With the market at nosebleed valuations, where can we look for value and yield?

Let’s turn to our favorite three-letter acronym. C-E-Fs.

As usual we have a handful of closed-end funds (CEFs) getting no love from Wall Street. This is perfect for us as we’re talking about dividends up to 14% and discounts between 10% and 15%.

In other words, these fat payers are trading for 85 to 90 cents on the dollar. Let’s discuss.

Gabelli Dividend & Income Trust (GDV)

Distribution Rate: 5.8%

Discount to NAV: 15.0%

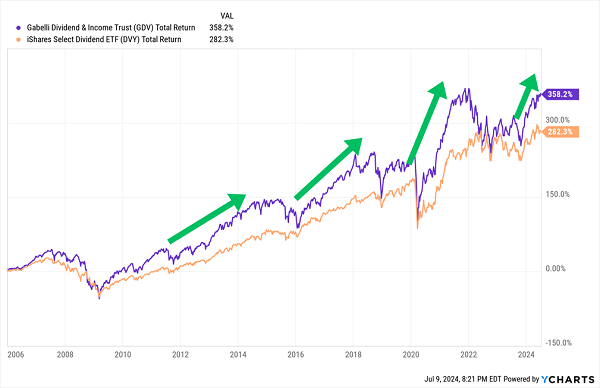

We begin with Gabelli Dividend & Income Trust (GDV), a top-rate closed-end fund whose management team includes legendary value investor Mario Gabelli.

Unlike a lot of CEFs that either deal in niche securities or put options strategies to work, GDV is pretty straightforward—it’s a straight-up equity-income portfolio that uses a modest amount of leverage (12%). But management isn’t timid. Unlike a lot of dividend funds that lean heavily toward stodgy value plays, Gabelli Dividend & Income has plenty of growth, with the likes of Microsoft (MSFT), Nvidia (NVDA), and newly minted dividend stock Alphabet (GOOGL) in its top 10 holdings.

Notice that many of these stocks don’t come close to meeting our yield requirements. But GDV comes a lot closer, delivering a nearly 6% yield currently—and it pays us monthly, too!

This is a great fund that I’ve previously flipped for a handsome profit in my Contrarian Income Report portfolio.

GDV Provides Bursts of Outperformance Over Time

And we can currently get it—and Mario’s expertise—at 85 cents on the dollar.

Kayne Anderson Energy Infrastructure Fund (KYN)

Distribution Rate: 8.3%

Discount to NAV: 10.6%

Kayne Anderson Energy Infrastructure Fund (KYN) is a “go-to” energy CEF for investors who want the big yields of master limited partnerships (MLPs) without all the headaches.

KYN provides exposure to energy infrastructure stocks across North America—predominantly midstream operators with oil, natural gas, and liquefied natural gas (LNG) infrastructure, though it also includes utilities and renewable energy plays as well. These are “toll taker” stocks that don’t necessarily need high energy prices to make a buck—instead, they just take a cut as energy flows through their assets.

If we owned these types of companies individually, we’d be saddled with a complicated K-1 package come tax time. However, when we buy them through KYN, we get a simple Form 1099 instead.

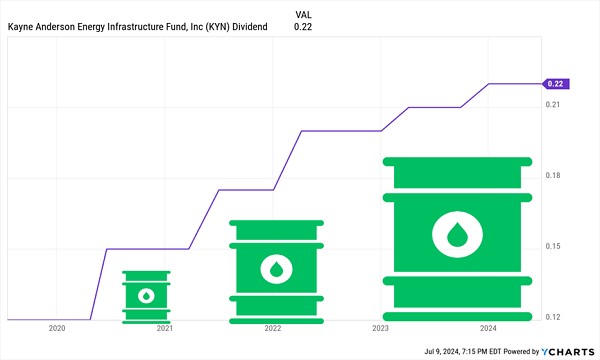

The portfolio is small—40 or so tickers, led by the likes of MPLX LP (MPLX), Energy Transfer LP (ET) and Enterprise Products Partners LP (EPD). These names provide outstanding income—income that’s on the upswing, with MLP distributions rebounding off the COVID bottom:

The Payouts Keep Getting Better

This Kayne Anderson fund amplifies that productivity with a decent amount of leverage—about 20% currently. That same leverage has made a good 2024 for MLPs even better for KYN, which has returned nearly 30% year-to-date.

That same success takes some of the luster off KYN’s discount, however. It’s still trading at a 10%-plus discount to NAV, which means we’re able to buy these assets for less than 90 cents on the dollar. But over the past five years, KYN has traded at a nearly 14% discount, on average, so one could argue this CEF is at least momentarily overheated.

MainStay CBRE Global Infrastructure Megatrends Term Fund (MEGI)

Distribution Rate: 11.7%

Discount to NAV: 10.4%

The MainStay CBRE Global Infrastructure Megatrends Term Fund (MEGI) is a different type of infrastructure CEF.

One of the differences is geographic—whereas KYN invests across North America, MEGI invests across the world.

Another is its lifespan. MEGI is actually a “term” fund that has a 12-year limited term and will liquidate either on or around Dec. 15, 2033.

But the biggest difference is MEGI’s larger scope: The fund is “focused on the investment megatrends of decarbonization, digital transformation and asset modernization, which are reshaping the demand for infrastructure assets and driving income and growth potential.”

Sure, we get some pipeline stocks in here—names like EPD and Pembina Pipeline (PBA). But we also get clean-energy plays like NextEra Energy (NEE) and Atlantica Sustainable Infrastructure (AY), communications-infrastructure property owners, data center REITs, even railway operators and satellite firms.

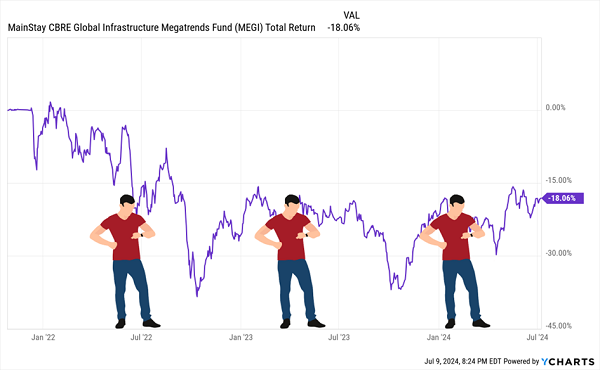

It’s a noble mandate, but MEGI has been cursed with lousy timing, hitting the markets in October 2021 just as stocks were about to top.

Investors Are Still Waiting for MEGI to “Launch”

It’s also a broad mandate—so much so that it’s difficult to recommend it for any one thematic reason. Between that and its small size, I hesitate to ever recommend it here or CIR. Instead, I keep my eye on MEGI for especially deep discounts to take advantage of in Dividend Swing Trader.

Right now, MEGI is cheap at a roughly 10% discount. But it has been much cheaper in its short history, trading at a discount as wide as 18% within the past 52 weeks alone. So we don’t own it currently, but DST subscribers will receive a Flash Alert if I see an opportunity to buy at a much better discount.

BlackRock Health Sciences Term Trust (BMEZ)

Distribution Rate: 14.0%

Discount to NAV: 13.2%

Another term fund with a wildly different aim is the BlackRock Health Sciences Trust II (BMEZ).

This healthcare-minded CEF, which started in 2020 and will liquidate on or around Jan. 29, 2032, holds a number of biotechnology and health-science firms—companies such as biotech giant Amgen (AMGN), robotic surgical specialist Intuitive Surgical (ISRG) and West Pharmaceutical (WST), which makes pharmaceutical packaging and delivery systems.

Of course, as anyone who has ever owned a plain-Jane healthcare ETF knows: We don’t get a 14% yield from owning pharma and biotech. Oh, we can find some decent dividends. But double-digit yields? Hardly.

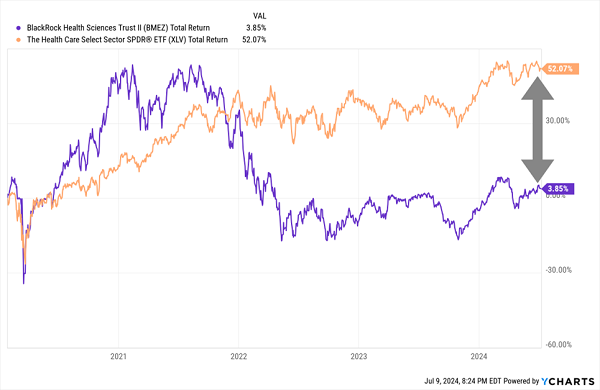

Unlike some of the other CEFs mentioned here, BMEZ’s sky-high yield doesn’t come from leverage—it comes from the fund’s ability to sell covered calls to generate income.

Unfortunately, this strategy has failed to capture anywhere near the upside of plain-Jane funds over the past few years.

BMEZ Hasn’t Unlocked Healthcare’s Potential

Even since bottoming out in mid-2022, the fund has trailed the broader healthcare sector by a few points. Effectively, all it has done has shifted its returns from price performance to dividends. That makes its 13% discount to NAV—which is roughly where it has stood for much of its publicly traded life—much less alluring.

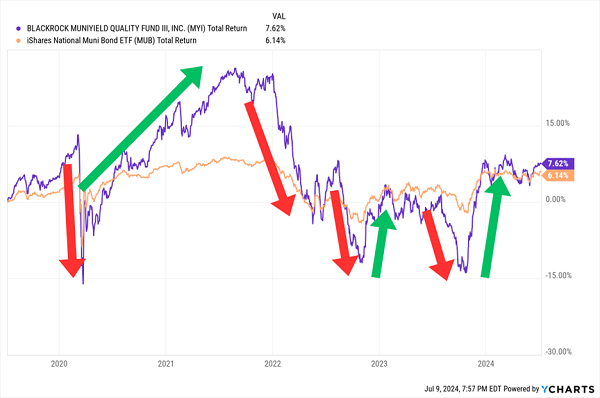

BlackRock MuniYield Quality Fund III (MYI)

Distribution Rate: 5.8%

Discount to NAV: 9.9%

The BlackRock MuniYield Quality Fund III is one of a trio of BlackRock funds that aim to hold high-investment-grade municipal bonds.

Municipal bonds are issued by state and local governments to fund infrastructure projects. Their headline yields are often lower than bonds of similar quality, but their income is exempt from federal taxation, and possibly even state and local taxes depending on where the investor lives. So while MYI’s yield of 5.8% might be less than traditional bond CEFs, someone in the top tax bracket would need a roughly 10% yield from a taxable bond to collect the same amount of post-tax income.

This portfolio of nearly 300 muni bonds are predominantly long-term in nature—about 80% of assets are wrapped up in debt that matures in 15 years or more. MYI’s credit quality is outstanding, with nearly 80% of holdings rated A or above. (Interestingly, MYI has a weaker credit-quality mandate than its sister funds, MQT and MQY, which are designed to hold “the three highest quality rating categories (A or better) or, if unrated, of comparable quality,” but it currently has the strongest portfolio, with a higher proportion of AA- and AAA-rated debt.)

It’s a decent CEF, it pays a nice monthly yield, and it’s trading at a slightly fatter discount than its lifetime average. But it’s also a fund that—thanks to very high leverage (37% currently)—experiences much more volatile swings than indexed municipal-bond funds.

MYI: A Lot of Movement to Get to the Same Place

The Bond Bull: 3 Funds Yielding Up to 12% With Massive Upside Potential

Let me be clear: We want to be positioned in bonds.

We just don’t want to do it through MYI.

The bond market has been pulverized in recent years, with many bonds getting slashed by 50% or more—on par with the Dot-Com Bubble bust and Great Financial Crisis!

But fixed income has recently shown flickers of life—a quick reversal that could signal the start of a new “bond bull.”

I’m making moves to make the most of this potential bull run in bonds. But I’m not targeting MYI, which is a “B” bond fund that’s better suited for quick swing trades.

Instead, I’m positioning myself into three funds that not only deliver fat yields of up to 12%, but have massive upside potential, too.

Bonds are throwing off their highest yields in more than a decade! The “Agg” index, with a yield of around 4.3%, is paying more than 4x what it did just three years ago.

The Fed has signaled multiple rate cuts—and as you know, when rates head lower, bond prices head higher.

So right now, we have a rare chance to lock in uber-high rates before they disappear, and set ourselves up for price upside when bonds pick up steam. It’s a powerful 1-2 punch most investors don’t think about when it comes to the bond market!

I’m not the only one who has noticed, either. Capital Group, Pimco, BlackRock … all of Wall Street’s big names, collectively managing trillions of dollars, are starting to notice the potential for a sea change in the coming months.

If things go the way the Fed, the biggest investment firms and I think—well, astute investors can make a boatload of money in the bond market.

Click here to learn how to ride the coming “bond bull”! You can download a FREE Special Report revealing 3 funds yielding up to 12%.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Which stocks are likely to thrive in today's challenging market? Enter your email address and we'll send you MarketBeat's list of ten stocks that will drive in any economic environment.

Get This Free Report