I know that plenty of our readers are self-directed investors who love nothing more than to build—and run—their own portfolios. Digging into a fund’s prospectus and annual reports is something they look forward to.

But if you’re like many people, you look to a wealth manager to oversee at least some of your investments for you, or at the very least help with things like tax optimization, financial planning and setting up an estate plan.

There are, however, a few things we need to bear in mind when selecting one. For starters, while many wealth managers can help their clients set up a program that puts them on a path to financial independence, the reality is that wealth managers face intense competition, and that can provide a temptation among less-experienced ones to cut corners.

As a result, some less-experienced wealth managers may end up convincing clients to invest in an underperforming asset because they genuinely think it’ll turn around—and then that doesn’t happen, or worse.

And there’s another thing we need to bear in mind when looking for a wealth manager: whether their services are worth their fees to us.

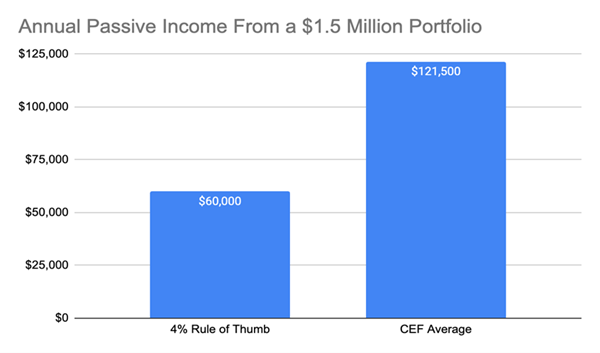

Consider this: A wealth manager charges a client 1% of their net worth in fees. The client wants to retire and replace their $100,000 annual income. With $1.5 million in assets, this investor could retire with a few CEFs and have money left over (since CEFs currently yield 8.1% on average, the client would get $121,500 in passive income, far more than needed and more than enough to reinvest to grow their portfolio and get more income in the future). This would generate around $15,000 in yearly fees for the wealth manager.

Source: CEF Insider

Instead, a wealth manager might recommend the “4% rule,” which has been around for decades. As the name states, the rule suggests withdrawing 4% of your portfolio every year in retirement in order to avoid running out of money.

Trouble is, even the author of this “rule” has abandoned the 4% figure. It also means the client will need to keep working and saving until they have $2.5 million in their portfolio to replace that $100,000-a-year salary.

Now you can save less than that under the 4% rule, but that, of course, means lower income: As you can see above, $1.5 million saved generates just $60,000 a year over 30 years using the 4% rule. To get $100,000 from a $1.5-million portfolio, we’d have to up the withdrawal rate to 6.7%. And that can’t be done over a 30-year period, can it?

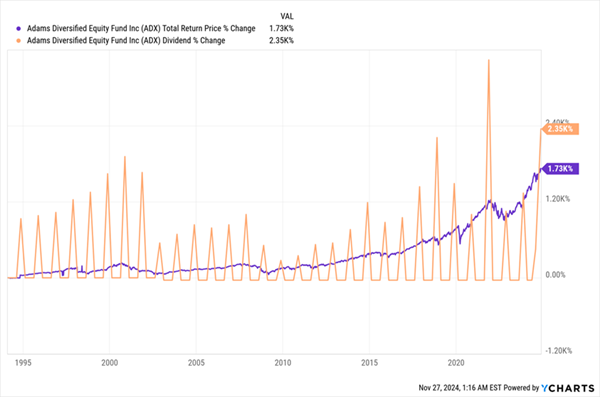

Well, yes, with CEFs it can, since many pay more than that: Like the ever-growing 7.3% annualized dividend the Adams Diversified Equity Fund (ADX) has paid over the last 30 years. That payout, plus the fund’s price gains, resulted in a 1,700% total return over that time (with dividends reinvested).

Strong Wealth Generation From a High-Yielding CEF

Those spikes are year-end special dividends, and they were the main way ADX paid its shareholders.

Hence the fund attracted less interest from income investors, who favored more predictable payouts (even though ADX had a mandate to pay a 6% yield by the end of the year and tended to pay much more).

For this reason, the fund’s discount to NAV was often mired in double digits (though we at CEF Insider loved this approach because it gave management the flexibility to invest more when it spotted overlooked bargains, goosing the fund’s overall return and future income stream).

But earlier this year, ADX’s new management team changed the dividend policy toward a more “normal” 8% annualized yield paid out quarterly. As we reported in our November CEF Insider issue, the change came after pressure from activist hedge fund Saba Capital Management.

Increased activism in the CEF space is another growing trend in CEFs over the last many months, and one we’ve been following closely at CEF Insider.

The shift in the dividend policy has caused ADX’s discount to narrow somewhat, but at 11% as I write this, the fund remains oversold—and a great way to buy the stocks in its portfolio, which include blue chips like Apple (AAPL), Microsoft (MSFT) and Visa (V), for 11% off the market price.

The bottom line here is that with CEFs, it’s very possible to go “DIY” and build a portfolio of funds that lets you retire on dividends alone.

Get 4 Top Managers Working for You—for FREE (and Grab a 9.8% Dividend, Too)

What if I told you I’ve got everything you need to build the retirement income you need … with just 4 funds?

It’s a fact: When you click right here, you’ll discover 4 CEFs from across the economy, holding top corporate bonds, blue chip stocks, real estate investment trusts and even tech stocks.

They’re all run by top managers, and they all trade at discounts. In fact, these discounts are bigger than these managers’ fees, meaning they’re essentially working for us for FREE.

The best part? These 4 funds yield 9.8% on average—enough to generate a sweet $49,000 a year on just $500K invested.

Now is the time to buy them, while we can still get in at a bargain! Click here and I’ll tell you more about this 9.8%-paying “mini-portfolio” and give you everything you need to get started.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Just getting into the stock market? These 10 simple stocks can help beginning investors build long-term wealth without knowing options, technicals, or other advanced strategies.

Get This Free Report