What’s better than a big dividend?

A hated high yield.

Especially when the disgust comes from Wall Street analysts themselves. You know, the fanboys who follow the company for a living.

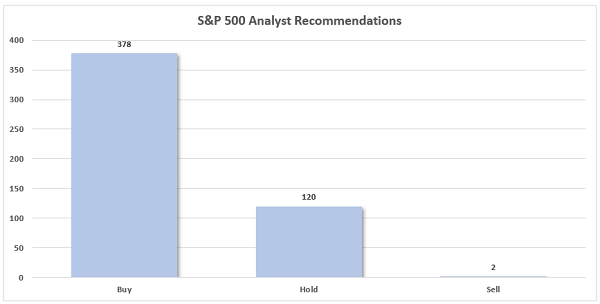

Analysts are paid to be bullish. Let’s face it, nobody wants to hear from a bear. Here’s how unusual is it for analysts to be down on a stock?

There are just two consensus Sell calls across the entire S&P 500. Two.

So, when one of the suits says a business is bad, we should take note, right?

Wrong.

Analysts tend to be trend followers. And as they say in the business, the trend is your friend until it ends.

When vanilla investors read analyst coverage, they think the suit-du-jour is looking out the front of the car. Preferably with GPS! In reality, though, most spreadsheet jockeys are simply projecting old numbers into the future.

As a result, analyst predictions tend to be light in, well, actual analysis. Hence, out-of-favor stocks tend to be a great place for us contrarians to start our independent research.

Today we’ll review seven payers dishing dividends up to 12.9%. The Wall Street guys and gals hate these stocks. A promising start!

Let’s start with a pair of long-in-the-tooth companies that haven’t been exciting growth names in decades, but that currently offer high-single-digit yields that dwarf most non-acronym stocks (REITs, MLPs, etc.).

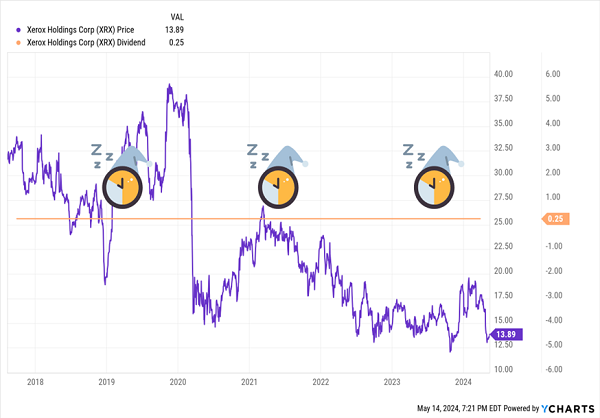

Xerox (XRX, 7.2%) is an outlier in the tech sector, paying more than 7% when most of its contemporaries deliver subpar or no dividends whatsoever.

That’s a great yield from this “Dividend 6” stock, but it’s not because of dividend growth—the payout has been stuck at 25 cents quarterly since 2017. No, it’s because XRX waved bye-bye to growth long ago—the company’s attempts to pivot from its core printing business have been slow and not as effective as hoped, and COVID further lowered the baseline for in-office printing needs.

Shares are in a prolonged downtrend as a result. 2024 has been particularly painful; the stock has lost a quarter of its value so far, erasing most of its late 2023 progress.

Sleepy Dividend, Sleepy Shares

Not many analysts still cover this elderly tech stock, but those who do aren’t enamored. Of the five pros with calls on XRX shares, three call it a Hold and the other two call it a Sell—a weak consensus centered on Xerox’s (nonexistent) growth case.

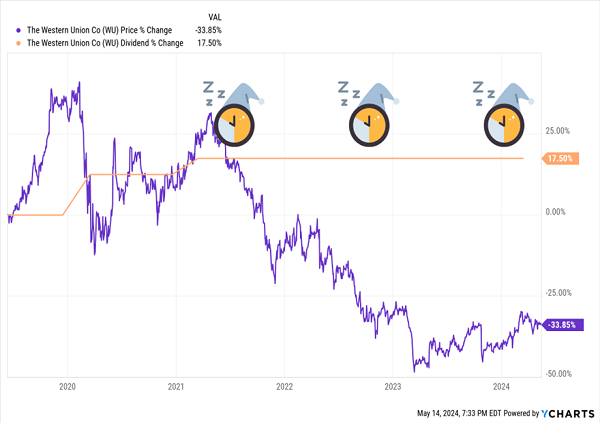

Western Union (WU, 7.1% yield) is in a similar position.

Western Union has fallen behind the technological times, and the money transfer/payment services firm has been hemorrhaging business to younger competitors like PayPal (PYPL), Wise and others. That too has sent shares into longer-term decline, and the dividend, while generous, has been frozen for a few years.

Western Union Won’t Pay Up, And Shares Won’t Wake Up

Wall Street has it out for Western Union. While WU shares have earned a pair of Buy calls, they’re drowned out by a dozen Holds and half a dozen Sells.

Long-term, it’s hard to see a path to growth for Western Union. But there are at least a few encouraging signs. Shares are up 25% from their spring 2023 lows. WU continues to show progress on its “Evolve 2025” initiative—a rollout of new products and improvements, as well as an operational efficiency program. The company recently announced its third consecutive quarter of top-line growth in the digital business (which makes up 21% of revenue). Yes, overall sales are still forecast to dip by 4% in 2024, but that’s stable compared to past years—and the company’s sales are actually projected to tick higher in 2025.

Western Union remains a “show me” stock, but at least it’s starting to show a little something.

REITs

Speaking of hurting businesses, let’s check in with office real estate investment trust (REIT) Alexander’s (ALX, 8.3% yield).

Alexander’s is a hyper-niche office REIT that owns five properties in the NYC metropolitan area and is managed by Vornado Realty Trust (VNO). And like the rest of the industry, ALX shares were crushed by COVID, with the stock losing as much as 50% of its value by 2023. It has rebounded a bit since then amid a wave of return-to-office initiatives, but shares have largely tread water in 2024.

Alexander’s isn’t drowning in Sell calls—in fact, it only has one to its name. But that’s from the only analyst covering the stock right now. That’s a different sign of a troubled company: Rather than put out persistently negative reports, the Wall Street crowd sometimes decides to just abandon coverage.

The biggest red flag on my radar has been ALX’s dreadful dividend coverage. I pointed this out in September 2023, and the situation didn’t improve much through the rest of the financial year. Alexander’s ended up generating $15.80 in funds from operations (FFO) per share for full-year 2023, but paid out $18 per share in dividends during that time.

Still, I wouldn’t bet against ALX here either. Its Q1 2024 FFO coverage was drastically improved; FFO jumped 37% to $4.98 per share, which was more than enough to cover Alexander’s $4.50 payout. And while I don’t think we’ll ever see the same level of workplace in-office time we saw pre-COVID, companies are getting bolder about demanding at least some time in the office—potentially a little more ballast for office REITs like ALX.

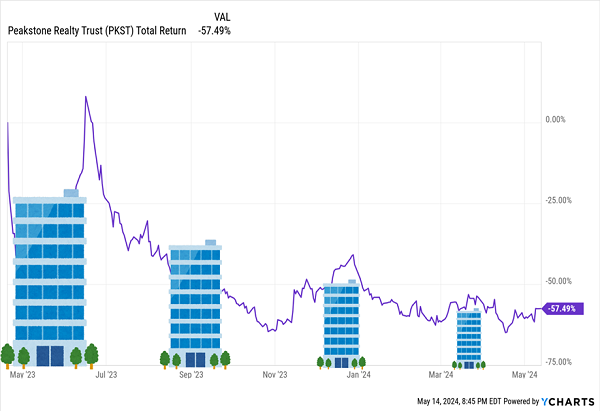

There’s a different reason for the relative lack of coverage on Peakstone Realty Trust (PKST, 6.0% yield): This REIT only went public a little more than a year ago. Still, what attention it has gotten isn’t great, with one Hold and one Sell.

Peakstone is a net-lease REIT with 67 properties across 22 states, with heavy concentrations in coastal regions and the Sun Belt. Its primary property types are office (60% of annualized base rent, or ABR) and industrial (27%), with the remaining 13% spread across various other types of property.

PKST has been slammed since coming public, with shares down nearly 60% since the company went public in April 2023.

Peakstone Is Well Off Its, Ahem, Peak

Wall Street and investors alike might have been too quick to the ax here.

Yes, right now, the majority of PKST’s base rent is office, and that wouldn’t bode well for its long-term prospects. But the company is attempting to reposition the portfolio by maintaining and growing its industrial assets while selling off all of its “other” segment properties and some of its office properties.

In the meantime, PKST trades at less than 5.0 times FFO estimates and has an exceedingly well-covered dividend.

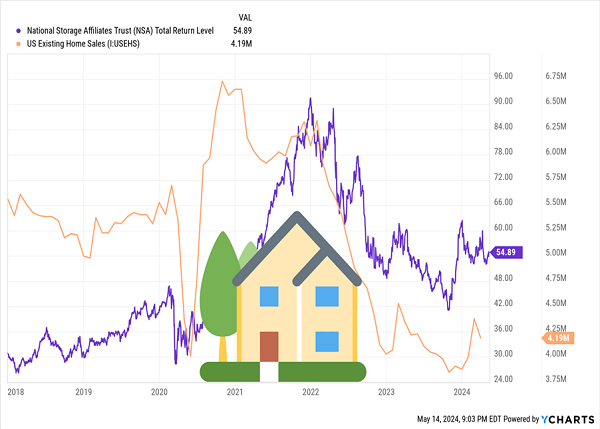

Moving away from office real estate, let’s shift our focus to National Storage Affiliates Trust (NSA, 6.0% yield), a self-storage REIT with 1,050 self-storage properties in 42 states and Puerto Rico. We actually held this name long ago, but we sold it (for a 40%-plus gain) amid a glut of supply and slack demand for these mini-warehouses.

NSA shares actually exploded post-COVID, but virtually all of those gains have evaporated right alongside activity in the housing market.

As Went America’s Housing Boom, So Went NSA

As I’ve mentioned before, NSA isn’t a typical self-storage REIT. It’s actually more of a collective: Its PRO (participating regional operators) program brings in private self-storage operators. It brings in more units through strategic joint ventures and third-party acquisitions.

Wall Street really doesn’t like National Storage Affiliates—it has two Buys, sure, but also seven Holds and five Sells. But like I said about half a year ago: There’s little wrong with NSA itself. Management is competent. The dividend is well-covered at 89% of estimated 2024 FFO. It has just been dealing with a bad environment for all self-storage names: high home prices, high interest rates, and recession fears have hampered the space. That latter point has eased, and NSA and its cohorts’ stock prices have been gradually improving ever since.

Massive Yields, Lousy Ratings

Wall Street is also bearish on a pair of double-digit yields:

Mid- to high-end fashion retailer Buckle (BKE, 10.0% yield) pairs a reasonable regular quarterly payout with what have been substantial annual special dividends in recent years.

Buckle has a thin analyst crowd that’s net bearish on the stock, with one Hold and one Sell. I recently sounded off on Buckle, but in short, while operations have been weaker in recent quarters and no one expects Buckle to reproduce its post-COVID spurt, this retailer is able to capture thick margins, is expected to resume growing its profits next fiscal year, and has a shareholder-friendly management team. There might be better opportunities out there, but it’s silly to bet against BKE.

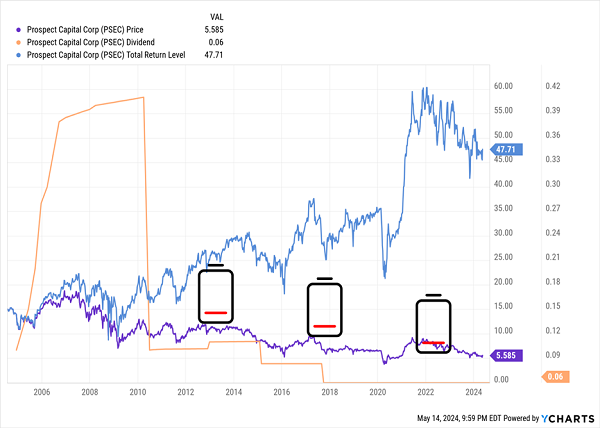

Prospect Capital (PSEC, 12.9% yield) is also lean on analysts, with the two pros covering the stock split at one Hold and one Sell.

PSEC is a business development company (BDC) that invests in 112 companies across 36 separate industries, primarily through first lien and other senior secured debt.

It’s one of the largest BDCs by net assets, but it also has a shoddy track record—one with multiple dividend cuts and share prices to match. While the total-return record is much better thanks to still-fat yields, it’s still worse than the broader market and better BDC peers.

PSEC can never seem to go out of its way, which is why it trades at a perpetually wide discount to NAV (62% currently!), and why the pros are perpetually pessimistic on the name despite that deep value pricing and decently covered payout.

Prospect Capital is another “show me” stock that’s hard to bet on for the long term. But watch out. If Prospect can string together reports like its recent fiscal first quarter operations, which included a net investment income (NII) beat, it could shake out a lot of bearish hands.

How to Retire on Just $500K

But let’s be serious. PSEC’s nearly 13% yield is as juicy as it gets, sure, but would you ever feel “safe” knowing how quick management has been to cut the dividend throughout its history?

That’s not a retirement plan—that’s a roll of the dice!

A real retirement plan is building a portfolio that can generate at least 9% in reliable dividends. And that 9% is an important number—one that will allow you to retire on dividends alone, even if you have a smaller nest egg of, say, $500,000 to work with.

The math is easy: At 9%, you’re generating $45,000 in cash from your retirement account alone. Combine that with Social Security, you’ll have plenty to work with once you’ve moved on from your career.

And if you have an even bigger pile of cash to plug into our 9% “No Withdrawal” Retirement Portfolio, you’re looking at a downright cozy retirement—one where you’ll never have to touch your original nest egg!

The hated stocks above don’t quite fit the bill. But I have plenty of stealth payout plays that do yield the 9% or more that we need to coast forever on dividends alone. Please click here and I’ll share the details on these secure funds with very generous dividends!

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

MarketBeat just released its list of 10 cheap stocks that have been overlooked by the market and may be seriously undervalued. Enter your email address and below to see which companies made the list.

Get This Free Report