Municipal bonds are too often ignored by investors. Which is a huge missed dividend opportunity.

It’s too bad, because billionaires have been using “munis” to anchor their portfolios for years. And with good reason: as we’ll see in a second, munis can perform well when rates rise. They also pay a high “hidden” yield that beats anything you’d get on a Treasury—and most stocks.

“Munis” Offer Safe, High—and Tax-Free—Yields

I say munis’ yields are “hidden” because they’re tax-free. If you’re in a high tax bracket, I probably don’t have to tell you how valuable a tax-free yield is, but the numbers here are very compelling. Take the 5.4% yield on the Nuveen AMT-Free Municipal Credit Income Fund (NVG), a closed-end fund (CEF) that’s one of the best ways for you to crack the muni market.

Thanks to its tax-free nature, that already-healthy 5.4% yield could be worth 9% or more to you if you’re in the highest tax bracket. That’s the kind of yield you’d normally have to look to a high-risk investment, like junk bonds, to get.

But munis are the opposite of that—renowned for their stability and primed to hold up well no matter what happens with the economy from here.

If recession predictions are accurate, municipalities are well-equipped to handle it, thanks to the reliable revenue they get from local taxpayers. Plus, many cities and states are still holding substantial pandemic-aid funds from the federal government.

History is also on our side here: despite high-profile bankruptcies in places like Detroit and Puerto Rico in recent years, munis’ default rates are so low (less than 0.01%) that research firms have stopped talking about this as a realistic risk.

And if the recession call is wrong and inflation and rates rise further, history tells us that munis do just fine, going by the performance of the benchmark iShares National Municipal Bond ETF (MUB):

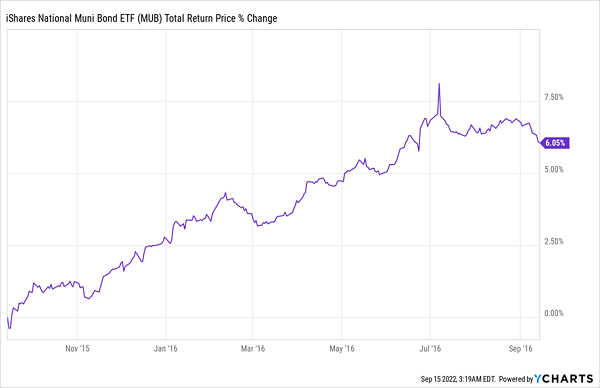

Munis Soared in the Last Rate Hike Cycle

When the Fed started hiking interest rates in late 2015, the muni market fell, but then quickly rose again as investors looked for a safe haven against volatility. And munis continued paying their dividends throughout the entire period, giving investors a much-needed income stream.

Think CEF, Not ETF, When Buying Munis

Finally, unlike an ETF, NVG is actively managed, and with munis, having an experienced manager at the helm is critical. That’s because the muni market is much much smaller than the stock market, so a muni-bond manager is better able to evaluate each bond’s quality. Personal connections help here, too, as the manager can be tipped off when attractive new bonds are issued.

Algorithm-run ETFs, like MUB simply aren’t set up for that kind of an environment, and it shows in a direct comparison of NVG and MUB since NVG’s inception:

NVG’s Active Management Makes It a Better Buy Than an ETF

Before I wrap, let’s talk a bit more about NVG and why I see it as a good buy now.

This nationwide muni bond fund holds assets across the country, making it geographically diversified, while its portfolio of over a thousand bonds protects it from one bond failing to pay out thanks to its massive diversification.

What’s more, about three-quarters of the portfolio is in investment-grade credit, meaning we’re getting the best quality and safest bonds out there. The fund trades at about 1% below the value of its portfolio (net asset value, or NAV) these days, which isn’t a deep discount, but it’s traded as high as 3% above NAV in the last year. I see it as likely to retake those highs as more investors see the high, tax-free yield and low volatility on offer here.

These 4 “Recession-Resistant” CEFs (Yielding 8.5%) Urgent Buys (20%+ Upside Ahead)

This discount to NAV is one of the best things about investing in CEFs. It sounds a bit jargon-y, I know. But the key takeaway here is that CEFs can (and often do!) trade at levels below the per-share values of their portfolios.

Buy when a fund trades far below NAV, you could be primed for big gains as that discount evaporates, catapulting the price higher as it does.

Which brings me to the 4 CEFs I’m urging investors to buy today. These 4 bargain-priced funds offer an outsized 8.5% average dividend now and they pay dividends monthly, too—right in line with our bills!

The real benefit here is that they all trade at totally unusual discounts to NAV—so much so that I’m calling for 20%+ price upside in the next 12 months! But even if I’m wrong and the markets tank, these deep discounts help cushion our funds’ fall—and we’ll still collect their 8.5% payouts!

I’ve put everything I have on all 4 of these funds—their names, tickers, current yields, discounts and more—in a FREE special report you can access right here.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Discover the 10 Best High-Yield Dividend Stocks for 2025 and secure reliable income in uncertain markets. Download the report now to identify top dividend payers and avoid common yield traps.

Get This Free Report