Real estate investment trusts (REITs) have become quite popular with income investors in recent years. And why not? These “retirement makers” are required to give 90% of their profits to their shareholders as dividends.

So, if you’re looking to retire on dividends, REITs are a natural place to look.

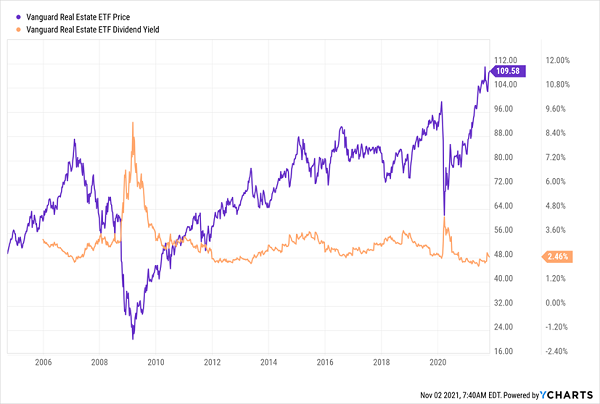

Problem is, their popularity comes at a price. The Vanguard Real Estate ETF (VNQ) yields just 2.5% today—pretty lame by its standards:

The Problem with Popularity: VNQ Pays Just 2.5%

A disappearing dividend isn’t the only problem with VNQ. Like most ETFs it tends to overweight the largest REITs, which typically translates into both lower overall yields and slower dividend growth. So, we’re left with a couple of options:

- We can “cherry pick” its holdings for hidden gems.

- Or we can buy REIT closed-end funds (CEFs) instead.

Option two is compelling today. Rather than buy an ETF at “par” or fair value, we can bank discounts up to 12% and yields as high as 7.3%.

CEFs are simply “built better” than ETFs. These superior dividend vehicles possess several advantages that give them several legs up on your average index fund. The big ones:

- They’re actively managed. Index funds follow a specific set of rules that force them to buy certain stocks only at certain times of the year. Actively managed funds, however, can take advantage of pricing opportunities, picking up stocks at bargain valuations and dumping them when they’ve become too expensive.

- They can “double down” on their own bets. Look at the holdings for any index ETF, and they’ll add up to 100%, as you’d imagine they should. But check out the holdings for some CEFs, and you’ll find that the math doesn’t quite work out. That’s on purpose. Closed-end funds can use debt leverage to invest even more than 100% in their high-conviction picks, which can accelerate not just price gains, but income.

- They can put options to work. Closed-end funds can also use options, which several do to generate even more income.

These tactics can generate more income from just about any equity or fixed-income strategy. But it’s particularly powerful when combined with high-yield assets—like REITs.

So instead of generating 2% to 3% in our average REIT ETF, we can make the most of the sector with these three CEFs. They dish out dividends from 5.4% to 7.3% and trade for as cheaply as 88 cents on the dollar.

Let’s take a look, starting with the still-generous smallest yielder:

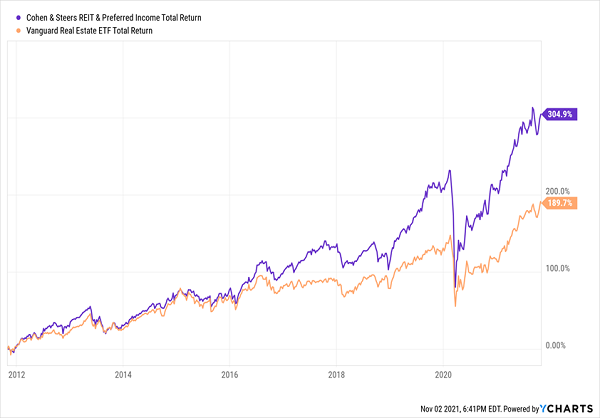

Cohen & Steers REIT and Preferred Income Fund (RNP)

Dividend Yield: 5.4%

This advanced income strategy is exactly why we look to CEFs over ETFs. The Cohen & Steers REIT and Preferred Income Fund (RNP) is an income-oriented fund that holds REITs, as well as preferred stock, to generate a high level of yield. And currently, the 300-holding portfolio is split virtually 50/50 between the two assets.

The REIT portion of the portfolio is a roughly 30-stock who’s who of Big Real Estate that spans 11 different property types. That means decent chunks of telecommunications infrastructure play American Tower (AMT), logistics REIT Prologis (PLD), storage specialist Public Storage (PSA) and a gaggle of other real estate names that you’d expect to see in any self-respecting fund.

The rest of RNP’s holdings are preferreds, and standard fare at that. While it does indeed hold a few real estate preferreds, the lion’s share are from financials such as Bank of America (BAC), JPMorgan Chase (JPM) and Wells Fargo (WFC).

Given the stable, defensive nature of preferred stocks, you’d imagine that Cohen & Steers’ hybrid CEF wouldn’t have much wiggle to it compared to pure-play REIT funds.

You’d be wrong.

RNP Torches the Plain Vanilla Competition

RNP injects some turbo via the use of nearly 25% debt leverage so management can sink more funds into its top ideas. That helps to deliver more yield overall, plus wring more returns out of its high-performance real estate holdings.

Would-be investors might be hobbling themselves by biting at current prices, however. A 2% discount to NAV sounds good in theory, as we’re effectively buying RNP’s holdings at 98 cents on the dollar, but that’s much thinner than the average 8% discount the CEF has traded at during the past half-decade.

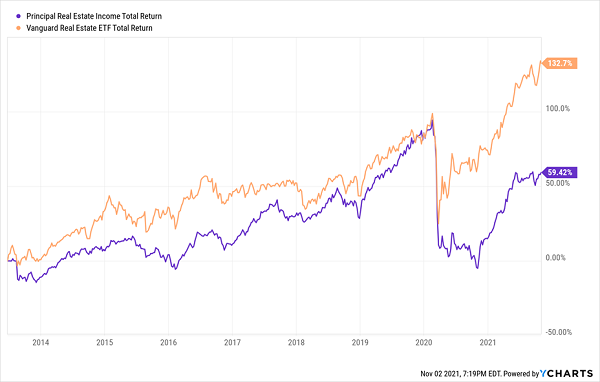

Principal Real Estate Income Fund (PGZ)

Dividend Yield: 6.6%

The Principal Real Estate Income Fund (PGZ) delivers another specialized strategy that you won’t find in a passive product. In this case, the fund is indeed invested almost entirely in real estate securities—but they’re not all REITs.

The lion’s share of PGZ’s assets (61%) are wrapped up in commercial mortgage-backed securities (CMBSes), so it’s primarily a debt fund at the moment. Another 21% of holdings are in U.S. real estate securities, but another 17% is international real estate securities, and the remainder is in short-term investments and cash.

This is a somewhat tighter portfolio of roughly 150 holdings, and unlike with RNP, no equity REITs even make the top 10. The best-held REITs—Invitation Homes (INVH), MGM Growth Properties (MGP) and Sun Communities (SUI)—sit roughly between 15th and 30th at a little more than 1% of assets each.

PGZ also utilizes leverage in hopes of amplifying performance but generally hasn’t achieved the same success as RNP.

Are CMBSes Holding PGZ Back?

The performance gap since the COVID pandemic first erupted is more like a performance chasm, but it’s important to note that Principal’s CEF largely lagged the real estate index for years before that. And while the fund seemingly looks dirt-cheap as a result, at a 12% discount to NAV, that’s pretty much on par for PGZ.

Management sounds off on what has weighed on its debt portfolio thus far: “The Fed conveyed a less-dovish tone as the dot plot shifted higher and preliminary tapering discussions began to take shape. Longer-term inflation expectations cooled, and the 10-year treasury rate fell by 0.27%. Against this backdrop, the portfolio’s holdings of Commercial Mortgage-Backed Securities posted a quarterly return of 6.18% while global real estate securities were up 11.08%.”

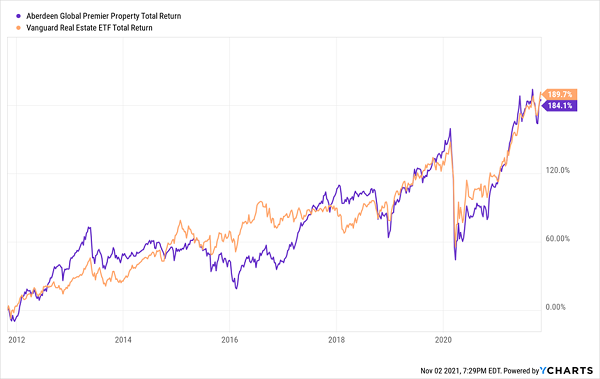

Aberdeen Global Premier Properties Fund (AWP)

Dividend Yield: 7.3%

The Aberdeen Global Premier Properties Fund (AWP) delivers more than 7% in annual income, making it one of the highest-yielding REIT CEFs you can buy. It trades at a modest 4% discount to NAV at the moment to boot.

And it’s the purest REIT play among the three funds here.

(Please note: Aberdeen the firm recently rebranded to Arbdn. It’s pronounced the same, but has no vowels. Yikes. Its fund names still read “Aberdeen” for now.)

Abrdn’s CEF is 100% invested in real estate securities from around the world. Like most “global” funds, the largest slug (58%) is wrapped up in U.S. securities. But that still leaves more than 40% spread across another 16 countries, with Japan (9%), Germany (5%) and the U.K. (4%) representing the top three international weights.

Even then, you have to venture outside the top 10 to find an international REIT. Top holdings are dominated by American firms, including Prologis, AvalonBay Communities (AVB) and Welltower (WELL).

And yet…

AWP Looks Simply Average

So, what’s going on here?

AWP has one major flaw that teaches us an important lesson about REIT-fund investing: International real estate has been historically weak.

This underperformance comes despite a lot of inherent advantages.

AWP doesn’t lay on the leverage too thick, but at 15%, it should still have a decent leg up on its contemporaries. And its expenses of 1.36% are more than your average Vanguard fund but mostly in line with our typical CEF. Moreover, its 7.3% yield is roughly triple the VNQ’s.

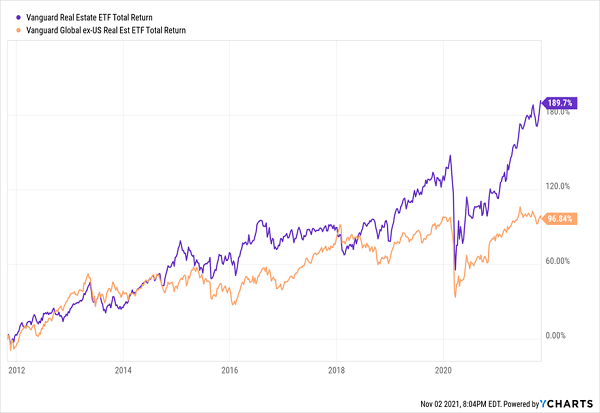

AWP’s mediocre performance largely comes down to the international holdings, which have long underperformed their U.S. counterparts, but especially so during the COVID recovery.

Double the Returns for U.S. REITs in the Past Decade

The “A” Squad: Monthly Payers Doling Out 7%+ Yields

I get it. 7% yields are hard to come by. 7% yields that are paid out monthly—doubly so. That kind of income potential could make an investor look past a lot of blemishes…and to invest in AWP, you’d have to.

Thing is, you don’t have to make that tradeoff. In fact, I can show you exactly how to cash fat dividend checks each and every month without ever settling on quality.

My “7% Monthly Payer Portfolio” is an elite set of high-income, high-frequency dividend payers that, at current prices, are smack-dab in the middle of our ideal “buy zone.” And as the name suggests, these 7% dividends are paid out to investors each and every month.

Many of the picks in my “7% Monthly Payer Portfolio” leverage the power of steady-Eddie holdings to generate not just massive yields, but shockingly aggressive price performance. That allows us to do the unthinkable from an income strategy: double our money much more quickly than traditional blue-chips-and-mutual-funds portfolios.

These dividends aren’t just good.

They’re not just great, either.

They’re downright life-changing.

If you drop $500K—less than half what most financial gurus suggest you need to retire—into this powerful portfolio now, you’d kick-start a $35,000 annual income stream. That’s nearly $3,000 a month in regular income checks!

The time to get in is now, while you can still buy these names at bargain prices. Click here to get everything you need—names, tickers and my full research—instantly!

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Discover the next wave of investment opportunities with our report, 7 Stocks That Will Be Magnificent in 2025. Explore companies poised to replicate the growth, innovation, and value creation of the tech giants dominating today's markets.

Get This Free Report