If you haven’t noticed, I’m a bit of a data nerd. I could go on and on about all the economic numbers I watch for you every month, but these weekly articles just don’t give me the room. So I have to be selective.

There are hundreds (I’m not exaggerating; I’m up to 157 so far) of data points that prove the US economy is doing better than most people think, and that 2022’s doom-and-gloom was way overdone (and in many cases plain wrong).

Unfortunately, my editor would never let me cover all of them, especially in one article! And, let’s be honest, most people wouldn’t want to sit through 157 data points, either.

So let me quickly throw three at you, because they go straight to the reasons behind our bullishness on equity and bond-focused closed-end funds (CEFs) at CEF Insider today.

Then we’re going to talk CEFs—including an 8.7% payer holding shares of America’s strongest companies—because these high yielders are our favorite way to tap America’s economic strength.

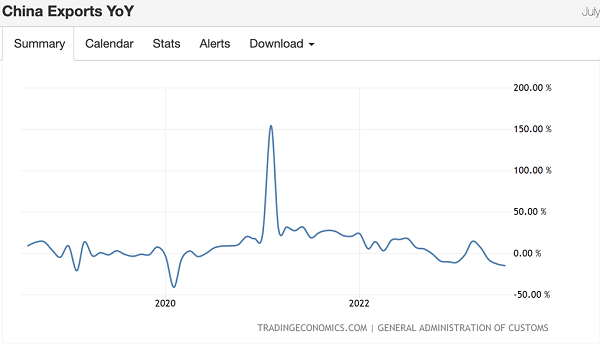

Bullish Data Point No. 1: The US Has Cut Loose a Sinking China

Most people wouldn’t see news about a collapse in China as good for any economy. After all, in a globalized world, what’s bad for America’s trading partners is generally bad for America. Except America isn’t really a major trading partner to China anymore.

COVID-19 resulted in a long (and well-documented) scramble from virtually every company in America to buttress, diversify and reinforce supply chains to make them less reliant on one region or country. The US, for example, ran out of personal-protective equipment in 2020, when some other countries had a surplus—companies won’t let that happen again.

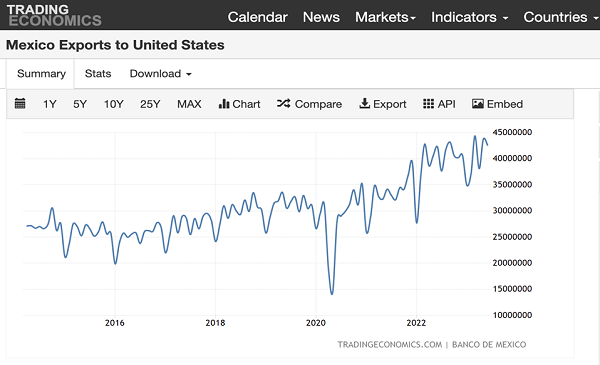

Meanwhile, exports from Mexico to the US have surged to $42.6 billion per month, up nearly 70% from before the pandemic.

China’s export decline tells us that worries about the country’s economic woes hurting the US haven’t come true. And they’re not likely to, with Mexico displacing Chinese exports to the US—a trend that’s likely to continue (not to mention the trend of companies simply moving their operations back to the US).

That shift, and the added stability it brings, is great news for US stocks.

Bullish Data Point No. 2: Flow of Cash Into Bonds Is a Good Sign for Growth

Today’s high interest rates make it hard for companies to borrow money to expand. That’s the conventional wisdom, and it’s not wrong. But it’s only half the picture.

To be sure, a lack of access to credit can cause a recession. But not only are companies doing fine, they’re still borrowing at high levels and earning a profit on those borrowings in the vast majority of cases.

But let me offer some reassuring data: BlackRock, the world’s largest investment manager, saw $68 billion flow into its iShares bond ETFs in the first half of 2023, and BlackRock president Rob Kapito says he expects more of the $7 trillion parked in money-market funds to flow to bonds, too.

This means that as more investor money flows into bonds, yields will fall—it’s simple supply and demand. That, in turn, will lower the cost of borrowing for bond issuers. This will happen organically—not due to any action from the Fed. So as long as money keeps flowing into bonds, companies will have more access to capital to expand, another plus for US bonds (and stocks).

Bullish Data Point No. 3: US Wages Are Outrunning Inflation

Consumer spending drives the US economy, and the knock-on effects of this spread across the globe.

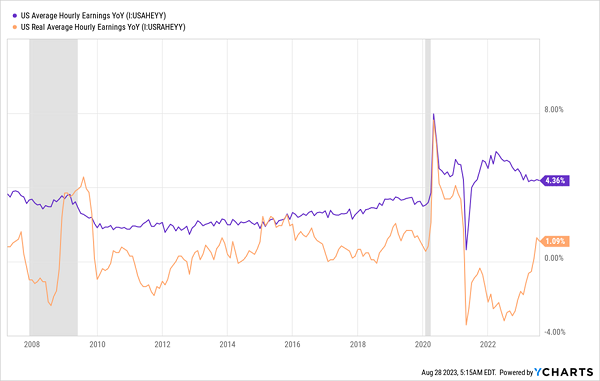

True Spending-Power Growth

The purple line above represents average hourly earnings growth in America—that headline number is strong. The orange line represents growth after inflation, which is key to determining whether American consumers are doing better or worse. When it’s above 0, they have more purchasing power.

That number collapsed in 2022, which was a key reason why stocks tanked. But now that hourly earnings growth is beginning to eclipse cost-of-living growth, that trend is gone, and it’s time to buy stocks while they’re still oversold—and they are, given that the S&P 500 is still well below its late-2021 peak.

Stocks Still Oversold

An 8.7%-Yielding CEF That’s Perfect for This Unloved Bull Market

This is where CEFs come in, because we don’t just want to buy the S&P 500 and be done with it. This is a weird time in markets—we went from all of our financial models collapsing three years ago to seeing unpredictable moves for two years until, all of a sudden, the models started working again.

If they start to collapse again, we could see a short-term selloff as people have flashbacks to last year. That would, of course, be a long-term buying opportunity.

So we need exposure to undervalued stocks and the liquidity that comes from big dividends, and CEFs are a great way to get both—especially CEFs like the Eaton Vance Risk-Managed Diversified Equity Income Fund (ETJ). Its portfolio has no surprises—Microsoft (MSFT), Apple (AAPL), Amazon.com (AMZN) and Mastercard (MA) are all top holdings.

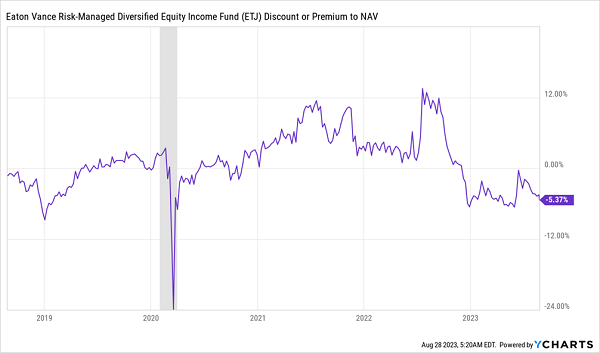

Here’s the best part: through ETJ, we can get all these stocks at a discount to their market prices.

This is weird; ETJ typically sells for more than its portfolio’s intrinsic value, and in fact its discount to net asset value (NAV, or the value of the stocks in its portfolio) has dropped in recent weeks, retreating to its early 2023 level:

ETJ’s Discount Suddenly Widens

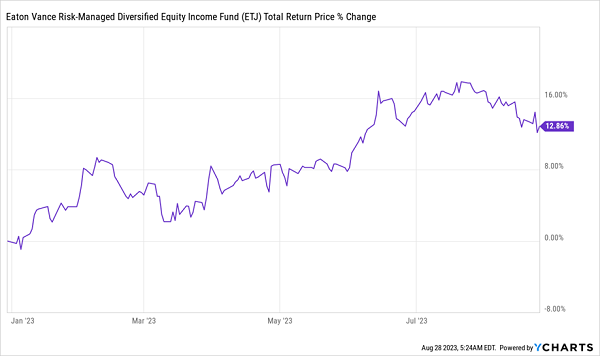

This might sound startling, but ETJ is up solidly this year, thanks to its strong stock portfolio.

ETJ Providing Profits

Plus, ETJ’s 8.7% income stream provides the cash we need to add more to our positions regularly, thanks to its monthly payouts and high yield. Reinvesting our payouts compounds our returns and gives us even bigger profits if the market ignores the data and falls in the short term.

And there are more data points that suggest that this would be a buying opportunity: used-car prices fell 4.2% year-over-year in June; job openings remain over double their 20-year average, consumer confidence has surged consistently for months … I could go on, but I can already hear my editor’s voice in my head warning me to stop!

ETJ Is a Smart Swing Trade, But These 9.5% Yielders Are Built for the Long Haul

ETJ’s discount is likely to flip back to a premium, and likely soon, given this fund’s habit of trading above its NAV. But it’s still a serial underperformer with a dividend that’s trended down in the last decade.

So while it makes sense to buy ETJ and hang on till that discount disappears, it’s not a fund I’d hold in my retirement portfolio.

For that, look to the 4 funds I’ll tell you about right here. They trade at discounts so deep I’m calling for 20%+ price upside from them in the next 12 months. And they pay out dividends averaging 9.5% that you can count on for the long term.

Click here and I’ll tell you more about these stout 9.5%+ payers and give you the opportunity to download a FREE Special Report naming all 4 of these funds.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Almost everyone loves strong dividend-paying stocks, but high yields can signal danger. Discover 20 high-yield dividend stocks paying an unsustainably large percentage of their earnings. Enter your email to get this report and avoid a high-yield dividend trap.

Get This Free Report