There’s a crop of outsized dividends out there that are absurdly underpriced—I’m talking 14%-off discounts here. And our opportunity to pounce has arrived.

I’m talking about municipal bonds, which, like corporate bonds, look set to bounce as the economy slows and interest rates top out—then start to move lower. As rates ease off, bond yields will dip, putting a lift under bond prices (as yields and prices move in opposite directions).

The upshot? AI-powered NASDAQ stocks will lose their luster, and bonds and bond proxies—including utilities and “munis”—will likely be the darlings of 2024.

Heck, even a modest decline in rates would be enough to boost these assets. Which is why we’re loading up on them now. (I gave you some utilities with growing dividends to target in last Tuesday’s article.)

I know, I know. Municipal bonds, issued by state and local governments to finance infrastructure projects, don’t exactly get most folks’ hearts racing. But that’s not their job. Instead, these “recession-resistant” plays should be a cornerstone of your portfolio due to their stability.

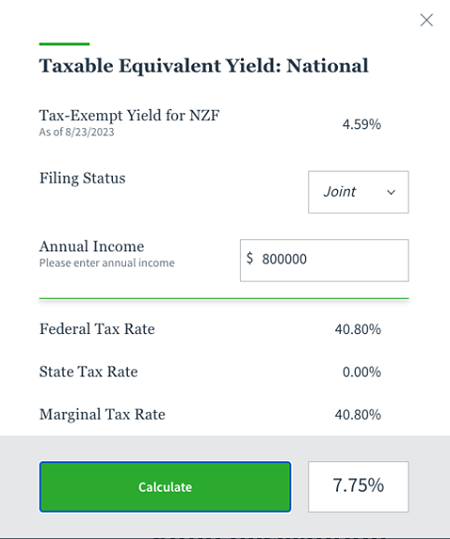

The biggest draw here is that munis don’t attract Uncle Sam’s attention: most Americans pay zero taxes on their muni dividends. This is no small detail: the 4.6% yield on the Nuveen Municipal Credit Income Fund (NZF), for example, amounts to a whopping 7.75% for a top-bracket filer filing jointly:

Source: Nuveen.com

Plus we get to buy cheap when we pick up our munis through closed-end funds (CEFs). Which we always do, for a bunch of reasons, starting with the fact that the small and insular world of munis is tough for us to access on our own, so doing so through a fund is the best option here.

Moreover, CEFs pay much bigger dividends than muni-bond ETFs. The go-to muni-bond index fund, the iShares National Muni Bond ETF (MUB), for example, yields just 2.5% today.

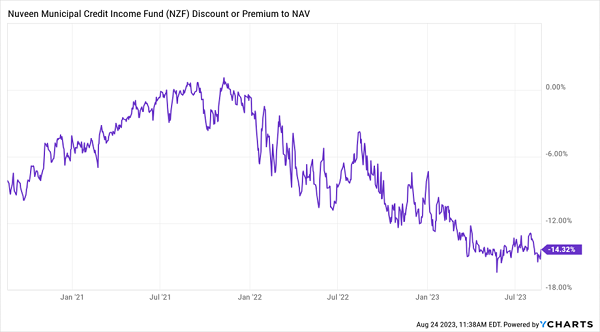

Finally, investors have been slow to pick up on the coming “rates-down-bonds-up trend,” leaving us some terrific deals on muni CEFs. NZF, for example, trades at a 14.3% discount to net asset value (NAV, or the value of the muni bonds in its portfolio) today. That’s far below its 6.6% discount over the last five years.

NZF Drops to the Bottom of the Bargain Bin

In other words, just a move back to that 6.6% average discount would imply a 9% price gain. And that’s before we account for potential gains from the coming “rate rollover.” That, of course, is also in addition to NZF dividend—7.75% on a taxable-equivalent basis for our top-bracket ballers.

ETFs? They never go on sale, so you’re stuck relying only on portfolio gains for upside.

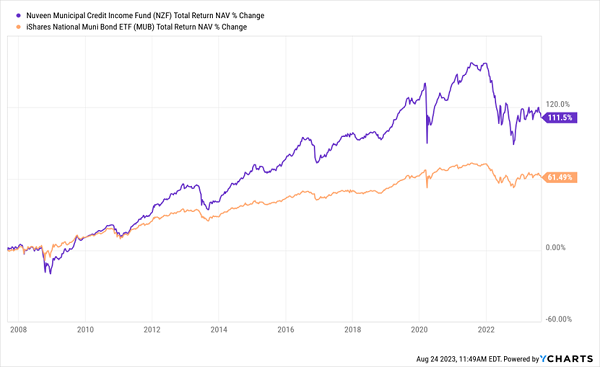

In terms of performance, NZF has a 22-year history behind it, having been launched in 2001. Moreover, its NAV return (or the return of its underlying portfolio) has easily beaten MUB since the latter was launched in ’07:

NZF’s Managers Crush the Benchmark

Truth is, we expect benchmark-beating returns from a muni CEF because the muni-bond market is tiny compared to the stock market, and the best of these funds have managers with deep connections, which is key to getting the best new issues. That’s an edge a “robotic” ETF like MUB simply can’t match.

Finally, NZF’s payout looks safe: its bond portfolio boasts an average coupon of 4.1%, just a hair below its 4.2% yield on market price. It gets better: because of the fund’s discount, its yield on NAV (or the yield on its underlying portfolio, in other words), is just 3.9%. That’s key because it’s the yield on NAV, not on the discounted market price, that management needs to earn to fund our 4.2% (before tax advantages) payout.

The bottom line here is that if you’re looking to bulk up your muni-bond holdings, NZF is a solid pick. And as I mentioned a second ago, its 14.3% discount won’t last: it’s just too low compared to the historical average.

Yours Now: A Full Portfolio of 8% Monthly Payers Set to Bounce

Something else we love about NZF is that it pays dividends monthly. And it’s far from the only monthly payer out there that’s set to gather steam as rates peak and roll over.

I’ve got a full portfolio of monthly paying REITs, CEFs and regular stocks that have serious upside as the market recovers from the banking mess. I’ve put them all in my “8% Monthly Payer Portfolio”—and I want to share everything I have on these income plays with you now.

Click here and I’ll tell you all about these stout monthly payers and show you how to download a FREE Special Report that gives you their names, tickers, current yields and a full analysis of each one.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Discover the top 7 AI stocks to invest in right now. This exclusive report highlights the companies leading the AI revolution and shaping the future of technology in 2025.

Get This Free Report