It’s finally happening: Management fees on our favorite 8%+ paying assets—closed-end funds (CEFs)—are falling. And some are sending their already soaring dividends even higher, too.

Those are key reasons to invest in these high-yield plays now. We’ll get into all the details below. But before we do, it’s important that we take a second to put CEF fees in perspective. That’s because many (most?) investors have a totally incorrect idea about them. And it’s caused them to miss out on the income (and growth) CEFs offer.

Ignore the Wall Street Line: CEF Fees Are Sometimes Worth Paying

When I ask investors if they’ve ever considered CEFs, those who say no often mention high fees as a reason. It’s clear that many folks simply look at CEF management fees, compare them to what they pay on bargain-basement ETFs—and set CEFs aside.

It makes sense on the surface. The investment industry has pounded the idea that any fees are bad into investors’ heads for decades now.

It’s too bad, really. Because those who get hung up on fees are missing out, as there are plenty of CEFs out there that clobber ETFs with fees included. That goes double when you look beyond stocks, to assets like corporate bonds, real estate investment trusts (REITs) and municipal bonds.

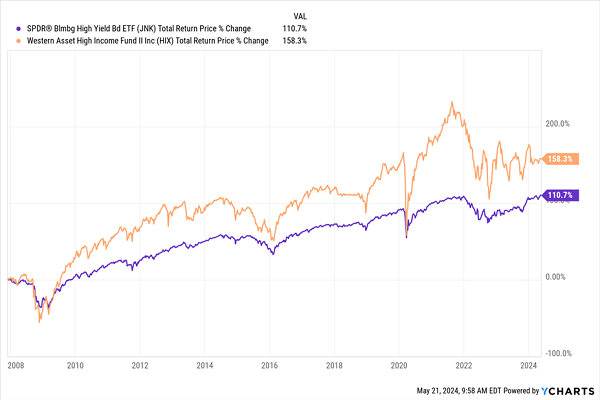

Consider a CEF called the Western Asset High Income Fund II (HIX), whose total return is well ahead of that of the bond benchmark SPDR Bloomberg High Yield Bond ETF (JNK) since JNK’s inception in 2007:

“Human-Run” HIX Outruns Its Benchmark

In the case of HIX, the fund charges 1.2% of assets per year on net asset value (NAV, or the value of the fund’s underlying portfolio), plus 0.2% in additional expenses and 1.86% in interest expenses on the fund’s leverage.

Compare that to JNK, with just 0.4% expenses. HIX also doubles up JNK’s dividend, 13.3% to 6.6%. The CEF pays dividends monthly, too.

Beyond HIX, there are plenty of other examples of CEFs topping their benchmarks. In the case of bond funds, this largely reflects the value of personal connections. In the bond world (which is a lot smaller than the stock world), these make a huge difference, as a well-connected manager can (legally!) get first crack at the best new issues.

As you can see above, that edge alone is worth paying for. Algorithm-run ETFs just can’t match it. The key to judging fund fees, then, is that while we never want to overpay, we are happy to pay the fee if the performance is there.

I think you’ll agree that in this case, the higher fees are worth it! But the best news is, we CEF investors are going to “have our cake and eat it too.” Because the biggest CEF manager of them all, BlackRock, is now cutting fees (and raising dividends). And where BlackRock—which boasts $10 trillion in assets under management, goes, others eventually follow.

BlackRock Starts the Fee-Slashing (and Dividend-Raising) Party

The investment firm is slashing fees on 24 municipal-bond CEFs—you can get the full list in BlackRock’s press release here. To be clear, admittedly, it’s not worth much yet, but this is the biggest effort to reduce CEF management fees in a very long time.

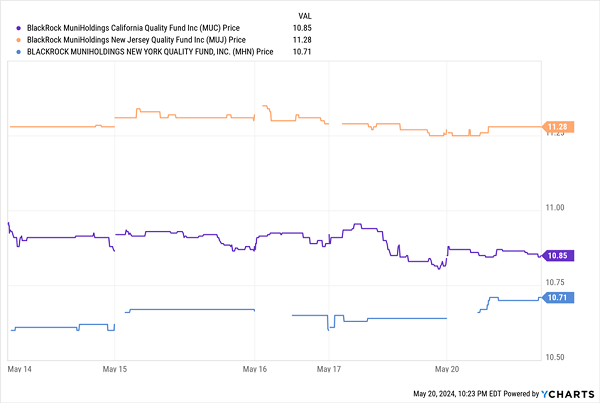

Just looking at the first three funds on BlackRock’s list, the BlackRock MuniHoldings California Quality Fund (MUC), BlackRock MuniHoldings New Jersey Quality Fund (MUJ) and the BlackRock MuniHoldings New York Quality Fund (MHN), we see how the funds saw no real movement in their prices after the announcement (which was released before trading on May 20).

BlackRock’s Fee Waiver Makes No Waves

At the same time, BlackRock raised payouts for a bunch of other funds, including two funds on its fee-reduction list: the BlackRock MuniYield Pennsylvania Quality Fund (MPA) and the BlackRock California Municipal Income Trust (BFZ). Those funds, it turns out, did see a small, temporary pop on May 20th.

What the Trend Toward Lower CEF Fees Really Means for Us

The takeaway here is clear:

- CEFs don’t generally pop when fees go down a little. That’s because veteran CEF investors know the real score on fees, as we saw with HIX above.

- CEFs are more likely to rise when payouts jump, but as investors mainly look to these funds for current income (the average CEF yields around 8% today), that pop isn’t usually as long-lived as it would be for, say, a typical S&P 500 stock (average yield: 1.3%).

That change in fees also makes sense when you consider the relationship between fees and CEFs’ discounts to net asset value (NAV, or the value of their underlying portfolios). In the case of HIX, the fund trades at a roughly 3% discount as I write this, covering the fund’s combined fees for management and interest. In other words, investors are essentially getting the fees—both management and interest—returned to them through the discount.

The bigger news on this isn’t the fee reductions themselves—it’s the fact that BlackRock is slashing fees and hiking payouts to respond to aggressive shareholder activism, which has increased. Now that it’s here and growing, more fund managers will have to slash fees, work at lowering discounts, and improve overall performance.

I can tell you that many CEF managers are unhappy about this. Their lives are getting harder as the pressure is ratcheted up. But that’s fine. Managing a CEF remains a terrific job for a portfolio manager. We don’t have to shed any tears for these folks! Nor do we have to worry that our CEF managers will quit en masse.

Instead, CEF managers are waking up to the new reality: They simply cannot allow discounts to linger forever. So if you buy a discounted CEF today, especially one that’s highly discounted relative to its historical trend, you might be surprised to find fund managers working harder to get rid of that discount than ever before.

5 Urgent CEF Buys (Average Yield: 8.6%) to Make as Activists Ramp Up

As we just discussed, with activists putting pressure on CEF firms to slash fees and boost payouts, now is a perfect time to get into these high-paying funds.

I’ve zeroed in on five that are terrific plays on this trend. They yield a rich 8.6% between them and trade at ridiculous discounts, too. I expect those discounts to dribble away in the next 12 months, as more CEF managers follow BlackRock’s lead.

My forecast? I’m calling for 20%+ price returns on these funds, in addition to their 8.6% average dividends.

Simply click here and I’ll tell you more about why CEFs are so far off the radar for most folks (hint: Wall Street wants you to ignore them!) and give you access to a free Special Report naming all 5 of these stout 8.6% payers.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Looking to generate income with your stock portfolio? Use these ten stocks to generate a safe and reliable source of investment income.

Get This Free Report