Look, I know pretty well everyone loves ETFs—mainly for the cheap management fees.

But here’s the thing: ETFs—especially dividend-growth ETFs—are almost always a raw deal. You’re better to go with carefully chosen individual stocks instead.

Today I’m going to prove it, with two popular ETFs whose lousy performance is costing investors thousands in lost gains. So we’re going to “swap” these losers for two terrific stocks whose payouts have exploded 379%+ in the last decade.

Their secret? An eye-opening “Dividend Magnet” pattern no one’s talking about (but as you’ll see in a moment, they should be).

Let’s start with the laggards, then move on to the Dividend Magnet—and these two overlooked individual stock buys.

Why Dividend-Growth ETFs Are a Mess

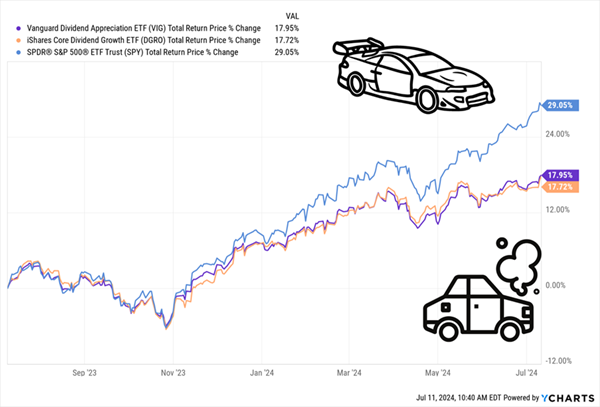

Vanguard and iShares are the top-two names in the ETF space. That’s not news, I know. But the lousy performance of their iShares Core Dividend Growth ETF (DGRO) and Vanguard Dividend Appreciation ETF (VIG) may be news to you.

Take a look at how this duo (in orange and purple, respectively) have fared against the benchmark S&P 500 ETF (in blue) over the past year:

S&P 500 Laps Dividend-Growth ETFs

As you can see, the S&P 500 clobbered this duo, with a 29% total return, compared to roughly 18% for VIG and DGRO.

And it’s not like you’re getting big dividends for your trouble here! VIG yields a paltry 1.8% as I write this, while DGRO does a bit better, at 2.3%.

Dividend-Growth ETFs Should Have a Built-In Advantage

This is particularly shocking when you consider that these ETFs have an edge that should make them shoo-ins to top the market, and it’s right in their names: dividend growth. That’s because a rising payout is the No. 1 driver of price gains.

That might sound surprising, as most folks see dividends and share prices as different animals. But it comes down to the “stair-step” pattern of a rising payout, which pulls the share price higher at every turn. A “Dividend Magnet,” in other words.

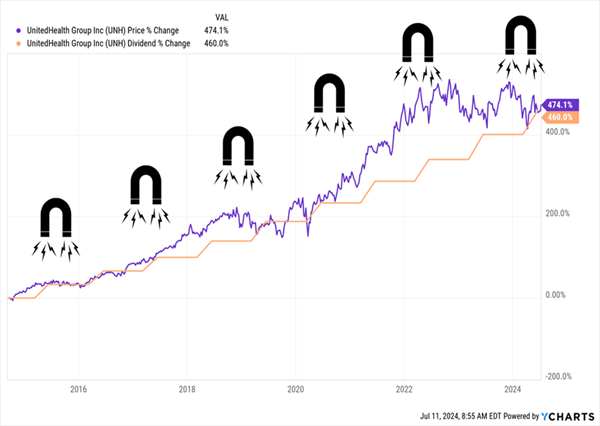

Consider UnitedHealth Group (UNH), which drops big payout hikes on the regular.

We held UNH in my Hidden Yields dividend-growth advisory from January 2020 until December 2022. In that short time—not even two years!—the payout popped 53%, pacing the stock to a stellar 75% price gain (83% with dividends included).

That fat return was the extension of a “dividend-up, share-price-up pattern” we’ve seen in UNH (and many other dividend growers) for years.

Look at this chart of UNH (which has since re-entered the Hidden Yields portfolio, by the way) over the last decade. The power of its Dividend Magnet is unmistakable:

UNH’s “Dividend Magnet” Powers Its Share Price …

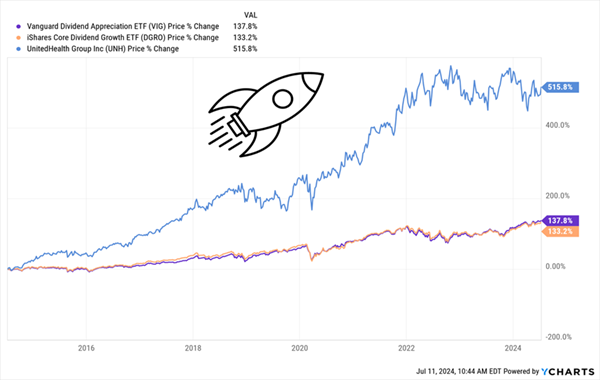

That, by the way, crushed our dividend-growth ETFs. It wasn’t even close!

…Which Soars Past Dividend-Growth ETFs

It’s a textbook example of why we look to individual stocks for strong returns. But this doesn’t mean our two ETFs are completely worthless (though they’re close!). It’s still worth cherry-picking their top holdings to pluck out the fastest-growing payouts.

Let’s do that, drawing one ticker from each:

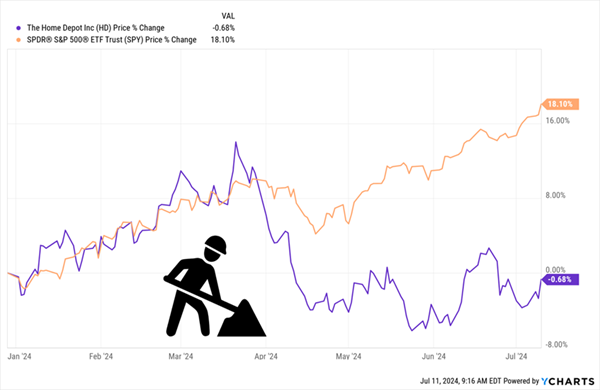

“Cherry-Picked” Dividend Grower No. 1: Home Depot (HD)

The home-improvement giant—the No. 10 holding of the iShares Core Dividend Growth ETF—has posted slipping sales for the last five quarters. And this year, as the S&P 500 soared, HD lost ground:

HD Stock’s “Rebuild” Falls Behind Schedule

That’s because the mainstream crowd has thrown in the towel, for two reasons (both of which are about to change):

- Everyone already reno’ed their homes during COVID, and …

- High interest rates are dragging down both renovation spending and home sales.

Let’s take those one at a time.

Remember COVID? I certainly do. Back in 2020, Home Depot became the official sponsor of my Puerto Backyarda setup at a time when going, well, pretty much anywhere was off the table.

It consisted of:

- Plastic Adirondack chairs,

- A small cooler from the 1990s,

- A sweet mister that pulls water from a five-gallon bucket and cools the entire patio,

- And this t-shirt.

At the time, I’d discovered HD’s speedy home-delivery service, which gave Amazon.com (AMZN) a run for its money.

But here’s the thing everyone’s forgetting about the last reno boom: It was four years ago! I know—it’s hard to believe how fast that time has gone by.

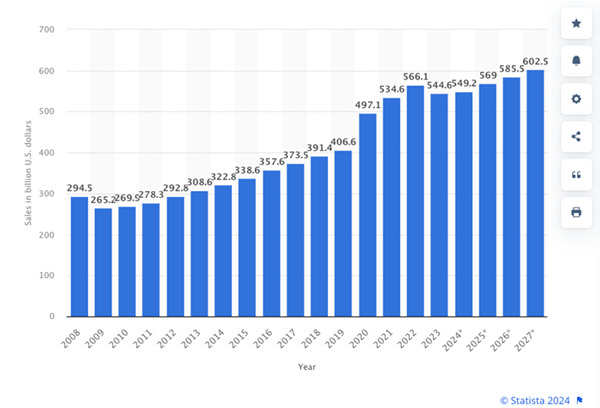

What this means is we’re due for another round of reno spending—and that’s exactly what’s on tap. In the chart from Statista below, you can see US home-reno spending peaking in 2022, bottoming at $544.6 billion in 2023 and then marching higher, till it hits a forecast $602.5 billion in 2027.

“Home-Reno Boom II” Is Set to Roll

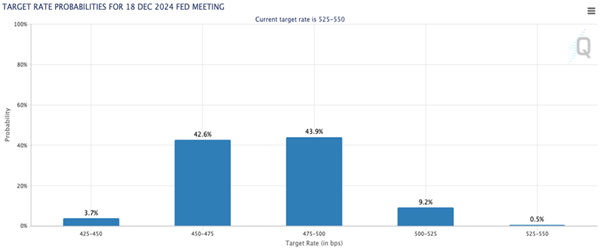

That alone is reason enough to buy HD. But there’s more: Last week’s cooler-than-expected CPI report has boosted rate-cut expectations, suddenly putting the three on the table before the end of 2024, according to futures traders:

Source: CME Group

That puts America’s HD in a great position to turn around its sales (and share price).

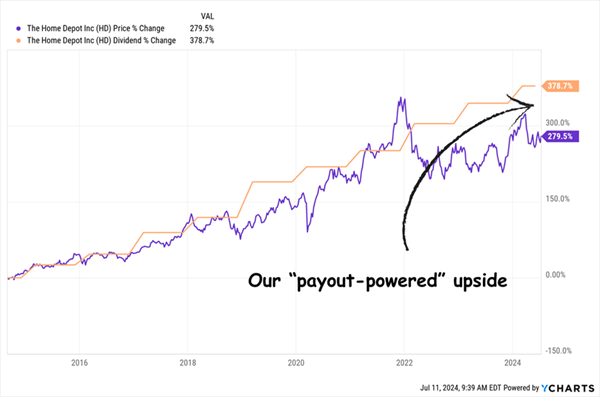

Which brings us to the Dividend Magnet: The stock yields 2.6% but as you can see below, it’s grown the payout an incredible 379% in the last decade. And since the COVID reno boom peaked, HD stock has broken its pattern of tracking the payout higher, showing us exactly the kind of upside we can expect as it (inevitably) catches back up:

HD Dividend to the Share Price: “Let’s Go!”

Even if Home Reno Boom II takes a while to show up, that’s fine: HD’s low payout ratio (the dividend accounts for a safe 47.5% of the last 12 months of free cash flow) means it can keep growing the payout—and ratcheting up the pressure on its share price.

Finally, management’s got plenty of wiggle room on its balance sheet, too. HD’s $38.5 billion of long-term debt (net of cash and short-term investments) is a mere 11% of its market cap, or value as a public company.

“Cherry-Picked” Dividend Grower No. 2: Visa (V)

The demise of the (physical) greenback due to COVID (sorry to bring it up again!) has been a boon to Visa, the No. 7 holding of the Vanguard Dividend Appreciation ETF.

The decline of paper money has sent more transactions flowing down Visa’s payment network. And the firm, which controls 52% of the US credit card market, takes a slice of each one.

Those all add up: Visa posted $33 billion of revenue in fiscal 2023, up 43% from pre-pandemic 2019.

And with US consumers still holding up as inflation ebbs (with interest to follow, as we just discussed with Home Depot), that’s likely to continue.

Meantime, Visa is not a bank—it just processes payments. That critical detail is the reason for the firm’s spotless balance sheet, with $20.6 billion in long-term debt almost entirely “cancelled out” by its $17.7 billion in cash and short-term investments.

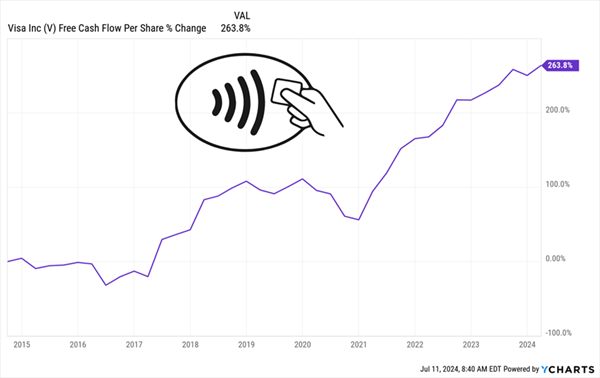

No wonder Visa is a cash cow, with free cash flow per share up 264% in the last decade.

Millions of “Taps” Build Into a Cash-Flow Wave

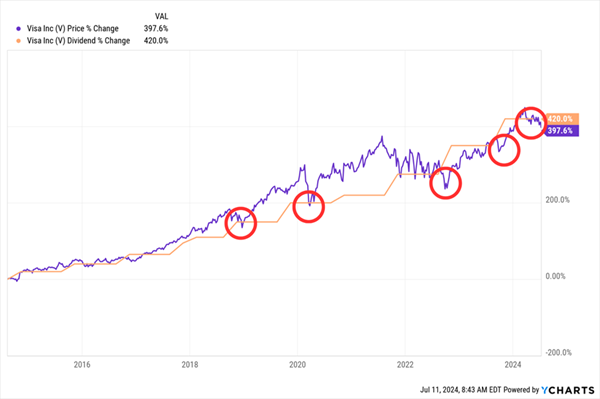

That, in turn, has boosted the payout 420% (ignore Visa’s 0.8% current yield—dividend growth is where the party’s at).

Visa’s “Dividend Gaps” Are Always Buying Opportunities

Finally, let’s talk Dividend Magnet. Once again, we see in the chart above that every time shares of “Big V” fall behind its payout they quickly bounce back and go higher. And that’s exactly the setup we have now.

Yours Now: My Top 5 “Dividend Magnet” Picks (They All Crush ETFs)

I know that a lot of ETF investors would love to amp up their returns—but they don’t want to lose the convenience these funds offer.

My “Dividend Magnet” proves this is not only possible but easily achievable. Simply click here and I’ll tell you all about this breakthrough strategy and show you the best way to profit from it yourself. Plus I’ll give you a free Special Report naming my top 5 “Dividend Magnet” picks with high current yields (one yields 6.7%), explosive payout growth—or both!

Don’t settle for middling ETF returns when you could do so much better (without doing more work!). Learn how my Dividend Magnet plan can help you today.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

MarketBeat's analysts have just released their top five short plays for April 2025. Learn which stocks have the most short interest and how to trade them. Enter your email address to see which companies made the list.

Get This Free Report