Years ago, we had a 15-month fling with a promising fund. It traded at a generous discount to its net asset value (NAV) and paid a double-digit dividend.

Plus, its price was rallying!

Brookfield Real Assets Income Fund (RA) checked all the boxes. Unfortunately, it failed the all-important “cash-flow smell test.”

RA’s NAV was declining. Not a good sign given the nebulous nature of its holdings.

The “realness” of RA ends with its name. More than half the portfolio is securitized real estate credit.

And actual infrastructure? The “real assets” headline buyers think they are investing in? Just 30%!

Even in 2018, shortly after the fund launched, it was apparent to us second-level thinkers that RA’s dividend was a mirage. The payout would eventually be cut. We were out.

In the November 2018 issue of Contrarian Income Report, we called RA out as a pretender and sold our shares:

The fund’s generous distribution (10%+) and equally generous discount (6% to 9%) gave us a margin of safety while we awarded their promising management team time to dial in their strategy. But to be blunt, they haven’t.

Their average coupon today pays just 4.8% while they’re on the hook for a 10.4% distribution on NAV. Borrowing cheap money helps fill some of the gap but not enough of it. And the portfolio remains too heavily focused on fixed-rate and longer-duration bonds for my liking.

Let’s take our modest 1% total returns and move on.

After we dumped RA, the fund continued to pay its usual monthly dividend for nearly five more years. The payout defied gravity, but really, management was putting the “RA” in fraud! They continually tapped the piggybank of NAV to keep the monthly dole rolling.

How do I know? RA’s NAV is 37% lower today than the day we kicked it to the curb. Yikes!

Ultimately the levitating dividend came crashing down to reality. Last week, RA announced a 41% payout cut. The fund’s price cratered, and today the fund’s total return since we sold it is only 10.7%.

Which means the fund continued to limp along, delivering an average 2% per year. We were smart to move on, as we had better places for our money.

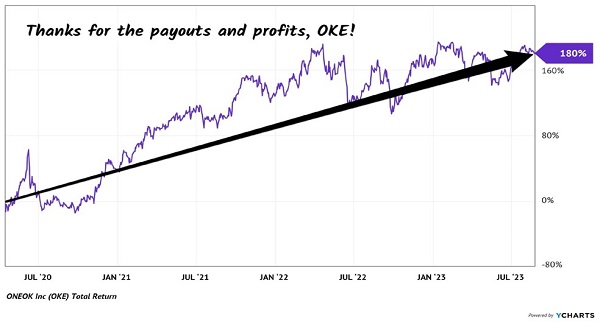

OKEOK (OKE), for example. The energy toll bridge was a better bet on oil infrastructure than hazy RA. OKE owned actual real assets and transportation lines.

And the value! OKE was a contrarian delight when we issued a CIR Flash Alert to buy it in April 2020. The world was shut down, oil futures were trading for less than zero and OKE yielded 13.2%.

OKE Was More Than OK!

The dividend looked dicey, but we reasoned that the company had enough assets to generate cash for the payout. And if not, then hey, even a 20% cut would have left us with a double-digit dividend. Happily, we were rewarded with price gains and an eventual payout hike as OKE survived and soon thrived.

Now we’re looking for the next “obvious in hindsight” dividend play. My bet is on bonds.

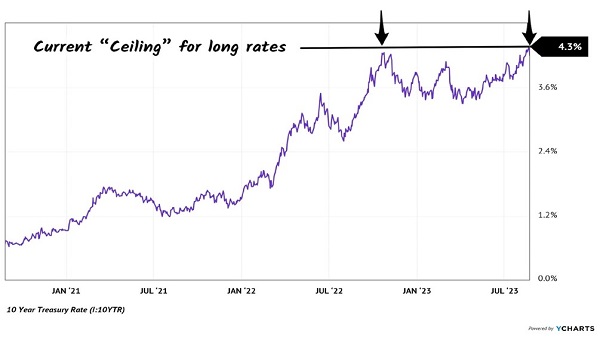

The 10-year Treasury yield is bumping its head—once again—on the 4.3% ceiling. This is the time to buy bonds: when rates are high, and investors hate them!

Buy Bonds Here… and Here

Last week’s labor data reveal a market that is finally slowing. No surprise. The Fed was going to keep hiking rates until wage growth subsided.

Which would only happen in a recession. Think about it—we have a structural shortage of workers. Every business is desperate to hire. Only a “slowdown” would calm down wage growth, and the question is whether we’re looking at a soft landing or a brutal one.

Either way, long rates decline when the economy slows down. Which is bullish for bonds.

But be careful! Not all income funds are created equal. Just ask RA shareholders, who have been collecting dividends and losing most of them in price declines for years now.

NAV matters. Gains are driven by a fund’s holdings. Which is why we always check under the hood—and keep checking.

It’s OK to make mistakes. It happens in high-yield land, where the payouts are often generous for a reason. However, it’s not OK to stick with a loser. Especially one that fails the cash flow smell test. Best to cut bait and buy something better.

NAV, NAV, NAV. It’s all about the NAV.

In fact, higher NAV is a “must have” for my Perfect Income Portfolio positions.

Some yield 7% or more. Others have “OKE-like” 180% upside potential. None have pointless payouts like RA. Click here for my full roster perfect income investments.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Unlock the timeless value of gold with our exclusive 2025 Gold Forecasting Report. Explore why gold remains the ultimate investment for safeguarding wealth against inflation, economic shifts, and global uncertainties. Whether you're planning for future generations or seeking a reliable asset in turbulent times, this report is your essential guide to making informed decisions.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.