The 10-year Treasury is storming past 1.6% yet again. Look out, high yield!

I kid because I love (income). And one-point-six just doesn’t do it for me. Plus, remember, this bounty does not escape the tax man. Any interest income we earn from Treasuries—no matter how sad—is subject to federal and state taxes.

So, if we’re multiplying a nest egg (let’s use $500K) by 1.6%, we must remember that the final answer is probably not $8,000 in annual income. Because if we’re raking in income from any other sources, we should lop off a chunk of this for taxes.

Interest Received is the official IRS tax term, for my fellow tax wonks.

“I Owe What on My Lousy 1.6%?”

Now, Treasuries are safe from default because we, the American people, own the world’s default printing press. This is a big reason why US bonds are so attractive. Earth runs on greenbacks and we print them as we see fit.

Inflation risk is another story. To that point, I’m not sure who exactly is buying bonds that pay 1.6% when Fed Chair Jay Powell has flat out said that he wants inflation at 2% per year. Why purchase a 10-year bond at 1.6% that is destined to lose money?

To paraphrase the great Christopher Walken, I gotta have more yield!

And for many of my fellow contrarian income seekers, the only prescription for their income-and-tax fever is:

- Safe, reliable interest payments, combined with a dose of

- Tax write-offs.

Which brings us to municipal, or “muni” bonds. These tax havens collect income from the funding of projects like toll roads in Denver and a convention center renovation in Chicago. Despite headline fears you may have read about muni defaults through the years (in Puerto Rico, for example), they’re actually the safest bonds you can buy other than U.S. Treasuries. Default rates regularly run a lean 0.1% to 0.2%.

Most “high bracket” investors love the idea of tax-free muni bonds. But they aren’t sure where to buy them and often end up using exchange traded funds (ETFs) as their vehicles of choice.

Bad idea. Muni ETFs provide a smooth but unfulfilling ride. They don’t use leverage, and when yields are this low, it’s better to use some to juice the income. Plus, hire the best muni bond pickers.

Most financial websites and television shows feature the popular iShares National Muni Bond ETF (MUB). It’s an ETF, and we need to remember that ETFs are marketing products, good at attracting assets from investors and not as proficient at delivering market-beating returns.

We contrarians prefer to buy our munis via CEFs (closed-end funds). They are the underappreciated way to play these tax advantaged vehicles, for three reasons:

- They are actively managed by pros with a legitimate “edge,”

- Their asset pools are fixed, which means they can (and do) trade at discounts to their net asset values (NAVs), and

- They get access to cheap money, which helps them increase returns with minimal risk.

To be clear, leverage gives muni CEFs higher price volatility than no-leverage ETFs. So, it is up to us, as patient investors, to hold these funds through their ups and downs. Let me show you what I mean.

Every couple of years, CEFs sell off en masse for one reason or another. Liquidity leaves but quickly returns, so investors who didn’t buy the dip soon wish they did.

Also, when markets completely break as they did in late 2008 and March 2020, CEFs get whacked. But they do gradually bounce back as liquidity returns. They’re a better way to play the returning money wave than vanilla ETFs.

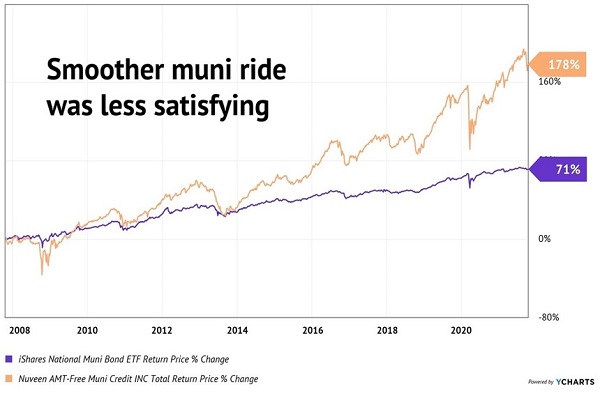

Muni ETFs are delightfully boring to some. They provide such a smooth ride that their vanilla-seeking buyers believe that boring is perfect. After all, they say, we’ve had two epic financial meltdowns in the last 12 years.

An investor who had this crystal ball and piled into munis 14 years ago (in late 2007), probably would have selected the easy joy ride in the MUB ETF. Makes sense in theory, but in practice, they’d have been nearly twice as well off in this CEF, and that’s with the heartburn in 2008 and 2020:

NVG Shows that MUB is a Noob

Our Nuveen AMT-Free Muni Credit Fund (NVG) was the better way to play munis. And it’s no surprise. Remember, Nuveen is the godfather of the sector. Portfolio manager Paul Brennan gets the early phone call on many of the best deals in muni-land.

Second, NVG isn’t hamstrung by “low risk” investment grade paper. The fund’s mandate lets it buy bonds (up to 55% of the portfolio) that are rated Baa/BBB or lower. Giving Paul some room to run is a good thing because he can find valuable bonds in the muni haystack. The ratings are a blunt instrument; Paul is a fine-tooth comb.

MUB doesn’t have this flexibility. The ETF must invest (too) conservatively and keep everything investment grade. With this vanilla strategy comes vanilla returns.

And we’re not simply living in the past here. NVG is still the better muni play.

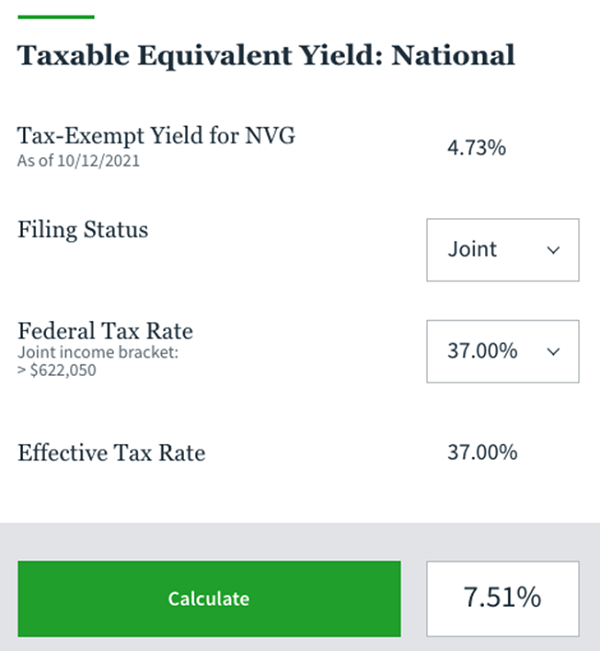

If you’re looking for your own taxable equivalent yield, you can hop over to NVG’s website and click the link on the left side of your screen (it’s the green text below the fund name that says “Taxable Equivalent Yield”) to bring up this calculator:

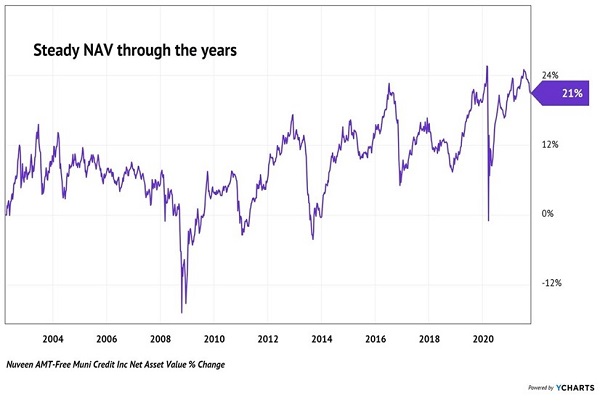

Muni bonds are also nice hedges for an uncertain, elevated stock market. NVG’s NAV never really moves over time. Since inception in 2002, it’s bounced up and down but here we are 19 years later, and its NAV sits a calm 21% higher, not counting the dividends. It means that NVG has done exactly what it was supposed to do—pay its dividend and make some extra spare change to boot:

NVG’s NAV is Boringly Beautiful

Two financial crises and here we are, just ahead of where this fund started nearly two decades ago. Perfect for income investors.

If you’re in a higher tax bracket, or you believe stocks are simply too high (or both!), then NVG is a nice place to hang out. It pays 4.7% (up to 7.5% tax advantaged) and trades for less than the sum of its safe bond portfolio.

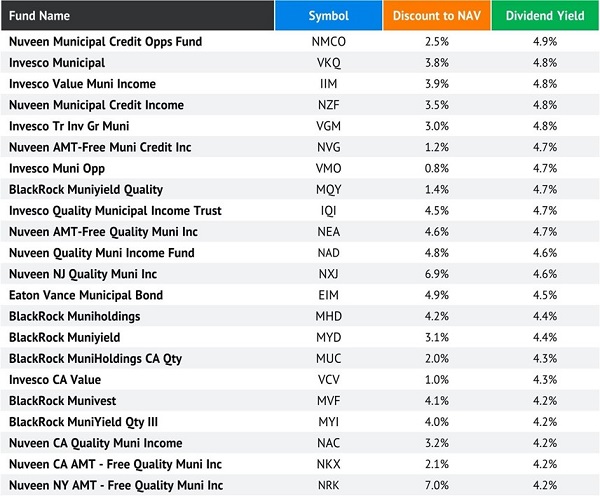

Many of you have requested more of my favorite muni funds, so here are my top 22. Each fund:

- Has a market cap above $600 million,

- Pays a 4%+ Federal tax-free yield,

- Pays its distributions monthly, and

- Trades at a discount to its NAV (net asset value, the market value of its muni bonds minus any debt).

22 High-Quality Muni CEFs, at Discounts

Notice a pattern? It’s no coincidence that Nuveen, Invesco, BlackRock and Eaton Vance dominate the muni leaderboard. These firms have an “unfair advantage” over their competitors and especially over any individual money managers or investors who want to buy munis directly.

What is that advantage? Simply put, they get the first phone call. (If you are selling bonds, don’t you head to the biggest buyers?) These behemoths are buying bonds (and securing bargains) that you and I (and anyone smaller than these big four) never see.

Fortunately, we can bridge this gap of unfairness simply by purchasing these funds. And since they trade at discounts to the value of their holdings, we can actually get our management fee “comped” with a free money kicker to boot.

Discounted muni funds like these are a part of my Monthly Dividend Superstars portfolio. If you like these ideas, you’ll LOVE the payers that are dishing nearly $3,000 in dividends per month—every month—to our fellow income seekers. Click here and I’ll explain how you can retire on 7%+ dividends that are paid monthly like clockwork.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Wondering where to start (or end) with AI stocks? These 10 simple stocks can help investors build long-term wealth as artificial intelligence continues to grow into the future.

Get This Free Report