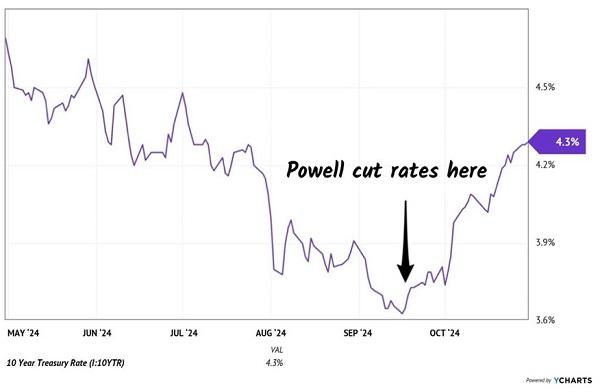

The Federal Reserve cut interest rates by an “historic” 50 basis points. Then, interest rates soared.

Wait. What?

The Federal Funds Rate is a target (technically a target range) that influences short-term rates in the economy. Money market funds, for example, pay interest based on this benchmark. They pay 0.5% less today than two months ago due to the Fed cut.

Long-term rates, on the other hand, are not controlled by the Fed. Not directly, at least. The global bond market is a cool $130 trillion. Far too large for anyone, even Uncle Sam, to control.

Hence the recent fixed-income paradox. Fed Chair Jay Powell cut rates by 50 basis points, but the bond market didn’t buy his explanation.

How can you be so dovish, Jay, when the economy is doing fine? Your accommodation will result in inflation. So, apparently, we need to ask for more interest over a 10-year period.

Fed Cut Sends the 10-Year Rate Higher

How can the economy be humming like this after such a sharp rate hike cycle? Haven’t we been hearing about an impending recession since the summer of 2022?

The “dark matter” in recent bearish miscalculations has been the government’s deficit spending. It is completely out of control. And someday there will be a wicked hangover—but for now, we have a booming economy party.

Debtors love inflation (the real value of their debt declines!), and Uncle Sam is showing no shame. For fiscal 2024, the Congressional Budget Office (CBO) projects a $1.9 trillion deficit on $4.9 trillion in tax receipts. And yes, this is the CBO that paints its projections with rose-colored ink.

So, we have nearly $5 trillion in revenues and almost $7 trillion in expenditures. A 40% overshoot.

Which means long rates should continue higher from here, right?

Not so fast, my friend!

Decorated economist Nouriel Roubini recently published a new paper citing “activist Treasury issuance” (ATI) as the favorable plumbing adjustment:

Roubini found that the US Treasury is, shall we say, finessing debt issuance to guide longer-term rates lower than they otherwise would be. Thanks to ATI, the 10-year Treasury yield is 30 to 50 basis points lower than it otherwise would be.

He calls it “stealth QE.” In these pages, before Roubini’s paper, we called it quiet QE.

Tomato. To-mah-to.

The bad news is that the 10-year should be even higher, closer to 5%. The good news is that the Federal government is “on our side” so to speak. The bond market is too big to be controlled, but it can be swayed for a while.

(Now, as a free market guy, I don’t condone this type of meddling. I only ask that when the Feds do interfere with long rates, they help buoy our beloved bonds. Ha!)

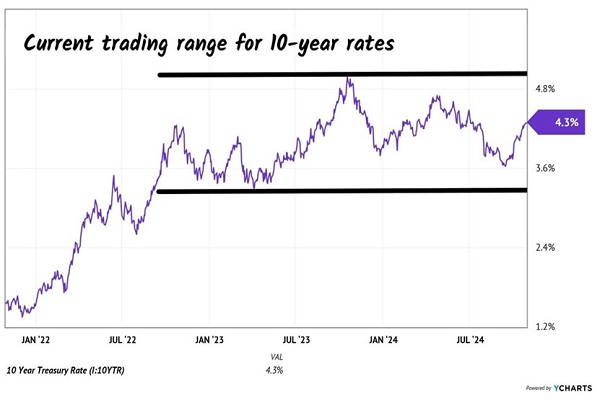

Let’s put the recent rate spike in perspective. Big picture, there’s nothing to see here. We have been rangebound for the past three years. Rates have rebounded after an extended drop. This is what markets do. They fall, then rise. Zag, then zig.

Putting the Recent Rate Rise in Perspective

If we assume that this too shall pass (thanks for that wisdom, Abe Lincoln!), we careful contrarians should hit the bond bargain bin. DoubleLine Yield Opportunities Fund (DLY) looks particularly attractive here.

DLY (called “dilly” inside the halls of DoubleLine) yields 8.7%. That’s double the current 10-year rate, and a nice buffer against price declines if yields on Treasuries continue to rise. (Bonds may trade opposite rates in general, but 8.7% is an elite yield, period.)

Here’s where guys like DoubleLine’s famous founder Jeffrey Gundlach find alpha. Three-quarters of DLY’s bonds are below investment grade or not rated. This would make us nervous were Gundlach not our assigned shopper.

“Shopper?” OK. There are great deals to be had below investment grade because, for example, pensions—the biggest buyers of bonds—aren’t allowed to own this paper. Issuers of these bonds approach Gundlach first to buy them (as business sellers often start with Buffett).

So, we benefit not only from deals others don’t see, but also the ones he thinks are the best. We can trust the picks that Gundlach puts in this CEF cart. It’s where the values are in Bondland, and ETFs and mutual funds are not flexible enough to take advantage of these deals.

We’ll let the vanilla investors have their interest rate worries. We contrarians will gladly take the 8.7% yield.

Best thing about DLY is that it pays monthly. Solid monthly dividends are difficult to find, but thanks to the recent “Fed cut, rates rise” paradox we have more 8%+ monthly dividends staring us in the face.

Don’t put all your eggs into the DLY basket! Diversify and retire on dividends with these 8%+ yields paid monthly.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Discover the 10 best stocks to own in Spring 2025, carefully selected for their growth potential amid market volatility. This exclusive report highlights top companies poised to thrive in uncertain economic conditions—download now to gain an investing edge.

Get This Free Report