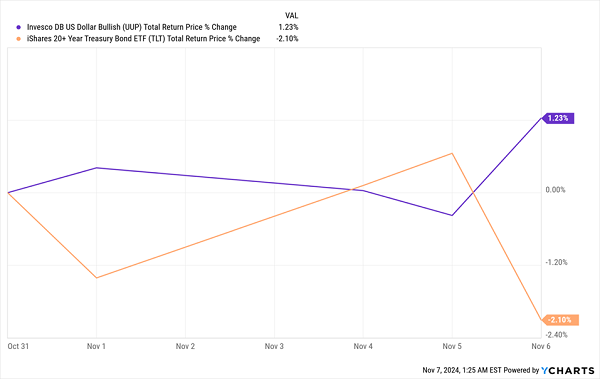

Immediately after President-Elect Donald Trump won his second term last week, the US dollar surged, while US Treasuries fell:

Election Sends Dollar Up, Treasuries Down in Early Trading

Both moves are opposite sides of the same coin: Investors believe Trump’s policies will be inflationary. The theory suggests this would happen for a couple of reasons:

- The US government will spend more, and interest rates will rise higher than rates elsewhere in the world in response. That will attract foreign capital to America while making it less attractive for capital to leave the US.

- All of that extra capital in America will boost economic activity and demand for the dollar. But it will also boost consumer prices.

Now let me explain why both of these theories are incorrect. (And let me be clear we always take a non-political, data-driven approach here at Contrarian Outlook).

Further on, we’ll look at a group of high-income closed-end funds (CEFs) that are set to profit, including a specific one to put on your buy list: It yields a rich 11% today.

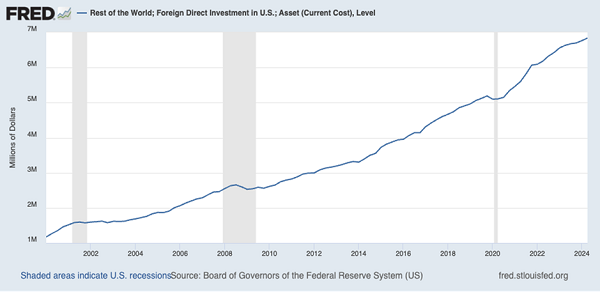

The best way to dive in here is to look at how the trend of foreign investment in America affected bond rates and the dollar long before Trump became president the first time.

America Is a Capital Magnet

Whether the red or blue party is in power, America attracts a lot of money from abroad for a simple reason: It’s a great place to do business.

As the head of Norway’s $1.6-trillion sovereign wealth fund recently said, “Americans just work harder” and have a higher “general level of ambition,” which is why a lot of Europeans love investing in America.

This has been going on for a long time, which is why foreign direct investment in the US has risen strongly since 2000, when the divergence between European and American growth grew especially wide.

America Remains a Magnet for Investment

More investment in the US has helped America’s stock markets grow to become 60% of the planet’s stocks by market cap—even as the US accounts for just 20% of global economic activity.

This, of course, is a big reason why our CEF Insider portfolio is heavily skewed toward American companies.

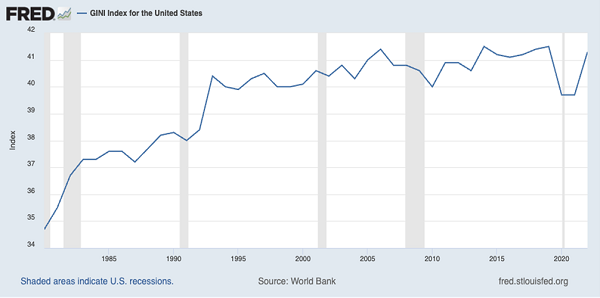

But all economic success comes with a price, of course. In the case of the US, that price has been an inequality in wealth distribution. This trend grew quickly in the 1980s and early 1990s, and things have leveled off a bit since, as you can tell by looking at the GINI index (a metric of how wealth is distributed in a country).

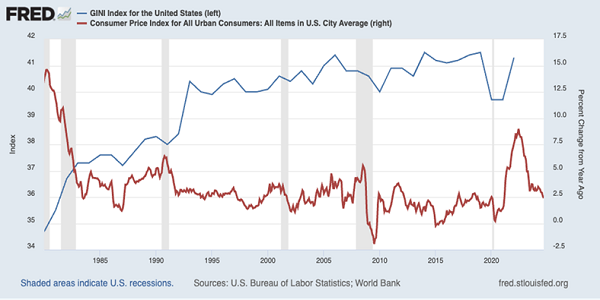

Here’s where the data tells us something else surprising: That inequality has actually helped lower inflation. You can see this seemingly odd correlation by plotting the rate of consumer price inflation (CPI), in red below, from the 1980s to today alongside the GINI index (in blue).

This makes sense if you stop to think about it; if a lot of wealth is equally dispersed, more people will bid for the same goods and services, boosting prices. If wealth isn’t equally dispersed, fewer people can bid on many goods and services, and more people struggle to make ends meet.

To be sure, this isn’t a recipe for a happy society, but it does point to one with lower inflation. And for the most part, that’s what America has seen in the last 50 or so years.

Let’s be honest, no president from either party is going to change this, at least in any rapid way.

As a result, we’re probably going to see less inflation than the market expects in the next four years. After all, if we compare inflation in Trump’s first term to Obama’s two terms, we see that they’re almost identical: Trump’s period saw 1.9% annualized inflation on average, while Obama saw 1.8% annualized.

In other words, Trump’s presidency likely won’t see inflation soar because income inequality isn’t likely to change anytime soon. So in my view, the market is overpricing the odds of a sharp inflation increase.

How to Position Your Stocks and Bonds

This overpricing is an opportunity for us clear-eyed contrarians, who always set politics aside and look at things like this from a clear, investment-focused perspective.

The obvious play is to buy US bonds, which have been oversold after the Trump victory, and sell US dollars, although selling USD is a bit complex for Americans living in the US. That leads us to stocks. But of course, stocks have surged since Election Day.

Fortunately we can easily get into oversold bonds and invest in high-quality US companies that are now well set up to attract foreign capital. The key is to buy oversold corporate bonds issued by US firms.

The bond market is a bit complicated, so I wouldn’t suggest buying bonds individually, especially since the best bonds typically aren’t issued on the open market for anyone to buy, like a stock. However, we can “partner” with talented bond-fund managers who are already playing this longer-term trend of America attracting capital.

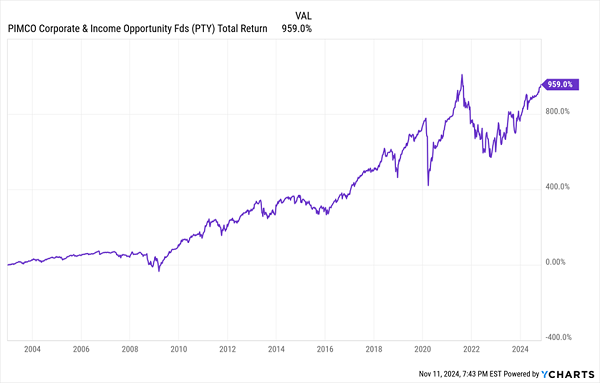

Take, for instance, a CEF called the PIMCO Corporate & Income Opportunity Fund (PTY), which is closing in on a 1,000% return over its 20-year history.

Smartly Run PTY Has Delivered Big Gains (and Dividends)

However, PTY currently trades at a pretty pricey 25.6% premium to net asset value (NAV, or the value of its underlying portfolio). Which is why I recommend PTY’s “sister” fund, the PIMCO Access Income Fund (PAXS).

PAXS, a holding of my CEF Insider service that we’ve reviewed in a couple of recent Contrarian Outlook articles (including our Monday piece), has just a 5% premium to NAV. That’s smaller than the typical markups on PAXS’s siblings in the PIMCO family.

PIMCO funds tend to trade at high premiums for good reason: They deliver strong returns (see the chart above) and have great assets. (PAXS, like PTY, holds a range of US corporate bonds and bond derivatives that now yield more due to higher interest rates and America’s strong economic growth). Hence PAXS’s big returns so far in 2024.

PAXS Jumps on US Economic Strength

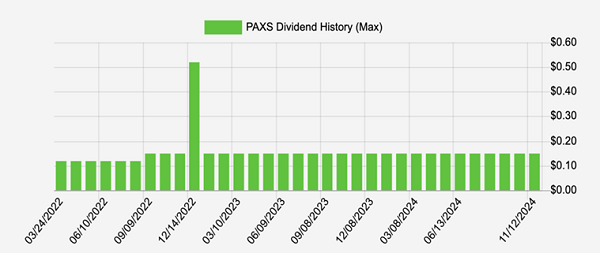

Here’s the best part of all this: PAXS yields 11% today. And it has actually increased its distributions in its short history:

11%-Yielding PAXS Boosts Its Dividends, Drops Special Divs, Too

Source: Income Calendar

This isn’t too surprising: Most of PIMCO’s bond funds raise their payouts over time, in addition to kicking out big current yields. Plus I see more special dividends as likely here. So if you buy PAXS now, you probably won’t get an 11% yield on your initial investment over time. You’ll likely get more.

My Top 5 Monthly Dividend Funds Are Perfect Plays on the “Trump Trade”

Bond funds are, of course, not our only play here. Other sectors, like real estate investment trusts (REITs) and even a select few tech stocks, are primed to soar as the whole “Trump will cause inflation” narrative gets a serious rethink.

The best way to get in? CEFs, of course!

PAXS, which we just discussed, is a great fund, and you can build on it with my 5-CEF “Monthly Dividend Portfolio.” These 5 CEFs hold REITs, bonds, blue chips, techs and more, and they’re all perfectly positioned to profit from the current moment.

And as I said, they pay 10.5% annually and, yes, they pay dividends monthly, too.

I can’t wait to share them with you, so you can kickstart your own monthly income stream (at a 10.5% annualized yield) NOW. And at a bargain price, too.

Click here to learn more and get your free Special Report naming all 5 of these 10.5% monthly payers.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Market downturns give many investors pause, and for good reason. Wondering how to offset this risk? Enter your email address to learn more about using beta to protect your portfolio.

Get This Free Report