Few folks know it, but there’s a comically ignored indicator that regularly hands out safe 8%+ dividends—plus payouts that surge double-digits.

I’m talking about insider buying.

When it comes to the buys and sells of the folks in corporate C-suites, Peter Lynch said it best: “Insiders may sell their shares for any number of reasons, but they buy them for only one: the think the price will rise.”

Far be it for me to “edit” Lynch, but I’d add one more thing: these ballers also think the dividend is safe.

Think about it for a second: dividend safety is priority No. 1, 2 and 3 for income investors (I hear it from members of our Contrarian Income Report high-yield service all the time!). Now imagine you’re the CEO of a company and want to not only keep your income safe but that of your colleagues and millions of shareholders, as well.

That’s a very nice alignment between management’s interests and ours. And a dynamite indicator of payout safety, too.

With that in mind, let’s zero in on two insider faves: an industrial firm whose dividend soared 77% in 5 years and a closed-end fund (CEF) trading at a (rare) discount—and throwing off a rich 8.3% payout as I write.

Insider Buy No. 1: This CEO Has $5 Million Piled Into This Surging Dividend

Let’s start with Graco (GGG), whose president and CEO, Mark Sheahan, has more skin in the game than most honchos. SEC filings show that on July 31, he bought 1,263 shares for a total cost of $99,828. That brings his total hoard to 62,986 shares, with a value north of $5 million at the current share price.

That’s a big endorsement from Sheahan, who only became the industrial firm’s president and CEO in June. Before that, he was CFO and treasurer, so we can be sure he has a firm grasp on Graco’s business.

Graco catches our attention for other reasons, as well. For one, it’s what I’d call a large midcap stock, with a market cap around $13 billion.

We love midcaps because they tend to be more domestic-focused than large caps, and therefore less exposed to geopolitical mayhem and the strong US dollar. In fact, both of those “risks” are benefits for Graco because it’s profiting from multinationals’ rush back to the US—the so-called “onshoring” trend.

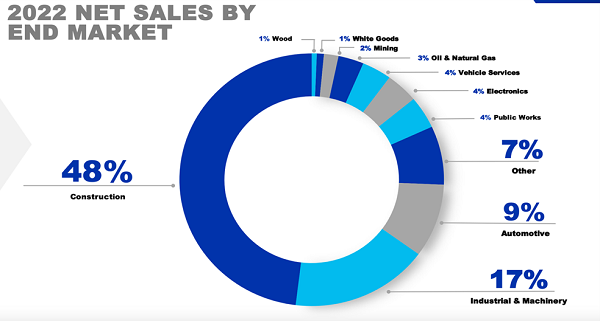

The company, which deals in fluid management-products (think paint sprayers and automatic lubrication systems for heavy equipment), relies heavily on the construction industry (48% of 2022 net sales). And while that does introduce some cyclical risk, onshoring, along with other trends, like the housing shortage and an ongoing flood of government infrastructure dollars, have a long way to run yet.

Moreover, Graco does have some diversification from the other 42% of its sales, which come from a wide array of sectors:

Source: Graco second quarter investor presentation

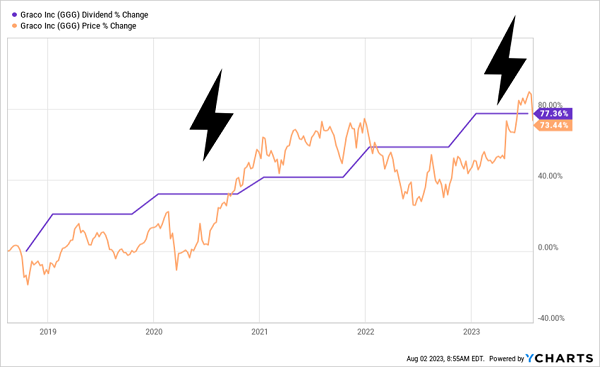

Graco’s 1.2% yield is uninspiring, but it’s the payout growth we’re interested in here: in late 2021, the firm announced a 12% raise and followed that up with another 12% hike late last year—its 25th and 26th straight hikes. Those big raises have pulled the share price higher, a reliable phenomenon I call the “Dividend Magnet”:

Graco’s Dividend Magnet Goes to Work

With a safe 47% of free cash flow paid out as dividends in the last 12 months and plenty of trends in its favor, Graco has what it takes to keep its dividend, and share price, popping.

Insider Buy No. 2: An 8.3% Payer With (Rare) Management Skin in the Game

CEFs are among our top high-yield plays at Contrarian Income Report, for two reasons:

- Big dividends: The average CEF pays 8.3%, with more than half of these 500 or so funds paying monthly, and …

- Big discounts: CEFs generally have the same share count for their entire lives, so they regularly trade at different prices than the per-share value of their underlying portfolios (called net asset value, or NAV, in CEF-speak). We can rack up some nice gains by buying when discounts are unusually wide, then “riding along” as they close, propelling the stock higher.

CEFs aren’t known for insider ownership: a Barron’s study back in the mid-2010s, for example, showed that out of 558 CEFs around at the time, nearly half (269) had none at all!

So when we see an insider buy at a CEF, we take note. And the latest moves by David D. Grumhaus, president and CEO of Duff & Phelps—a subsidiary of Virtus Investment Partners, are interesting, indeed.

On June 16, he picked up 2,500 shares of the Duff & Phelps Utility and Infrastructure Fund (DPG), then followed that up on July 31 with another 2,500-stock buy. The entire 5,000-share haul is worth around $50,000 at today’s prices.

That goes along with another $37,000 of shares in two other Duff & Phelps funds. Sure, these amounts may seem small for a CEO, but given the small size of these funds (DPG’s market cap is just $379 million), they’re meaningful.

They also prove what we CIR members already know: utilities are primed for gains as interest rates top and roll over, pulling down Treasury rates—and sending investors looking for alternatives, like high-yielding utility and essential-services stocks. (The average utility yields around 3% now, more than twice the typical S&P 500 stock.)

DPG holds a nice mix of utilities (63% of the portfolio), pipelines (25%) and infrastructure plays (10%), including top holding NextEra Energy (NEE), a renewable-energy leader that’s rarely cheap (but we can buy for 12% off, thanks to DPG’s discount to NAV):

Source: dpimc.com

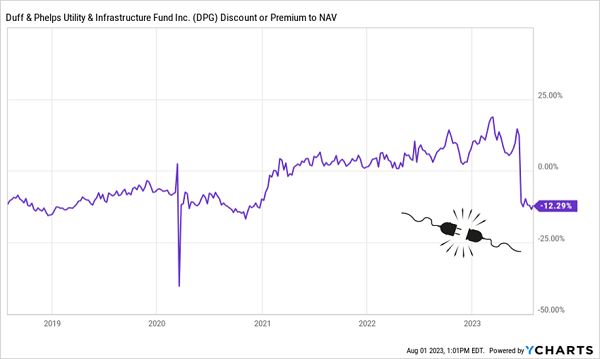

Speaking of the discount, that 12%-off deal is rare: it only exists because DPG dropped on news of a dividend cut announced June 15, the day before Grumhaus’s latest buy:

DPG’s Discount Loses Power

Management said the cut, from $0.35 a share quarterly to $0.21, was due in large part to the higher cost of leverage—the fund has borrowed against about 28% of its portfolio, which isn’t particularly high for a CEF.

But even with the cut, DPG’s forward yield is still 8.3%. And Grumhaus (like us) knows that the best time to buy a high-yield asset is often right after a payout cut. After all, the last thing management wants is to have to bring in another cut (especially if they’ve got their own cash on the line!).

Moreover, with rates topping (and likely heading lower), DPG’s borrowing costs should drop. That, along with likely gains for utilities, sets the stage for the fund’s next growth spurt.

Let Me Build Your “Dividends-Only” Retirement (With Safe 8%+ Payouts)

Dividend Magnets. Safe 8.3% payouts. Insider buying. These are all guiding lights we use at Contrarian Income Report to navigate our way to the “holy grail” of investing: a retirement funded by dividends alone.

As I write this, our CIR portfolio yields 8.1%, and many of our picks pay more—up to 14% yields—many of which are paid monthly.

These holdings are the keys to our system, and I want to share them with you now. Click here and I’ll tell you about our “no-withdrawal” approach and give you the opportunity to download 2 Special Reports naming my very best high-yield buys. You’ll also get to “road test” Contrarian Income Report—and its portfolio stuffed with high-yield stocks and CEFs—for 60 days.

Don’t miss this opportunity to put the daily gyrations of the stock market behind you—and fund your retirement for years to come with safe, high dividends.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Which stocks are likely to thrive in today's challenging market? Enter your email address and we'll send you MarketBeat's list of ten stocks that will drive in any economic environment.

Get This Free Report