If retirement gets any better than monthly dividend payers then, well, I don’t want to know about it.

Seriously. I’m a simple guy! Pay me every 30 days and I’ll smile and shut up.

And I’ll grin even wider when my monthly dividends add up to 8.7%, 14% or—get this—19.5% per year.

These are not typos. They are real yields from actual stocks and yes, they are spectacular. We’ll highlight them in a moment. But first, let’s review the magic of monthly dividends.

Bills keep showing up every month. Active paychecks from our jobs do not, which is why we rely on payouts. Problem is, most blue-chip dividends pay quarterly. The result? Lumpy cash flow that looks something like this:

We can settle down the heartburn by picking monthly dividend payers. They are out there:

Granted, they are not easy to find. Monthlies tend to be concentrated in a handful of special structures:

The 14.1%-yielding, monthly paying mini-portfolio I’m about to share with you includes BDCs and CEFs, which share an important trait: diversification.

Now spreading our bets doesn’t guarantee success. Ever play roulette?

Buying winners is more important than diversifying. Now let’s look at the monthly payers I teased earlier to see if they deserve our calculated wagers.

Oxford Lane Capital Corp. (OXLC)

Distribution Rate: 19.5%

It’s impossible not to notice a yield as big as the nearly 20% doled out by Oxford Lane Capital Corp. (OXLC).

Oxford Lane is a closed-end fund that invests primarily in debt and equity tranches of collateralized loan obligation (CLO) vehicles. CLOs are similar to mortgage-backed securities (MBSs) in that they’re pooled investments, but rather than pooled mortgages, CLOs typically are pooled corporate loans.

I said it a couple years ago, but it bears repeating: This is an opaque market that your average investor will struggle to even get sufficient information about, let alone even understand.

But here’s what we can see from the outside.

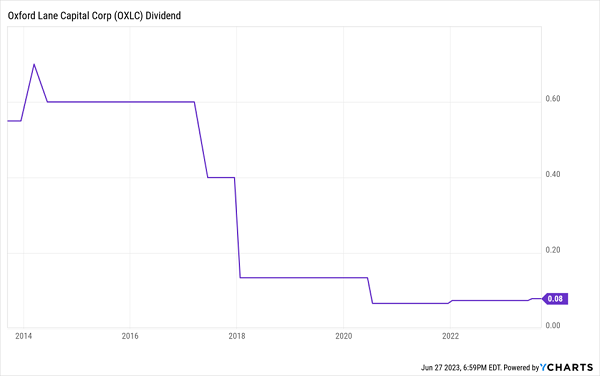

OXLC recently bumped its distribution up from 0.75 cents monthly to 8 cents monthly. Nothing we love seeing more than an already monstrous monthly dividend somehow getting bigger—but sadly, that’s still not close to what Oxford Lane was paying prior to the COVID pandemic (or before that, for that matter).

Oxford Lane’s Dividend: A Couple Steps Forward—After a Few Leaps Back

In the meantime, management has been dealing with a net asset value (NAV) that has been plunging for several quarters, and that’s 30% lower than it was a year ago. Core net investment income (NII) for the most recent quarter plunged by 29% from the year-ago quarter. And the fund has been running a string of both GAAP realized losses and GAAP unrealized depreciation for more than a year.

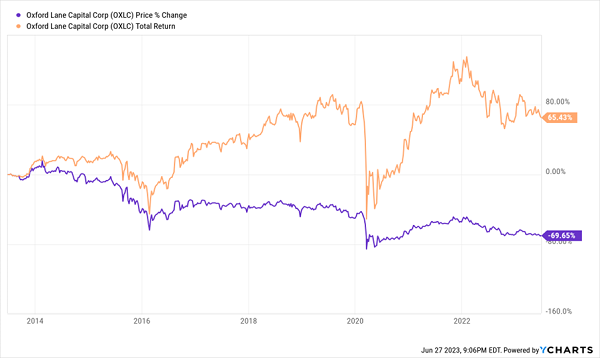

You’ll be unsurprised, then, to find that while the dividends are ample, they’re also bailing out woeful price performance.

OXLC Has Been Pointed South for Years

On top of all that, you’re paying a mint for what you’re getting. Management takes a 3.15% haircut—while interest and other expenses juice the total expense ratio to a wild 13.14%!

Suddenly, that 20% dividend doesn’t feel generous enough.

AGNC Investment Corp. (AGNC)

Dividend Yield: 14.0%

Let’s consider another company dealing in pooled debt that’s a little easier to understand, and that might have a somewhat brighter future.

AGNC Investment Corp. (AGNC) is an internally managed mortgage real estate investment trust (mREIT) that uses heavy leverage to deal in agency residential mortgage-backed securities (MBSs).

While I say “heavy leverage,” that’s just the nature of the business. AGNC’s leverage is actually relatively low right now, at 7.2x versus a historical leverage ratio of 8.2x. It’s a more defensive positioning because, well, the past year-plus hasn’t exactly been a great time to deal in MBSs.

mREITs Have Been Taken to the Cleaners

Think about it: Mortgage REITs buy mortgage loans and collect the interest. They make money by borrowing “short” (assuming short-term rates are lower) and lending “long” (if long-term rates are, as they tend to be, higher).

It’s a good business to be in when long-term rates are steady, and a great business when they’re declining. Drops in long-term rates mean new loans pay less, which makes existing mortgages more valuable. However, rates have been rising—rapidly, at that—and that’s a miserable environment for mREITs.

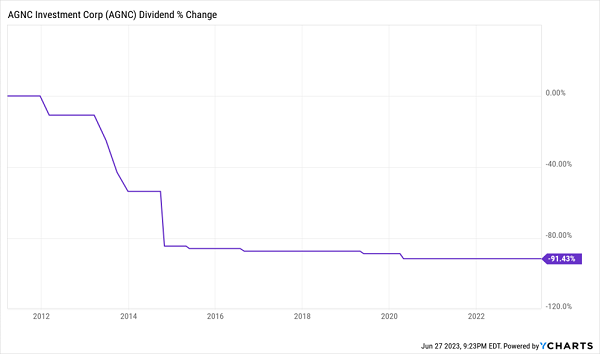

Compound that with AGNC’s longer-term difficulties, and, well, you can see how it’s difficult to trust this mREIT’s dividend, juicy and monthly as it might be.

AGNC: A Long History of Shrinking Payouts

That said: While you might want to avoid AGNC if you’re looking for secure retirement income, now might not be the time to bet against it, either. Management isn’t completely incapable—they smartly sold more than 17 million shares above AGNC’s book value last quarter. And if we are nearing the end of Fed Chair Jerome Powell’s hawkishness, a flatter rate environment should ease mREITs’ pain.

Gabelli Utility Trust (GUT)

Distribution Rate: 8.7%

There’s a lot more to like about the Gabelli Utility Trust (GUT), which if nothing else, is a much simpler fund dealing in a much simpler industry: utilities.

Specifically, Gabelli Utility Trust is a CEF that invests in utility companies—which it specifies as “foreign and domestic companies involved in providing products, services, or equipment for the generation or distribution of electricity, gas, water, and telecommunications services.”

I know you know what utility companies are, but I like that wrinkle at the end: telecommunications services. Because while companies like AT&T (T) and Verizon (VZ) don’t fall in the GICS’s definition of a utility company, make no mistake—phone and internet service have become crucial to everyday life, almost on par with things like electricity and water.

Being a CEF, Gabelli Utility Trust is run by human managers—including GAMCO founder Mario Gabelli himself—and uses a decent amount (23%) of debt leverage to provide a little extra oomph to the team’s picks.

I’d say that’s working well for them.

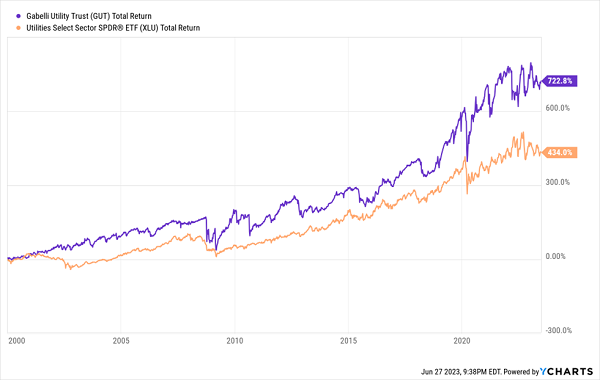

Gabelli Utility Trust Has Crushed Plain Index Investing

Clearly, GUT is a little more volatile than what you’d expect out of a utility fund, but if the outperformance is there, what’s not to like?

Well.

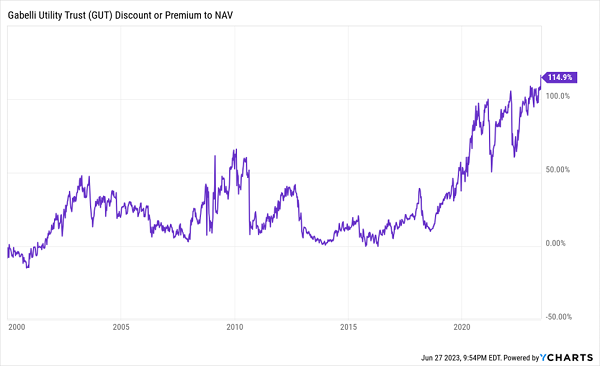

That’s Not Percentage Growth in Premium to NAV. That IS the Premium to NAV.

Gabelli Utility Trust’s premium to NAV is so astoundingly high, at nearly 115%, that it defies belief, but several data providers will back up that number. In fact, GUT has long traded for an absurd premium—its five-year average premium is just above 70%—it’s just getting more absurd.

And to throw a cherry on top of this, utilities trade at a historically high P/E, to boot, so when you buy GUT, you’re overpaying Gabelli to overpay for utilities.

8%-Yielding Blue Chips That Pay EVERY MONTH

I can’t knock on Gabelli too much—they’re skilled managers, and GUT has clearly been able to produce big returns despite (in fact, because of) an outrageous overvaluing of its CEF.

But even with an 8%-plus dividend to act as padding, a valuation reset is too high a risk—it could set investors back by years.

If we want to retire comfortably, we have to be comfortable with our retirement holdings. And for that, you need to target the reasonable businesses trading at reasonable prices, like the ones I hold in my “8% Monthly Payer Portfolio.”

The point of this exclusive portfolio isn’t just earning high levels of yield—it’s earning high levels of yields by leveraging steady-Eddie holdings that won’t have you waking up in cold sweats every few nights.

You don’t need to be anxious about bleeding your nest egg dry, either. The income this portfolio can generate is so rich, it can sustain a retirement on dividends alone.

Do the math: A mere $500,000 nest egg—less than half of what most financial gurus insist you need to retire—put to work in this powerful portfolio could generate a $40,000 annual income stream.

That’s more than $3,300 every month in regular income checks!

Even better? The current bear market has provided us with a rare gift, pulling many of these monthly dividend stocks back into our “buy zone,” where we can grab them at bargain prices. Click here to learn everything you need about these generous monthly dividend payers right now!

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

MarketBeat's analysts have just released their top five short plays for April 2025. Learn which stocks have the most short interest and how to trade them. Enter your email address to see which companies made the list.

Get This Free Report