As we head towards the most telegraphed recession in recent memory, US Treasuries are receiving a lot of attention. And rightfully so.

In recessions, interest rates go down. This boosts bond prices (which trade opposite rates).

But not all bonds are created equal—especially during recessions. Slowdowns tend to make the safest bonds the most attractive.

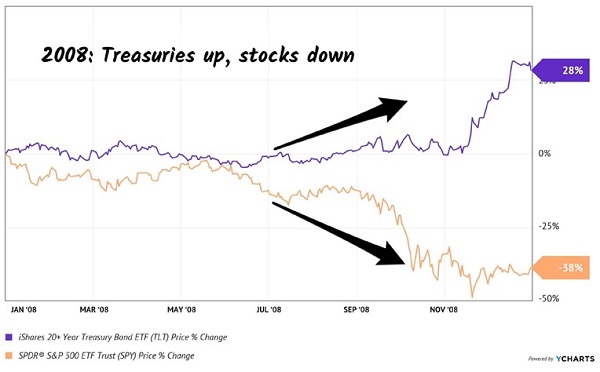

After all, it can be a slippery slope from slowdown to meltdown, so many investors prefer the safety of Treasuries. In 2008, for example, the S&P 500 sank 38% but US Treasuries rallied sharply. The iShares 20+ Year Treasury Bond ETF (TLT) delivered a 28% gain for the year:

In 2008, T-Bonds Did Great

I don’t think we’re in for a repeat of ’08, but this “buy Treasuries before a recession” trade has worked superbly since we called it in November. TLT is up 16% since then!

Major media outlets soon followed our contrarian call, so today the Treasury trade is a bit too popular for my liking. We should instead focus on almost-as-safe bonds trading for just 86 cents on the dollar.

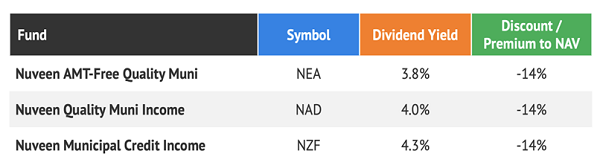

Municipal (“muni”) bonds remain in the bargain bin. While they too have gained in value since November, they are cheaper now than they were then.

We can see this reflected in discount windows that are wide open with respect to their net asset values (NAVs). Check out these three fine funds from Nuveen:

Nuveen is our “go to” bond manager when it comes to munis. They get the first phone call and, hence, the best deals.

I’m talking financing for behemoths like Chicago’s Board of Education and New York’s Liberty Development Corp. These state-financed agencies are safe bets because if they ever can’t pay, they will be bailed out by the Fed so they can.

Yup, the Federal Reserve will ride to the rescue. Chairman Jay Powell & Co. are already staring at a potential banking crisis. They won’t risk an unraveling in the muni market.

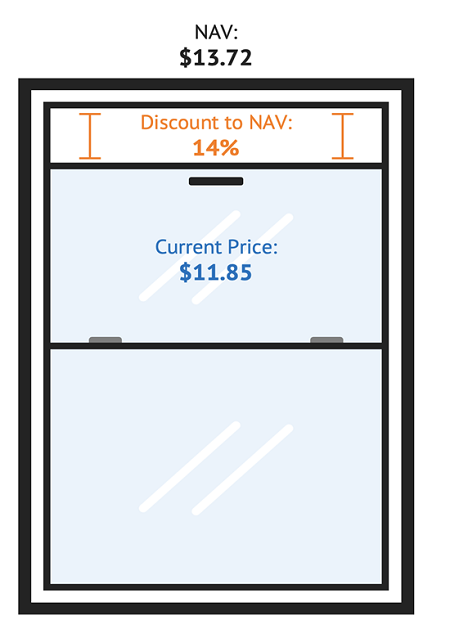

Which is why a fund like Nuveen Municipal Credit Income (NZF) is really a fantastic deal. It trades at a 14% markdown to its NAV. This discount window is as wide open as we ever see!

NZF’s Discount Window is Wide Open

Munis like NZF have been pinched on both ends by rising rates. First, as long rates rose, the value of NZF’s underlying holdings declined (interest rates up, bond prices down). This was reflected in the fund’s declining NAV.

Second, the earnings power of NZF dropped when its cost of money increased. NZF (like other muni CEFs) uses leverage to juice returns. This is a “no brainer” when short rates are low, but they skyrocketed at the start of 2022.

The result? NZF had less cash and trimmed its dividend.

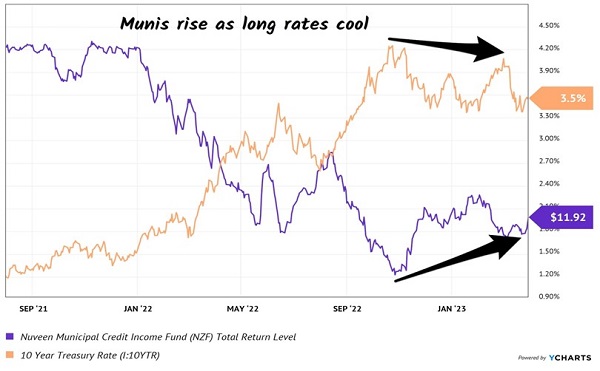

But the payout pain appears to be over. Munis are rising and with a recession on the way, a top is likely in for long rates. These bonds sold off on “duration risk”—the price pain inflicted by higher rates. With duration turning around, this will be a net positive for munis:

Finally, “Duration” Risk Helps Munis

NZF presents a compelling “total return” formula here. Its dividend will stabilize, and we have a 4.3% starting yield. Plus the fund is selling at a 14% discount to NAV, which means we can buy it for just 86 cents on the dollar.

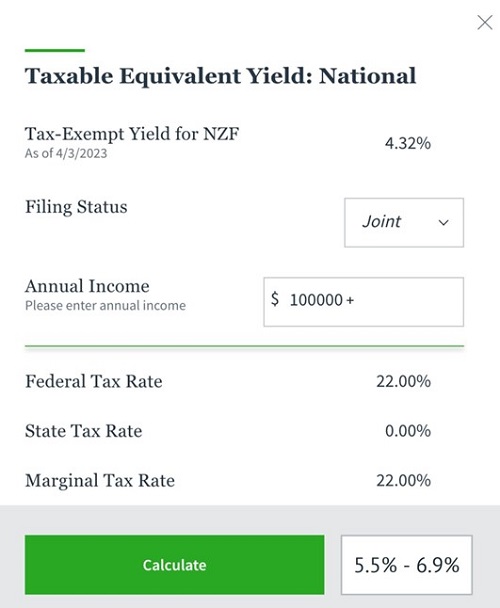

Also, NZF saves us on our tax bill. For my $100,000+ income folks, we’re looking at taxable equivalent yields between 5.5% and 6.9%!

(Source: Nuveen’s Taxable Equivalent Yield calculator.)

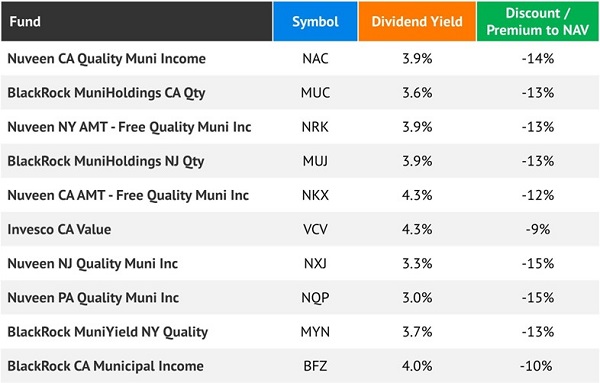

Looking for a break on state taxes, too? I get it—I’ve lived most of my life in New York and California.

Consider a state-specific muni fund. There are many. Here are the ten largest, all offering delicious discounts:

Buying muni bonds at 14% discounts is a “no brainer” retirement move. If you’re looking to retire on dividends, it’s tough to beat these types of tax-advantaged plays.

But why don’t we hear this from the tried-and-true money advice crew?

Because the idea of an 8% “No Withdrawal” Retirement Portfolio is too beautifully logical. Retire on dividends and, really, there’s nothing left to talk about!

The trick, of course, is finding yields that are high enough to make it work. If we’re trying to stretch $500K or a million dollars forever, then we really need 8%+ yields.

These muni funds, of course, aren’t quite there. But I have plenty of stealth payout plays that do yield the 8% or more that we need to coast forever on dividends alone. Please click here and I’ll share the details on these secure funds with very generous dividends.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Looking to profit from the electric vehicle mega-trend? Enter your email address and we'll send you our list of which EV stocks show the most long-term potential.

Get This Free Report