to Own Now

Secure dividends are the ultimate safety net—they’re cash in your pocket, right here, and right now, no matter whether your tickers are flashing green or red.

The dividend stocks above provide a lot of market cover even at single-digit yields.

So just imagine what kind of protection against volatility you could get from a 12% dividend.

My One 12% Dividend to Own Now is a rare machine capable of generating a simply ludicrous amount of cash. A 12% yield, in the most practical terms, is:

- $1,000 a month from a mere $100,000 investment

- $60,000 a year—a proper salary in many parts of the U.S.—from a mere $500,000 nest egg

- A wild $120,000 annually if you have a million bucks to put to work.

Paid out for sitting around and doing nothing but waiting.

That kind of money doesn’t just buy you things.

It buys you comfort. It buys you peace of mind. It buys you a regular good night’s sleep—where you stop wondering and worrying about which way the market’s winds will blow next.

It could even buy you the ability to live off of dividends alone, without ever laying a finger on your nest egg.

But you don’t have much time. If you miss the deadline to get on the list now, in a few days, you could be leaving money on the table—and might not be able to lock in this 12% when the next distribution comes around.

Click here, and I’ll tell you all about this monster 12% yield, its growing payout, and its special dividends!

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Almost everyone loves strong dividend-paying stocks, but high yields can signal danger. Discover 20 high-yield dividend stocks paying an unsustainably large percentage of their earnings. Enter your email to get this report and avoid a high-yield dividend trap.

Get This Free Report