Select bank stocks may be cheap, but why settle for 2% to 3% yields?

Let’s really bang on the bargain bin and for dividends between 8.3% and 9.4%. These yields are available thanks to the current banking fears.

Fortunately, these payouts are more secure than vanilla investors appreciate. Hence, the dividend deal.

A Better Way to Play Banks

I wrote a few weeks ago about how mainstream investors are trying to time a bottom in banks.

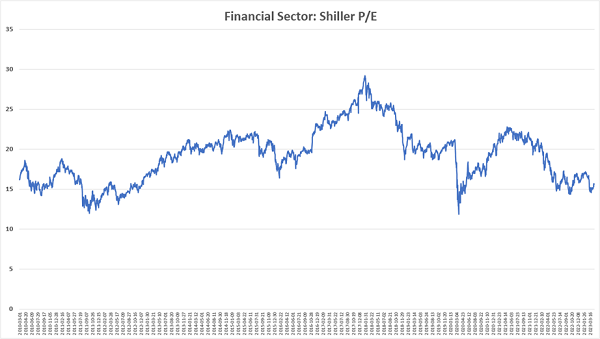

Fair enough. Banks are extremely cheap right now by a well-known measure of long-term value: CAPE (cyclically adjusted price-to-earnings), which is the price divided not by the past year of earnings, but the past 10 years. This metric was thought up by Yale University professor Robert Shiller—thus is also known as the Shiller P/E—to value companies in a way to smooth out short-term earnings volatility.

This Is One of the Best Financial-Sector Deals in a Decade

Source: GuruFocus, Contrarian Outlook

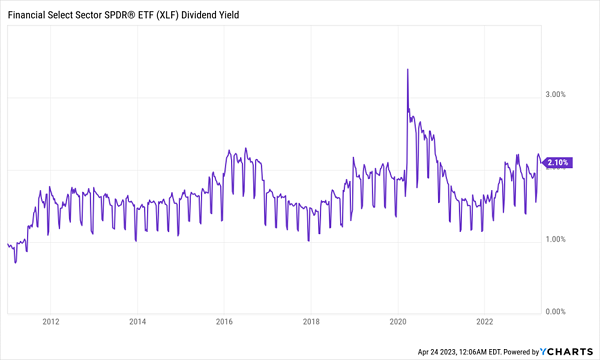

But even at bargain prices, the financial sector isn’t delivering on the income front.

Financials’ Yields Are Flat, Not Fat

But we can get much, much more income out of the exact same companies by shifting our strategy—instead of dumpster diving in banks’ common stocks, which are the stocks you and I are used to, we want to focus on preferred stocks.

As I said earlier:

“We’re doing it through preferred shares, which are part stock, part bond and all dividends. And because banks issue most preferreds, they’re the contrarian’s choice for profiting from this mess.”

Preferred stocks represent ownership in companies, but they trade with more stability like bonds, and they feature high, fixed dividends. They’re also paid out before common-stock dividends, giving them a higher level of safety. And while you can find preferred stocks across a number of industries, the lion’s share can be found in the financial sector.

Thing is, while you’ll find plenty of analysis and research on the common stocks of companies like JPMorgan Chase (JPM) and Citigroup (C), there’s very little you can dig into about their preferreds. So investors are typically better off buying them in batches through funds.

The so-called “smart money,” and most retail investor cash, is stashed away in preferred exchange-traded funds (ETFs). That’s a so-so way to invest in the space—but you’re leaving some returns and yield on the table that way. Instead, I suggest you take a look at closed-end funds (CEFs), which let us buy preferreds collectively at greater discounts than if we had bought them individually, collect a few more percentage points’ worth of yield, and leverage skilled managers who can make the most of bargains in the preferred-stock space.

Just consider these three preferred-stock CEFs that yield between 8.3% and 9.4% right now:

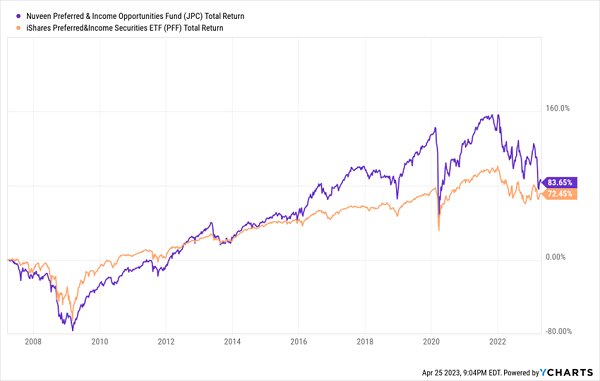

Nuveen Preferred & Income Opportunities (JPC)

Distribution Rate: 8.3%

Let’s start out with the Nuveen Preferred & Income Opportunities (JPC), which delivers an 8%-plus yield through a basket of fairly high-quality preferreds.

Nearly two-thirds of JPC’s 230-stock portfolio are investment-grade, including single-digit exposure to A-rated preferreds. BBs are another 27%, leaving just a peppering of B-rated and unrated issues. And true to preferred funds’ preference for banks, financial preferreds represent more than three-quarters of assets.

Something else that stands out with JPC is the presence of international preferred stocks—and in fact, with ex-U.S. preferreds making up 35% of the fund, you could call JPC a truly “global” CEF. Its international positions include stocks from the U.K., France, Italy, and more, with overseas mega-banks HSBC (HSBC), Lloyds Banking Group (LYG) and Barclays (BCS) in the top 10 holdings.

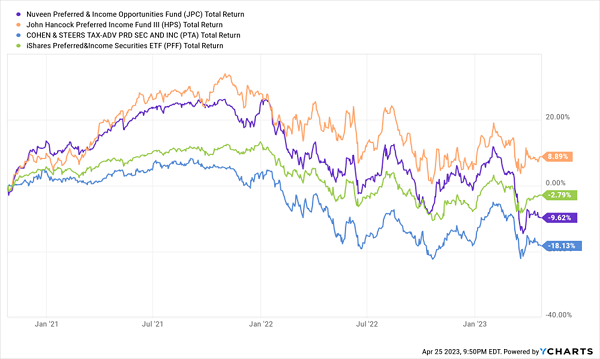

This Nuveen CEF has been a longtime outperformer since inception in 2003, though its lead over plain-vanilla preferred ETFs has dwindled over the past year-plus. The primary culprit: rocketing interest rates, which have not only weighed on preferred prices, but have inflated the expenses of its whopping 37% in debt leverage.

JPC’s Longtime Lead Has Been Whittled Away

JPC is nonetheless a good fund at a good price—it trades at a nearly 12% discount to net asset value (NAV), which is much deeper than its five-year average discount of 4%. Should Fed Chair Powell take his foot off the gas, this preferred fund could start to look much more attractive.

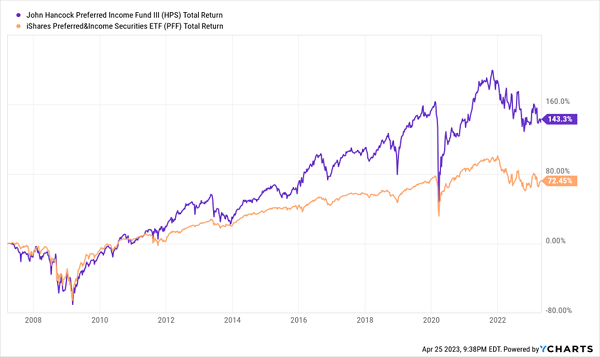

John Hancock Preferred Income Fund III (HPS)

Distribution Rate: 9.2%

That’s no typo—the John Hancock Preferred Income Fund III (HPS) is the third of three John Hancock preferred-stock CEFs. While not cleverly named, it is the largest of the three, at $455 million in assets, though it’s also the youngest, coming live in 2003 versus 2022 for its pair of brothers.

This CEF’s goal is pretty straightforward: generate high income from a basket of preferred stocks while investing at least half of the portfolio in investment-grade issues. It’s slightly more than that now—57% of assets are in BBB-rated preferreds, with another 34% in BBs, and the rest B and below (or unrated). Not as high-quality as JPC, but not by much.

Like JPC, John Hancock’s preferred CEF is loaded up with leverage, at 39%, so volatility is much higher than you’ll get from a basic preferred index fund. But where HPS differs is a much lower concentration of financials—about 56%, which isn’t nothing, but is much lower than you’ll find in most preferred funds, CEF or ETF. That has served it well of late—in large part because recent bank-implosion scares haven’t hit HPS’s portfolio as hard—helping the CEF to pad its long-term outperformance.

HPS: A Bumpy Ride, But Still a Better Ride, Too

That said, a little pause might be warranted. John Hancock’s preferred funds rarely trade at a discount, HPS included. But currently, HPS is trading at a 6% premium to NAV, which compared to a 2% long-term average premium, is expensive even by its own standards.

Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund (PTA)

Distribution Rate: 9.4%

The biggest yield of the bunch can be found in a younger fund: the Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund (PTA), a COVID-era launch from October 2020.

Sadly, this fresher face hasn’t held its own against its older peers.

PTA Pulls Up the Rear

The question now becomes, “Is PTA a beaten-up value?”

The name “Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund” is easy to misinterpret. Typically, if you see “tax-advantaged” in a fund name, you think municipal bonds. But that’s not the meaning here. Instead, PTA is trying to “achieve favorable after-tax returns for its shareholders by seeking to minimize the U.S. federal income tax consequences on income generated by the Fund.”

It does that in two ways:

- Invest in preferreds that pay qualified dividends. It sounds like a chore, but it’s not. Many preferreds already pay qualified dividends.

- Achieve favorable tax treatment by holding longer. In short, PTA is taking advantage of favorable long-term capital gains rates.

This isn’t some wonder-formula—the result is a pretty run-of-the-mill preferred CEF portfolio. PTA holds roughly 250 preferreds, more than 70% of which are from the financial sector. It’s highly global in nature, with almost 40% of its issues coming from overseas. A little less than half the portfolio is investment-grade in nature. And it’s using almost 40% debt leverage right now.

With less than three years of trading under its belt, management doesn’t have much of a track record to analyze yet. But at least so far, it doesn’t appear the “tax-advantaged” special sauce lends much to performance, nor does it really differentiate the breakdown of its distributions.

If there’s anything to like, it’s a high 9% yield and a steep 10% discount to NAV—though the latter’s not markedly different than its typical pricing since coming to market.

Give Me 4 Minutes, I’ll 4X Your Retirement Income

While these preferred funds are certainly a better alternative than traditional bank stocks, I don’t love them. Any sort of let-up from Powell is always just around the corner, but never here, and as long as he’s taking the fight to inflation, these preferred funds sit on shaky ground.

That’s not exactly the sturdy ground we need to build our retirement portfolios on.

If we want a cozy, comfortable retirement without bleeding your nest egg dry, we need to be able to plan around our income with laser precision. Fortunately, there are plenty of safe harbors in our “Perfect Income” portfolio—and you can enjoy their security and sky-high dividends, too.

- The perfect dividend retirement stocks have several things in common:

- They pay you consistently, predictably and reliably.

- They’re built to survive—even thrive—in market crashes.

- They deliver double-digit returns, with safe, secure investments.

- They take just a few minutes every month to “manage.”

- They DON’T involve day trading, buying on margin or any other risky strategy.

- They DON’T involve gambling on penny stocks, Bitcoin or buying puts and calls.

Getting each and every one of these things from any single holding might sound impossible. But it’s par for the course for every position in my “Perfect Income” portfolio.

Let me show you the stocks and funds you need to stabilize your retirement. But more importantly, let me teach you more about this incredible strategy itself and make you a better investor in the process!

Take control of your financial legacy today. Click here for my newly updated briefing on the Perfect Income Portfolio!

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Nuclear energy stocks are roaring. It's the hottest energy sector of the year. Cameco Corp, Paladin Energy, and BWX Technologies were all up more than 40% in 2024. The biggest market moves could still be ahead of us, and there are seven nuclear energy stocks that could rise much higher in the next several months. To unlock these tickers, enter your email address below.

Get This Free Report