The only thing I love more than dividends is dividend growth. And ‘tis the season for payout raises as first-quarter earnings season kicks into gear.

I have my eye on companies that have recently announced dividend hikes of 28%, 52%, even 150%. If we get similar dividend growth this time around, great—more money in our pockets. But just as important is the confidence they’d be communicating with big raises amid an extremely uncertain economic environment.

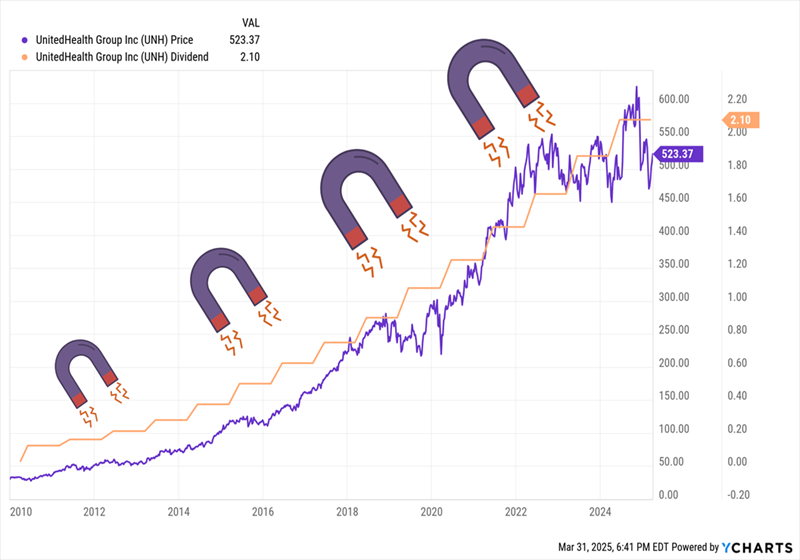

Regular readers know about my “Dividend Magnet” strategy—three signs that can lead to massive price gains. The most important sign is dividend growth, which is management’s way of saying “We’re growing profits, and we know those profits are going to stick!”

Not only do shareholders collect more cash every year—but that extra cash also entices investors to buy more. As a result, the dividend “pulls” prices higher, like we see in this chart of high-quality dividend-growth name UnitedHealth (UNH):

As UnitedHealth’s Dividend Accelerates, So Does UNH’s Stock Price

The coming lineup of dividend announcements is especially interesting because they’re happening during a potentially difficult time for corporate America. Economic data is worsening. GDP estimates are being revised lower seemingly every couple of weeks. Constantly changing tariffs are flustering even the most disciplined planners in the C-suite.

Any company that can announce a bold dividend increase in a difficult environment probably deserves a closer look.

Here’s a quick menu of dividend growers that improved their payouts by an outstanding 28% to 150% last year, and that are expected to make dividend announcements sometime during the upcoming quarter.

Victory Capital Holdings (VCTR)

Dividend Yield: 3.3%

2024 Increase(s): 40.3% (across 4 hikes)

Projected Q2 Dividend Announcement: Early May

Victory Capital Holdings (VCTR) is an investment manager that provides specialized investment strategies to institutions, retirement platforms and individual investors. Specifically, it offers mutual funds, ETFs, separately managed accounts, alternative investments, private funds, brokerage services and more.

It does so through a variety of brands that it has picked up through its acquisitive history, including Munder Capital Management, THB Asset Management, and WestEnd Advisors. Perhaps most notable, though, is Victory Income Investors—the rebrand of USAA Asset Management Company, which it acquired in 2018.

Despite its heavy M&A, Victory Capital’s top and bottom lines haven’t been growing in a straight line, but those arrows are at least pointed in the right direction.

But its dividend has been growing like a weed.

VCTR has a downright odd payout history since coming public in 2018. It initiated a 5-cent-per-share dividend in 2019, put together a streak of quarterly hikes in 2020 and 2021, went to annual raises for a couple of years, and now is in the midst of another multi-quarter streak dating back to March 2024.

Victory Capital Is on Another Heater

During that time, Victory Capital’s distribution has exploded by 840%, including a 40% improvement across the past year’s worth of hikes.

I’ll be keeping my eye on its Q1 earnings report, which likely will be in early May. For one, VCTR typically makes its dividend announcements alongside quarterly earnings, so we’ll find out whether the streak will continue. But also, after nearly doubling on a total-return basis in 2024, shares have become chaotic in 2025—and that report could be a big catalyst for a move in either direction.

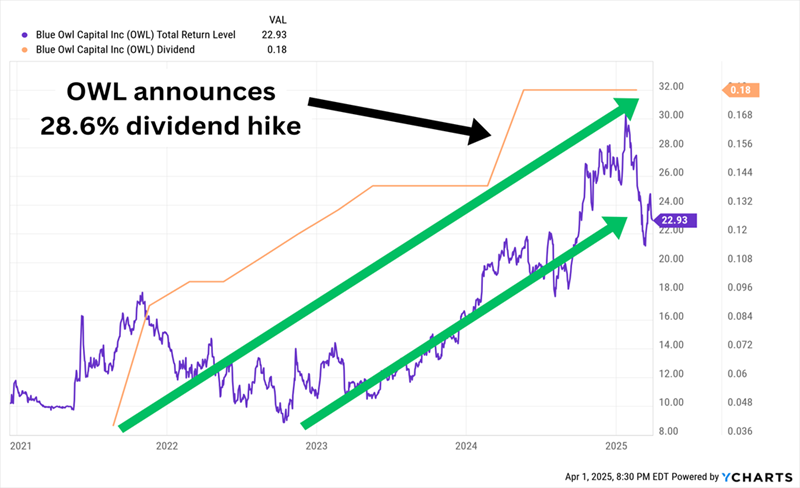

Blue Owl Capital (OWL)

Dividend Yield: 3.9%

2024 Increase(s): 28.6%

Projected Q2 Dividend Announcement: Early May

Blue Owl Capital (OWL) is another asset manager, this one focused on alternatives. It offers a wide variety of capabilities, including direct lending, alternative credit, liquid credit (largely CLOs), real assets, and minority equity stakes (including a budding business of professional sports minority stakes, through its relationship with the NBA).

It’s also the name behind Blue Owl Real Estate Net Lease Trust—a private, non-traded real estate investment trust (REIT)—as well as several business development companies (BDCs), most notably Blue Owl Capital Corporation (ORCC).

Blue Owl has been downright explosive over the past half-decade or so, driving its top line from around $190 million in 2019 to $2.3 billion last year. It too has done so heavily through acquisitions, including private equity real estate firm Oak Street and business development office Ascentium Group. Most recently, on September 30, it bought up alternative asset manager Atalaya, which managed more than $10 billion.

The company spilled a lot of red ink along the way, the worst of it coming in 2021—the year it went public via special-purpose acquisition company (SPAC)—but it turned a $54 million profit in 2023, then roughly doubled that in 2024.

OWL hasn’t been shy about sharing the wealth, even during those unprofitable years. The company started with a prorated 8-cent-per-share dividend in 2021, then gradually increased it for a few quarters before (it looks like) switching to a yearly-raise schedule in 2023. Last year’s raise was nearly 30%.

There’s Some Lag, But OWL’s Dividend Has Been Pulling Shares Higher

It’s difficult not to wonder whether another big year of growth will translate into a significant step up in the payout—but we won’t have to wait long. Blue Owl should make its next dividend announcement sometime in early May.

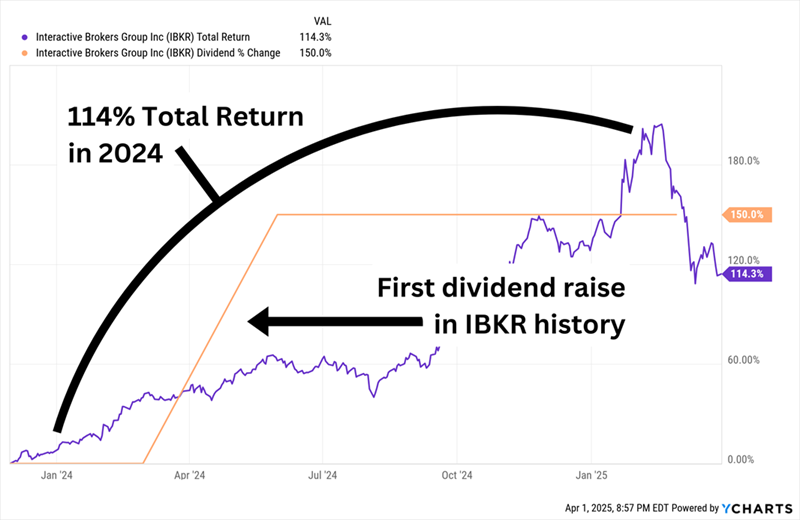

Interactive Brokers Group (IBKR)

Dividend Yield: 0.6%

2024 Increase(s): 150%

Projected Q2 Dividend Announcement: Mid-April

The yield might be chump change, but if Interactive Brokers Group’s (IBKR) future dividend improvements look anything like its 2024 raise, it won’t be that way for long.

Interactive Brokers is one of the world’s largest electronic brokers, providing automated trade execution and custody of securities, commodities and forex in more than 160 markets to clients in more than 200 countries and territories. It doesn’t just serve individual investors—it also provides service to financial advisors, trading groups and hedge funds.

IBKR has taken full advantage of the current bull market, nearly tripling its top line in three years and growing profits by about 150% over the same time period. Trading volumes have surged, as have margin loans. Higher interest rates have also helped it generate more money on its (and its clients’) cash.

And while it took some time, that success finally spilled over into the dividend. IBKR had kept its distribution level at 10 cents per share since 2011(!), but in mid-April 2024, it punched through the glass ceiling and raised its dividend by a whopping 150%, to a quarter per share.

IBKR Shares More Than Doubled in 2024, Too. Coincidence? I Think Not.

Interactive Brokers’ full-year 2024 results crushed expectations, while quarterly commissions and trades were up huge year-over-year. So I’m excited to see what IBKR has to offer when it makes its next dividend announcement, likely in concert with its April 15 earnings report. We probably won’t get another 150% banger, but given that IBKR’s current dividend represents a paltry 13% of 2025 earnings estimates, management has a lot of room to make another splash.

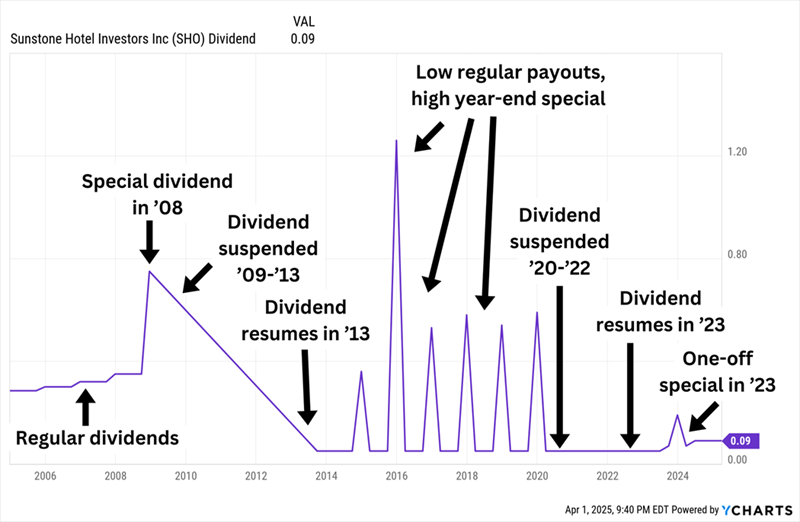

Sunstone Hotel Investors (SHO)

Dividend Yield: 4.0%

2024 Increase(s): 28.6%

Projected Q2 Dividend Announcement: Early May

Sunstone Hotel Investors (SHO) is a small hotel REIT whose properties are located in gateway and resort markets. Its tight 15-hotel portfolio includes the Wailea Beach Resort, Four Seasons Napa Valley, The Westin in downtown Washington, D.C., and Andaz Miami Beach—formerly The Confidante, a Miami Beach oceanfront hotel it acquired in 2022 and has been revamping ever since.

Sunstone has spent the past few years recovering from COVID, which slashed its revenues and, in 2020, drove a 165% plunge in adjusted funds from operations (AFFO) into deeply negative territory.

Like with many hotel REITs, Sunstone was also forced to temporarily suspend its dividend—traumatizing to shareholders, but for SHO, just a single chapter in one of the wildest dividend histories I’ve ever seen.

It’s hard to tell what SHO has planned next. The company resumed its dividend in 2022. In 2023, it raised its base dividend to 7 cents, and it looked like it was primed for a return to quarterlies-and-specials, with an additional 6-cent special at the end of that year. However, 2024 saw a raise in the base dividend (to 9 cents) but no special—though admittedly, Sunstone took a step back financially.

Sunstone’s next dividend announcement, expected in early May, might provide more clarity into whether SHO plans to continue significantly improving its regular dividend, or rely more on specials going forward.

Western Midstream Partners LP (WES)

Dividend Yield: 8.6%

2024 Increase(s): 52.2%

Projected Q2 Dividend Announcement: Mid-April

Western Midstream Partners LP (WES), is an energy infrastructure company that manages 21 gathering systems, 75 processing and treating facilities, and more than 14,000 miles of pipeline spread across seven natural gas pipelines and 11 crude oil/natural gas liquids pipelines. It does so on behalf of Occidental Petroleum (OXY), which owns nearly 45% of the company and manages WES via its subsidiary, Western Midstream Operating LP.

WES is the biggest yielder among the five stocks listed here, at more than 8% at current levels. It’s also the only one that’s produced a positive return in 2025.

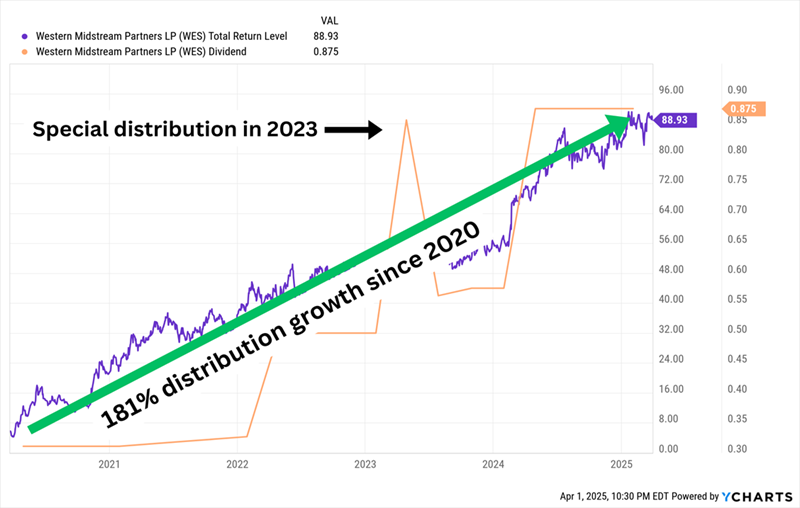

Those year-to-date gains have added to a whopping 1,470% ascent from the stock’s COVID lows. Western Midstream has achieved that through relatively steady growth, as well as maintaining an optimal cash-flow balance of investing in its business while keeping shareholders happy with growing distributions—including an impressive raise of more than 50% last year.

WES Pumps Up Its Payout

I’m interested to see what WES does in mid-April, when it’s expected to make its next distribution announcement. Alongside its Q4 2024 report in February, it also announced a new project: the Pathfinder Pipeline, which will be capable of moving more than 800,000 barrels per day of produced water into the Delaware Basin. That and other projects could see Western increase its capital expenditures over the next few years—and might leave less room for ambitious distribution raises.

My 2025 Dividend Plan: Buy the Best Yields of 2035 Today!

I’m going to be laser-focused on stocks like these all year long.

That’s because my 2025 investment plan is to buy “Dividend Magnets”—stocks that boast some of Wall Street’s fastest-growing dividends, which in turn attract more investors and “pull” prices higher, providing us with the potential for a wicked 1-2 punch of total returns.

Some of these stocks are in Wall Street’s far-flung corners, but a few of them are hiding in plain sight. In fact, one of my favorite Dividend Magnets is a blue-chip Dow component!

I’m currently zeroed in on 5 stocks I see as the next Dividend Magnet winners. They’re my top picks for the fastest-growing payouts—and share prices—through 2025 and beyond.

And I’m going to share them with you right now. Simply click here and I’ll tell you more about these 5 “Dividend Magnet” winners, including a Dow blue-chip, and give you access to a free Special Report revealing their names and tickers.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Learn the basics of options trading and how to use them to boost returns and manage risk with this free report from MarketBeat. Click the link below to get your free copy.

Get This Free Report