It’s as predictable as night following day: Stock markets crash, and we almost immediately hear more about the so-called “60/40 rule” as a way for investors to protect themselves.

Don’t fall for this overdone “rule of thumb” (which, as the name says, recommends putting 60% of your portfolio into stocks and 40% into bonds).

Today we’re going to look at a much better way—one that pays you 9.7% dividends and delivers far better performance, too.

2025 Is 2022 Redux for the 60/40 Crowd

Today’s setup reminds me of what I heard near the end of 2022, when stocks were crashing. Back then, many advisors were dredging up this old idea to help ease worried investors’ fears.

Except, in doing so, they were costing those investors money, which I pointed out in an October 2022 Contrarian Outlook article: “With the 60/40 portfolio, you’re actively withdrawing money from your portfolio during a bear market, so the longer the market stays down, the more you need to gain to make your initial investment whole again.”

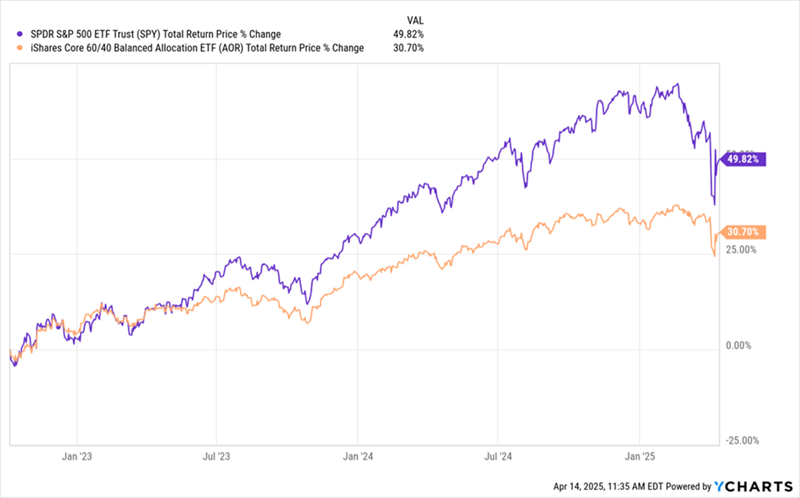

Here’s how a garden variety S&P 500 index fund has done compared to a 60/40 ETF, the iShares Core 60/40 Balanced Allocation ETF (AOR), since then:

Stocks Clobber 60/40

In other words, even with the tariff panic (which you can see at right above), investors who opted for 60/40 rule then are $1,912 poorer, as of this writing, for every $10,000 they invested than those who simply bought an S&P 500 index fund.

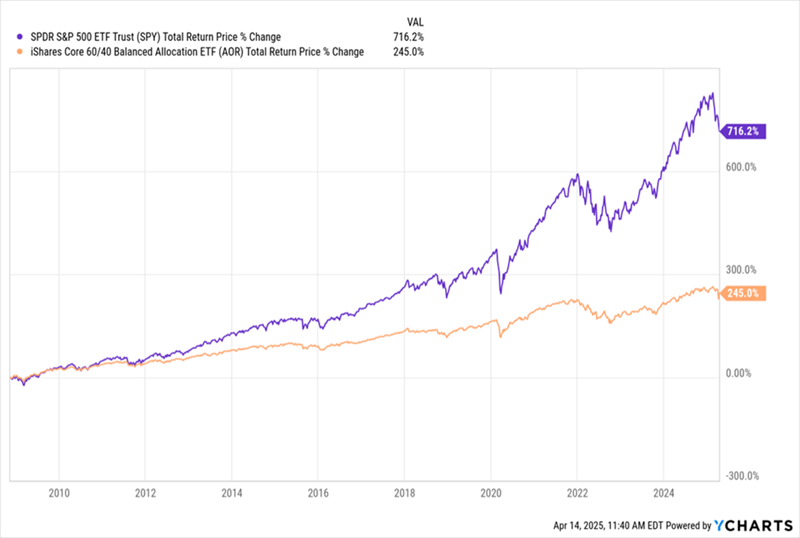

Now that investors are panicking again, I’m even more convinced 60/40 is a poor strategy. Let’s zoom out and look at the lousy performance this rule has baked in over the long run:

60/40 Rule Costs Investors a Fortune

Here we see that investors relying on 60/40 would’ve missed a staggering $47,120 in profits for every $10,000 invested over 16 years.

Stretch that over a lifetime, and you can see that 60/40 can literally cost you millions.

To be sure, moving cash into bonds might feel good today, with fear running high, but if you do, you will lose money compared to the average stock investor.

Where 60/40 Came From

The 60/40 rule stems from economist Harry Markowitz’s modern portfolio theory (MPT) from back in the 1950s. This work suggested investors could optimize returns, relative to risk, by diversifying across asset classes.

By the late 20th century, 60/40 was a go-to for many investors, although, as you can see from the chart above, it began badly lagging stocks in the early 21st century (it had actually begun doing this in the 1990s, but things really fell apart after the dot-com bubble burst).

Markowitz never meant this rule to be an actual guide for advisors, but it is convenient, so it’s not too surprising that it’s endured—even with its poor performance.

Investment Pros Start to Turn on 60/40

But that may be starting to change, as more pros speak out against 60/40. That may, funnily enough, speed up a stock rebound.

Just before the Trump tariff selloff began, Blackrock’s Larry Fink wrote about how the rule doesn’t work anymore, saying it “may no longer fully represent true diversification.” More recently, Apollo Chief Economist Torsten Sløk wrote that the 60/40 portfolio continues to underperform, “with only a 2% annual return for the past three and a half years.”

The question, then, becomes: What do we choose instead?

CEFs: Your High-Income Alternative

In that October 2022 article I mentioned earlier, I suggested an alternative to 60/40: three closed-end funds (CEFs) that combine stocks, corporate bonds and real estate.

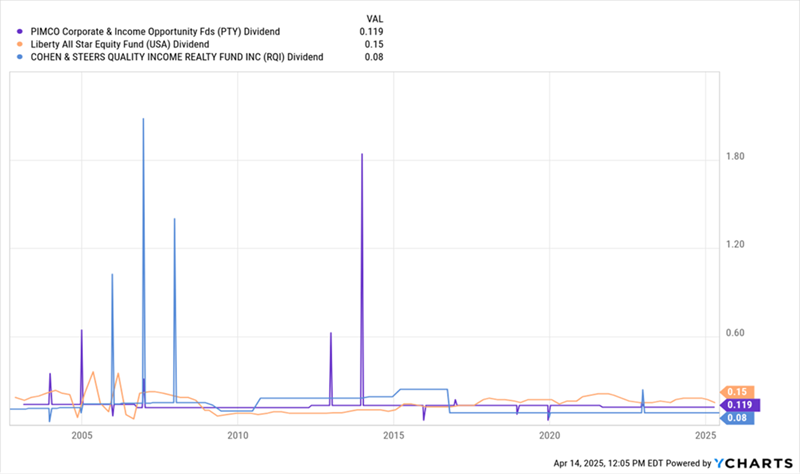

This three-fund “mini-portfolio” included the 9.5%-yielding, stock-focused Liberty All-Star Equity Fund (USA); the 11.2%-yielding, bond-focused PIMCO Corporate & Income Opportunity Fund (PTY); and the real-estate-heavy, 8.5%-yielding Cohen & Steers Quality Income Realty Fund (RQI).

Why these funds? The reason is why members of my CEF Insider service choose CEFs in the first place: income. With an average 9.7% yield as I write this, they provide a huge income stream that index funds and 60/40 simply can’t match.

We have also seen, in the more than two decades since all three of these funds have been around, very consistent payouts, on average.

Reliable Payouts, Special Dividends Keep Retirements Funded

Because profits from stocks fluctuate (every year will give different returns), USA’s dividend will tend to move around more than the more stable payouts PTY provides. Meantime, changes in income from rents, as well as fluctuating interest rates, tend to cause RQI’s payouts to take a small step up or down for a few years’ time.

Over the long haul, though, these payouts tend to remain roughly stable as managers move to keep them consistent.

Beyond this, though, is the performance.

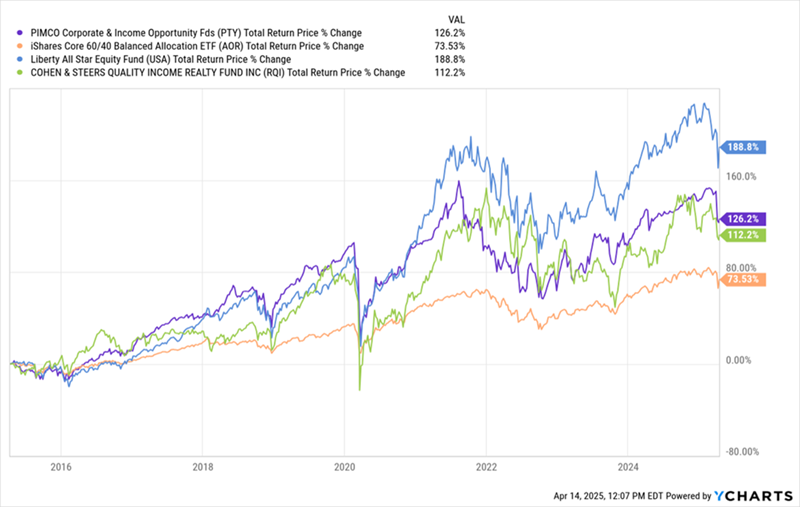

Strong Long-Term Profits

Over the last decade, these funds have delivered a 9.3% average annualized return, while 60/40 (shown in orange above) has delivered about half that.

The bottom line: These three funds have a proven history of delivering strong dividends, and they spread your money across asset classes. In other words, they do what 60/40 is supposed to—without the (potentially millions) in missed profits.

A 9.7% Dividend Is Nice—But Here’s an Even Better Way to Crush 60/40

There’s no doubt about it: Go with the 60/40 rule and you WILL be stuck with weak returns—and a puny income stream, too.

It’s locked in.

Meanwhile, those who buy a handful of overlooked closed-end funds (CEFs), like the ones we just discussed, will be quietly collecting HUGE dividends while positioning themselves for big gains.

To give you the biggest edge over the 60/40 crowd—and do even better than the three CEFs I’ve pointed out above—I’ve zeroed in on 5 CEFs I urge all investors to buy now.

These 3 “battleship” funds pay 8.3% dividends between them and are massive bargains today. That’s key, because their cheap valuations help cushion them in a downturn—and set them up for market-beating gains when stocks turn higher.

And we’ll collect their 8.3% dividends the entire time!

The longer you wait to buy these 5 funds, the longer you’ll have to wait for your first dividend payout. Don’t leave cash on the table: Click here and I’ll tell you more about these five “60/40-crushing” funds AND give you a free Special Report revealing their names and tickers.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Unlock your free copy of MarketBeat's comprehensive guide to pot stock investing and discover which cannabis companies are poised for growth. Plus, you'll get exclusive access to our daily newsletter with expert stock recommendations from Wall Street's top analysts.

Get This Free Report