With 2022 likely to be a wild ride, we income investors are going to lean on two key advantages. In doing so, we’ll secure 7% dividends no matter what the broader markets do.

First, we can secure this “head start” by January 1 by purchasing funds that yield 7%, on average. And these aren’t risky payouts, by the way. I’m talking about secure dividends funded by real cash flows.

And secondly, we can buy them from the bargain bin for just 90 or 95 cents on the dollar! That’s better than most investors, who pay full price (or more!) for their stocks. Yikes.

We won’t find these deals—or really any discounts—in popular stocks right now. Fortunately, we have the ability to type in little-known tickers that represent the best dividend vehicles on the planet.

The closed-end fund, or CEF for short.

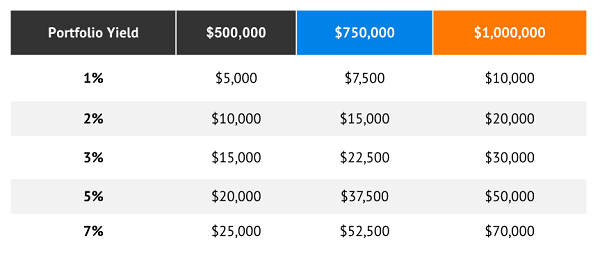

Most mutual funds and ETFs yield between 1% and 3%, give or take. Even at the high end, we’re talking about an annual income stream of just $30,000—and that’s if we have at least a million bucks to play with.

CEFs pay more. And when we buy them at discounts, they charge less! CEFs often pay 7% or better. This makes a big difference when we’re talking about retirement income on a million dollars:

The Only Funds We Can Buy on Sale

There’s no overstating the income potential of CEFs, but they boast another leg up on their more popular cousins:

We can get them at a discount.

Unlike mutual funds and ETFs, closed-end funds have a limited number of shares. That means that when markets panic, they can (and often do) trade at a discount to their net asset value (NAV). Let’s take a fund trading at a 5% discount to NAV: That means we’re effectively buying all the stocks and/or bonds inside for 95 cents on the dollar!

Think about it: Not only can we benefit from the inherent growth of the fund’s holdings, but we can enjoy additional value upside, too—just like we would with an underpriced stock—and high dividend yield to boot!

So, let’s get ready to make some game-changing moves that will put us on the right foot not just for 2022, but well beyond. Let’s quickly look at 22 CEFs that offer up yields of at least 5.4% but up to an astounding 36.5%, and trade for less than their assets are worth.

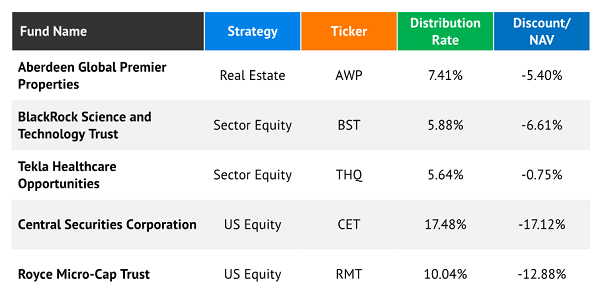

U.S. Stocks: Go Above and Beyond the Basic Index Fund

Source: CEF Connect

Instead of investing in, say, an S&P 500 tracking fund, or a sector ETF like the Technology Select Sector SPDR Fund (XLK) or Vanguard Real Estate ETF (VNQ), we can do the same thing via CEFs and juice our income by several times over.

Take BlackRock Science and Technology Trust (BST), for instance. This CEF stands out in part because of a stellar payout that yields nearly 6% at current prices. But another part of the appeal is how BST is run.

Like just about every other CEF, this is an actively managed fund whose portfolio generally looks like a broad tech offering. Its 125 holdings include the likes of Apple (AAPL), Microsoft (MSFT), Marvell Technology (MRVL) and Dutch chip firm ASML (ASML). But BlackRock Science and Technology Trust also can (and does) invest some of its assets in private placements—companies we simply can’t access right now via a basic index fund.

On top of that, BST puts options strategies to work, employing covered calls to help reduce volatility and generate income.

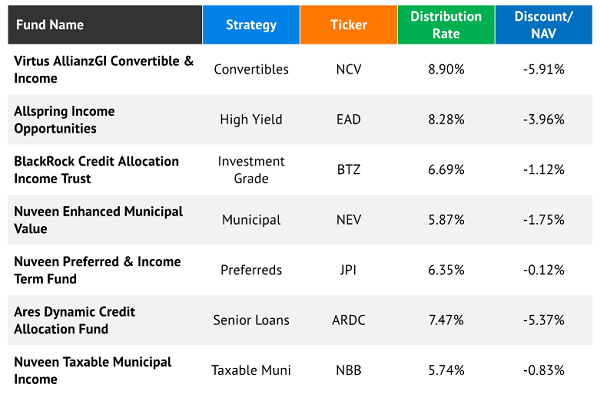

Fixed Income: These Bonds Aren’t Boring

Source: CEF Connect

Closed-end funds are also a fantastic way to get fixed-income exposure, especially in a low-rate environment like this.

The iShares J.P. Morgan EM High Yield Bond ETF (EMHY) is one of the most aggressive bond ETFs I can think of. This fund pairs junk debt and emerging markets such as Turkey and Mexico, and it squeezes a fat 5.8% yield out of that.

We can do better with CEFs. In fact, we can secure the same type of yield out of tax-free municipal bonds, and even more substantial income once we get into junk and convertible funds.

Let’s consider the Nuveen Enhanced Municipal Value (NEV). This fund holds about 260 municipal issues, from health-system revenue bonds to general obligation debt. Credit is utterly unremarkable—almost 80% of its portfolio is investment-grade, so it’s not sacrificing quality to offer up big income.

However, unlike an ETF or a mutual fund, Nuveen’s NEV can put debt leverage to work. The fund currently has 33% leverage in use, allowing management to put even more money to work in their top picks.

And most of that 5.8% yield—paid monthly, no less—is bond income, meaning it’s free of federal tax obligations. If we’re in the top tax bracket, we’re receiving a tax-equivalent yield of 9.2%!

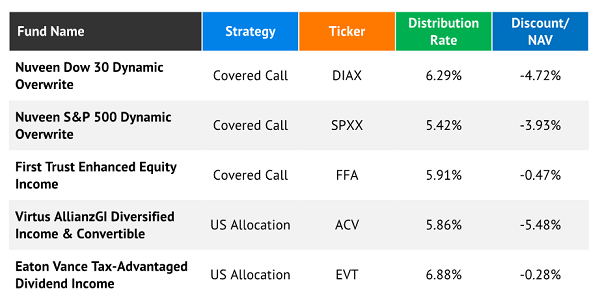

The Oddballs: Alternative Strategies

Source: CEF Connect

This penultimate cluster of CEFs is made up of two groups of funds: covered call strategies and “allocation” funds (read: stocks and bonds together).

Nuveen S&P 500 Dynamic Overwrite (SPXX), for instance, invests in about 300 S&P 500 holdings to somewhat mimic the index’s performance. It then sells covered calls against its equity holdings to smooth out performance and generate more income. That’s one way to get Meta Platforms (FB) and Alphabet (GOOGL) to pay us 5.4%!

Eaton Vance Tax-Advantaged Dividend Income (EVT), meanwhile, is a “portfolio in a can.” The asset mix at the moment includes 75% in U.S. equity, but also 8% in investment-grade debt, 7% in preferreds, 6% in junk bonds, and sprinkles of foreign stocks, convertible debt and cash. And incredibly, this diversified portfolio still yields nearly 7%.

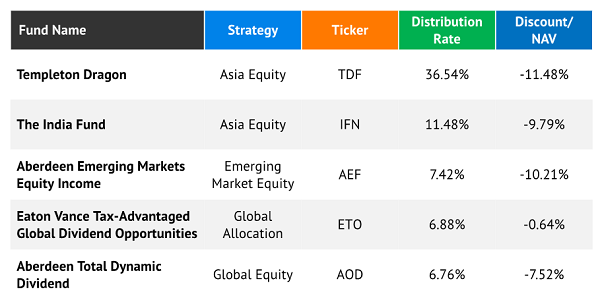

International Funds: Ignore Them If You Hate Money

Source: CEF Connect

Many investors tend to overlook foreign funds, and I understand why: US stocks have been the superior performer for years on average. But in doing so, we miss some overseas moonshots:

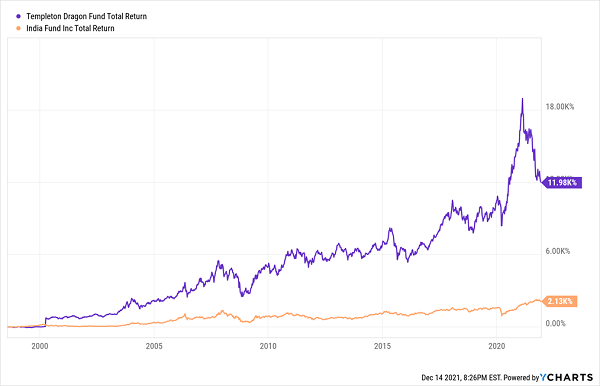

Imagine Quadrupling the S&P 500 in India…

…Or More Than Quintupling It in China!

Templeton Dragon (TDF) and The India Fund (IFN), which invest in Chinese and Indian equities, respectively, sport outsized yields of 36.5% and 11.5% at the moment. And while that’s historically lofty for both of them, high-single-digit and low-double-digit yields are very much the norm.

All the credit here goes to the funds’ managers, who have proved for years that for certain classes of investments, it pays to pay specialists rather than getting cheap and settling for income funds.

Your 2022 Guide to Retirement Riches: 7%-Yielding Blue Chips That Pay EVERY MONTH

And you and I can do even better yet. We can lock in 7% yields—paid monthly by blue-chip stocks and bonds—with little risk.

These types of investments are ideal for retirement funds. They hold up great during volatile markets, like the one we’re about to embark upon in 2022.

But with my favorite high-yield CEFs, you won’t have to wait nine months, or even every three months, for your dividends

You’ll receive a big, fat income check in the mail each and every month.

Listen. You can’t retire comfortably if you’re hunched in front of your computer every day, frantically monitoring the market and praying that a big price drop doesn’t crack your nest egg wide open.

You need to know, rain or shine, that a sizable dividend check is hitting your mailbox each and every month. No exceptions.

You need the “A” squad: diversified, reliable payers of high, sustainable income that don’t knuckle under every time the economy throws a fit.

And you can find these rare monthly dividend blue chips in my “7% Monthly Payer Portfolio.”

Many of the picks in my “7% Monthly Payer Portfolio” leverage the power of steady-Eddie holdings to generate not just massive yields, but shockingly aggressive price performance. The upshot is that we can do the unthinkable from an income strategy:

We can double our money much more quickly than traditional blue-chips-and-mutual-funds portfolios.

And the dividends?

They’re not just good. They’re not just great. This is life-changing income.

Do the math: Even if you have just a $500,000 nest egg—that’s less than half of what most financial gurus suggest you need to retire—into this powerful portfolio now, you can kick-start a $35,000 annual income stream.

That’s nearly $3,000 a month in regular income checks!

Even better? The market’s recent antics have provided us with a rare gift, pulling all of these monthly dividend stocks back into our “buy zone,” where we can grab them at bargain prices. Click here to get everything you need—names, tickers, complete dividend histories and more on these monthly dividend payers—right now!

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Enter your email address and we'll send you MarketBeat's list of seven best retirement stocks and why they should be in your portfolio.

Get This Free Report