This week, we’re going to pick up some rich 8%+ payouts alongside … Taylor Swift?

You read that right. Turns out the favorite singer of everyone from, well, my two daughters to the attorney general of the United States is a fan of our favorite income plays: closed-end funds (CEFs).

That news broke in the form of a tweet from billionaire investor Boaz Weinstein, head of Saba Capital Management. Weinstein apparently heard from Swift’s dad (who used to work for Merrill Lynch) that the singer does, indeed, hold CEFs.

“Having a blast watching our daughters sing every lyric tonight in Philly,” Weinstein tweeted. “Did you know that @taylorswift13 invests in discounted closed end funds? You think I’m kidding, but her father, Scott, told me so!

In some ways, that’s no surprise. Swift has long been known to be a canny financial operator. She was, after all, one of the few celebs who saw the FTX crypto mess coming a mile off, refusing to endorse it while others—Larry David, Tom Brady and even business “expert” Kevin O’Leary among them—got pulled in (and are now facing a class-action lawsuit).

But even so, CEFs are a pretty obscure corner of the market, even for a savvy investor, with only 500 or so out there. But Swift apparently knows the score: as Weinstein says, she not only buys CEFs, but focuses on CEFs trading at a discount to net asset value (NAV).

We contrarians agree—so much so that your income strategist wonders if Swift has been browsing the pages of Contrarian Income Report.

We’ve long panned the idea of buying CEFs at a premium. So we never, ever, ever do it. (Sorry, couldn’t resist!) But buying at a discount sets us up to “ride along” as that deal disappears, propelling the CEF’s price toward the fund’s NAV as it does.

The CEF Discount Window Is No “Blank Space” to Swift

And while we wait, we pocket a rich dividend, too. These days, payouts north of 8% are common in the CEF world.

Weinstein, who you may remember made a fortune back in the mid-2010s betting against the JPMorgan trader known as the London Whale, is a fan of CEFs, too. Here’s what he had to say about these funds back in 2017:

“You go into it hoping the discount will narrow on its own, but one of the nicest points about this investment is that while you wait, you earn an above average yield, given the discounted price.”

That’s one of the best quotes I’ve ever seen on the power of CEFs. But it is missing one detail: buying CEFs at a discount alone isn’t quite enough—you need to look at the discount as it relates to its historical pattern.

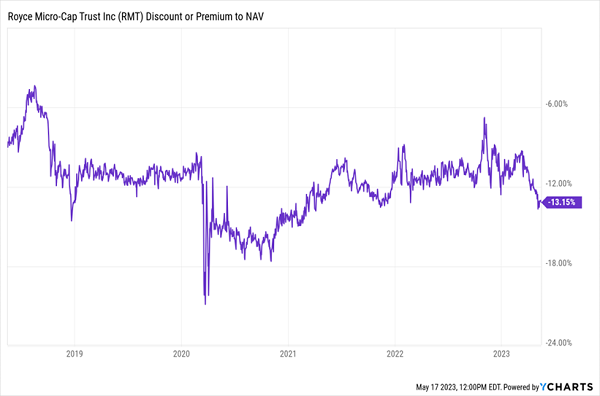

After all, a deep CEF discount is no good if management has no plan to close it. Which is why we want to avoid CEFs that are always cheap, like the Royce Micro-Cap Trust (RMT), which sports a 13% discount to NAV and yields around 9%.

Trouble is, RMT always trades at a discount—and that discount has actually gotten wider over the last five years:

We Knew RMT Was Trouble

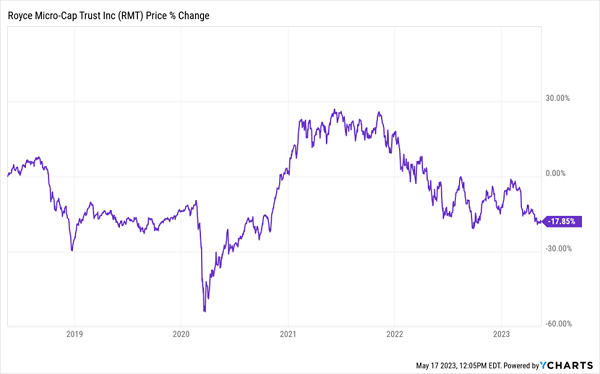

That falling discount has been a lead weight on RMT’s market price. Sure, RMT investors have pocketed a 23.5% return, but that’s less than half the S&P 500’s 65%. And even that 23.5% is entirely because of the dividend. On a price basis, RMT is down significantly:

RMT’s Price Can’t “Shake Off” Its Eternal Discount

That’s why we want to see management with a plan to close a CEF’s discount. This way we have two ways to win (three when you include CEFs’ high dividends!):

- NAV gains, from the appreciation of the CEF’s portfolio, and ..

- Closing discounts, which we can see as a kind of afterburner, giving our returns an extra lift.

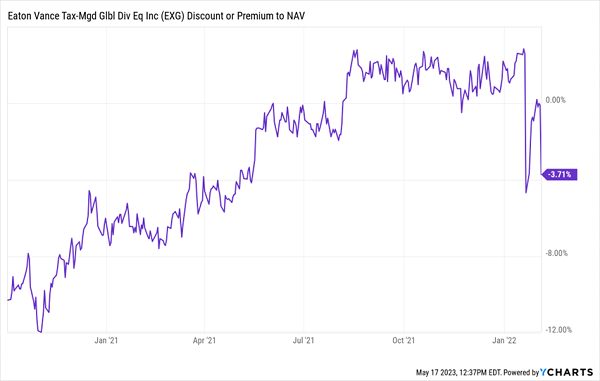

The Eaton Vance Tax-Managed Global Diversified Equity Income Fund (EXG), holder of large caps like Apple (AAPL), Amazon.com (AMZN) and Coca-Cola (KO), is a terrific example of a closing discount in action.

From the time we added it to our Contrarian Income Report portfolio in October 2020 until we sold in February 2022 (just sidestepping the market dumpster fire that was to come), EXG’s discount narrowed from around 10% to 3.7%, driving a 28% gain in the share price in just under a year and a half:

EXG’s Discount Window Slams Shut …

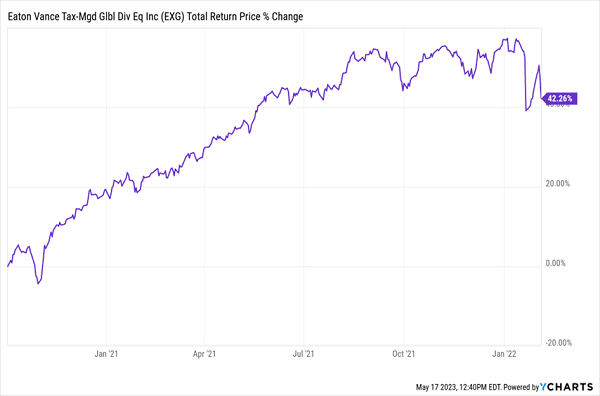

There was more. Because in addition to its portfolio gains and the upside from its closing discount, EXG rewarded us with dividends during our holding period, to the tune of $1.03 for every share held, essentially “paying back” 14% of the $7.51 per share we paid for the fund.

The end result: a quick total return of just over 42%!

… and Delivers a Rockstar Return for CIR Members

The best part is that you don’t have to be rich to profit from CEFs. Like Weinstein and Swift, we can pick up discounted CEFs on the open market and start tapping their 8%+ dividends (often paid monthly) straight away.

Publisher’s Note: These High-Yielding CEFs Win 90% of the Time

Kevin Wallen here. I’m the publisher of Contrarian Outlook.

I’m breaking in on Brett’s article here to tell you something else few folks know about CEFs: the oldest of the bunch—those that have been around for 10 years or longer—have only lost money 10% of the time!

That’s an incredible stat. And when you focus on well-established CEFs with big, safe dividends and big discounts, you tilt the odds even more in your favor.

This is why I like to call CEFs “lifetime profit plays.” You can buy the best ones and hold them for the long haul, collecting big dividends while waiting for their discounts to disappear—and their prices rise.

Wealthy investors clearly know it. And to help you profit alongside them, our CEF pro, Michael Foster, has put together a brand new presentation to give you the full story on CEFs’ remarkable reliability.

Click here to read his exclusive briefing and learn how to unlock his Special Report revealing his top 5 bargain-priced CEF picks to buy and hold for the long haul (and collect big cash dividend payouts while you do).

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Discover the 10 best stocks to own in Spring 2025, carefully selected for their growth potential amid market volatility. This exclusive report highlights top companies poised to thrive in uncertain economic conditions—download now to gain an investing edge.

Get This Free Report