We’ve been extolling cash in these pages since the start of this year. As the Federal Reserve prepared to pause its money printer, we contrarians booked profits and stacked dollar bills.

Long before the media began saying “bear market,” we recognized that a volatile 2022 was highly likely. We were ready for a decline.

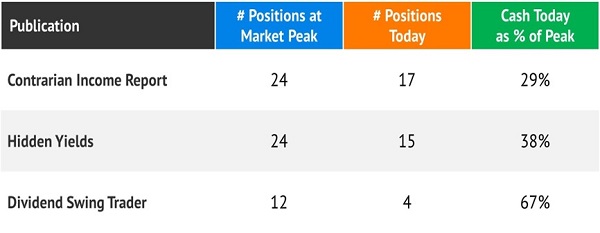

As I write, our premium portfolios are all sitting on sizeable cash positions:

Yup. Plenty of capital ready to be deployed after the final “wash out” in the markets.

These comfortable cash seats have served us well. Bonds kicked off their worst start to a year since 1788 (per Nasdaq). Fixed income, often a safe haven, was anything but. Even US Treasuries, which sailed in 2008, have been trampled in 2022.

The Nasdaq itself has never started a calendar year worse since, well, ever. And the S&P 500—the only investment most Americans own—clocked its worst start since 1939.

Which made cash the perfect place to be, right?

There’s just one problem, though. Cash is just… so… boring.

I get it. We are income investors. We want to be fully invested in something while we wait the bear out.

As thoughtful subscriber William writes:

Q: Why not use short-term bond funds or floating-rate funds as “cash equivalents?” We would at least get a small amount of interest while we are waiting.

William, I’m always up for interest, no matter how modest! But we need to find it securely and safely. Right now, that ain’t happening. And a few bucks in interest aren’t worth watching the principal get clobbered.

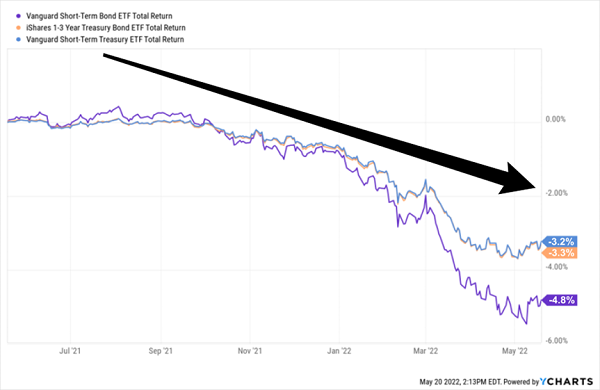

Let’s start with your short-term bond suggestion. A reasonable idea. The world has been “selling duration” with rates rising. Why not avoid long-term fixed income (and its duration) and park our cash in short-term bonds instead?

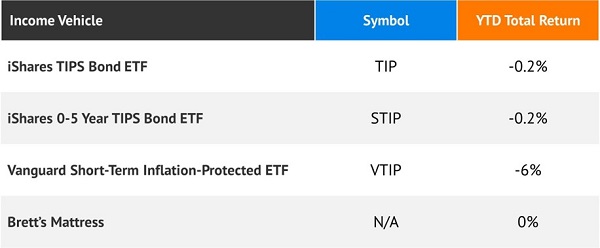

Because, unfortunately, the short stuff is getting smacked too. Here are three of the most popular short-term bond ETFs in the world. All have lost money in the past year:

3 Poor Cash Equivalents

What about floaters? They have variable coupons—interest payments—that are calculated regularly. Their rates start with a reference point, such as the federal funds rate and add a defined payout percentage to it. When the reference ticks higher, so does the coupon’s payout.

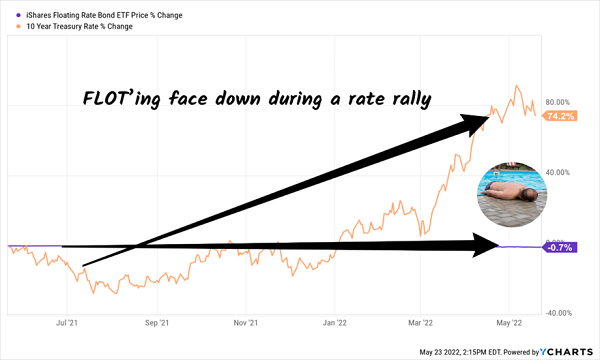

The iShares Floating Rate Bond ETF (FLOT) is the ETF lovers’ alternative to TLT. FLOT buys corporate bonds with floating rate features.

These bonds aren’t as bulletproof as Treasuries, but they are close, because FLOT only buys investment grade paper.

FLOT is doing better than the fixed rate bonds above. Unfortunately, FLOT lags the cash stuffed under my mattress year-to-date:

FLOT yields a puny 0.6%. Drop a million dollars into this fund, and we reap just $6,000 in yearly income. Pretty lame for a seven-figure account.

Sure, the FLOT fanboys will point to price upside. But if FLOT’s price can’t float higher under these conditions, when will it rally?

Now, floating-rate closed-end funds (CEFs) usually beat their comatose ETF counterparts. CEFs benefit from active management. When we let the ETF computers do the fixed income picking, they lose to my mattress.

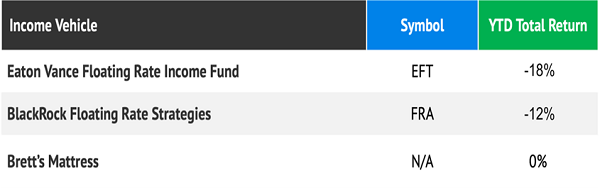

My “go to” floating-rate CEFs are Eaton Vance’s Floating Rate Income Fund (EFT) and BlackRock’s Floating Rate Strategies (FRA). Contrarian Income Report subscribers and I have had flings with each during a previous rising rate period.

The yields on EFT and FRA look good today at 7% and 6.2%, respectively. Both funds trade at discounts to their net asset values.

Should we park our cash there?

I wish income investing were that easy. Problem is, EFT and FRA prices aren’t floating either. EFT is down 18% year-to-date, while FRA has shed 12%. Investors who buy these funds for inflation insurance have been disappointed.

Maybe TIPS? Treasury Inflation Protected Securities are indexed to inflation. Their value, theoretically at least, is supposed to rise as inflation climbs because their interest rate payments adjust higher.

And these are Treasuries, so they’re even safer than FLOT and EFT and FRA.

Except… these three popular TIPS are losing to my mattress, too:

How about the new Series I savings bonds? They boast a sweet headline yield of 9.62%. But if we’re holding cash now so that we can bargain hunt soon, I-bonds have two big drawbacks:

- We must hold them for one year.

- We can only invest $15,000 per year.

(The annual limit is $10,000 per person, plus an extra $5,000 per year if using a federal tax refund. These position size and liquidity restrictions prevent I-bonds from being a big play for us.)

We need to be nimble and ready to buy. The best deals happen at the end of bear markets.

Let’s not outthink ourselves with our cash equivalents. Sure, it’s boring, I get it—but cash really does mean cash. Our post-bear profits depend on this preparation.

And hey, since we’re friends, I’ll save some space under my outperforming mattress for your stack, if you’d like.

As I write, the stellar 17 stocks in my Contrarian Income Report portfolio yield an average 7.6%. This baker’s dozen is spinning off $76,000 for every million dollars invested.

Not a bad cash companion!

And you don’t have to be a millionaire to take advantage of this strategy. A $500K nest egg will create $38,000 in annual income. Or $200K will generate $15,200 in yearly dividend income. And that’s hard to find.

The important thing is that these yields are safe, which creates stability for the stock (and fund) prices attached to them. We want our income, with our principal intact. It’s really the only way to retire comfortably, without having to stare at stock tickers all day, every day. Sound good?

Best of all, many of my favorite dividends are paid monthly. So, we’re talking about $3,000+ in dividends every month on that $500K. Or $6,000+ per month in income on the seven-figure accounts that Fidelity brags about in its ads.

Click here and I’ll share my favorite 7%+ dividends that are being paid monthly—plus how to get my specific stock and fund names, tickers, and recommended buy prices.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Wondering where to start (or end) with AI stocks? These 10 simple stocks can help investors build long-term wealth as artificial intelligence continues to grow into the future.

Get This Free Report