Investing for the future is essential, as is considering your risk tolerance. All types of investing come with the risk of losing money, but there are strategies that you can use to limit your risk. By balancing the potential for growth with more conservative investments that tend to retain value in times of volatility, you can set yourself up for success toward your unique financial goals.

Determining your risk tolerance is crucial before you start investing. Read on to learn more about how to determine risk tolerance for investing and how you can use it to refine your portfolio.

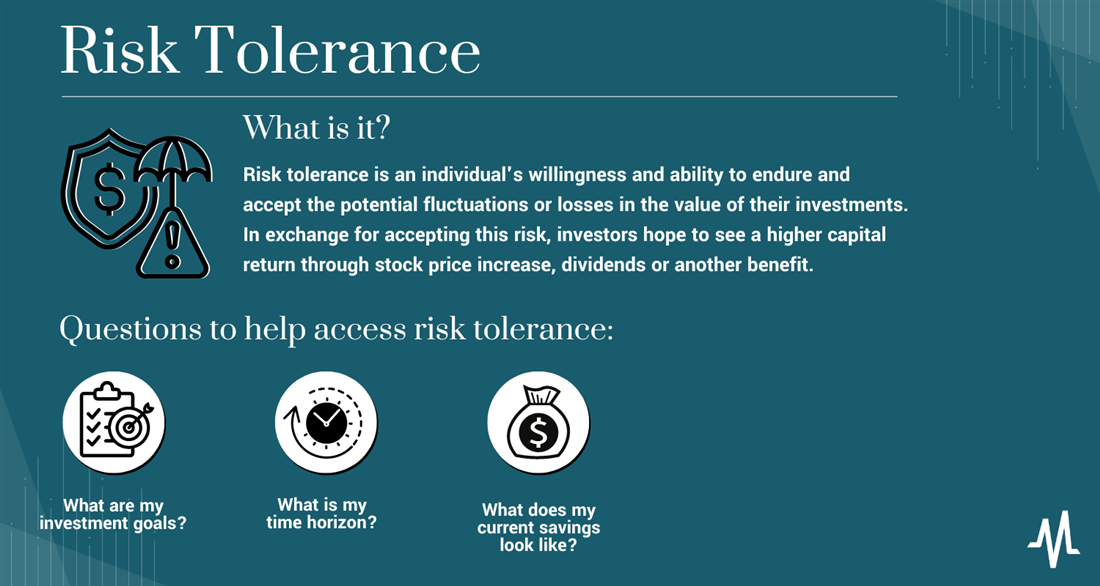

What is Risk Tolerance?

Before determining your unique risk tolerance, understand the general risk tolerance definition. Risk tolerance refers to an individual's willingness and ability to endure and accept the potential fluctuations or losses in the value of their investments. In exchange for accepting this risk, investors hope to see a higher capital return through stock price increase, dividends or another benefit.

Determining risk tolerance is essential in investing for the future because the volatility you can withstand will vary depending on your financial goals. Assets that show less volatility and retain their value better in periods of economic downturn do not show the same level of growth during periods of economic prosperity. Investing in assets like penny stocks may result in more volatility, but it can also enhance returns if the investment is successful.

For example, municipal bonds will retain value exceptionally well during recessions and depressions because the government backs them. However, bonds will be left behind during booming periods, leaving profit on the table for investors in the form of opportunity costs. Determine risk tolerance before dividing your investment funds according to your value retention needs.

Understanding Different Types of Risk Tolerance

While there is no universal investment risk tolerance scale, we can examine a few general categories of investors. Most investors fall into one of the three categories when determining investing risk tolerance.

Aggressive Risk Tolerance

Investors with an aggressive risk tolerance are willing to take on a substantial investment risk in pursuit of higher potential returns. They typically have a long-term investment horizon and are comfortable with significant market volatility.

An example of an investor who could have an aggressive risk tolerance level is a young professional. Investors in their mid-20s will likely be investing for many years and thus able to handle a higher level of market volatility. Risk-tolerant investors may put more capital into volatile assets like growth-oriented stocks or investments in emerging markets.

Moderate Risk Tolerance

Most investors fall into the "moderate" risk tolerance category, looking to balance growth during bull markets and retain as much value as possible during bear markets. Moderate investors often have a medium- to long-term investment horizon and may allocate their portfolio across a mix of equities, bonds and other asset classes.

An example of an investor who may have a moderate risk tolerance is a worker in their 40s. While this investor will still likely be working for years before retirement, they may have other financial obligations (like a mortgage or a child's college education) that make market turbulence more challenging to withstand. These investors may use a retirement account like an IRA to invest heavily in diversified mutual funds or ETFs.

Conservative Risk Tolerance

If you're approaching retirement, you may not be able to handle as much volatility as in the past. Investors with a conservative risk tolerance prioritize capital preservation and stability over higher potential returns. Conservative investors often have a short- to medium-term investment horizon and may allocate a significant portion of their portfolio to fixed-income securities, cash and less volatile assets.

An example of an investor who could take a conservative risk tolerance when building their portfolio is a senior in their early 60s. As these investors near the end of their careers, they will want to begin cashing out their investments, so growth is less of a concern. Their portfolio may have a higher concentration of bonds and other backed assets with insurance or guarantees to protect value.

How to Determine Your Risk Tolerance

Learning how to measure risk tolerance starts with an examination of your personal financial goals and investing timeline. Take the following steps to determine your unique risk tolerance.

Step 1: Learn about the major asset types.

If you're a new investor, you might need to become more familiar with the multiple types of assets available. Stocks, bonds, ETFs and mutual funds are all investment vehicles with different levels of volatility, with each asset suitable for a different type of investor.

MarketBeat's financial terms dictionary is an excellent resource for learning about common investment options.

Image: MarketBeat offers a free financial terms dictionary with more than 200 in-depth definitions.

Image: MarketBeat offers a free financial terms dictionary with more than 200 in-depth definitions.

Step 2: Consider your investment preferences.

Your investment preferences will play a significant role in the level of risk tolerance you'll need to accept. If your investing goal is to earn active income through trading, you'll likely need to invest in highly volatile assets to see a worthwhile potential return. On the other hand, if you're a long-term investor with an eye toward long-term retirement, you can achieve your financial goals without taking on more risk.

Risk tolerance is about more than calculating return — you'll also want to consider your personal feelings and psychology when choosing an asset mix. If you have multiple investment portfolios already, you may be more successful in taking risks because you aren't jeopardizing your financial future when executing your trading strategy. Consider investment preferences, including how active a role you want to take in your portfolio management, when determining risk tolerance.

Step 3: Create a list of financial goals and timelines.

Financial goals provide a clear time frame for investors to achieve specific objectives. Longer-term goals, such as retirement planning or funding a child's education, allow for a longer investment horizon. Investors with longer time horizons may have a greater capacity to tolerate short-term volatility and take on higher levels of investment risk to pursue higher returns.

On the other hand, shorter-term goals, like purchasing a house in the next few years, necessitate a more conservative investment approach to preserve capital and ensure funds are available when needed. Create a list of financial goals and your timeline for each goal to determine the type of investments you can use to achieve them.

3 Questions to Help Assess Risk Tolerance

After learning more about the market, it's time to take a closer look at your finances and investing timeline to refine risk. Be sure to ask yourself these three questions before creating your asset mix.

What Are My Investment Goals?

Your investing goals are one of the first things to consider when defining your risk tolerance. Whether the goal is retirement, buying a home or funding a child's eventual education, having a well-defined goal allows investors to align their risk tolerance with the desired outcomes.

Investment goals inherently involve a tradeoff between risk and potential reward. By defining your investment goals, you can evaluate your level of financial returns needed to achieve those goals. This assessment helps determine the amount of risk an investor may need to assume. If the potential risk seems too high for the desired return, you might need to reassess goals, adjust your time horizon or reconsider your risk tolerance.

What is My Time Horizon?

The amount of time you anticipate holding your investment will also play a role in your ideal risk tolerance. A longer time horizon generally allows for higher risk tolerance. You can ride out short-term market volatility with a longer timeframe and recover from any temporary losses. This increased tolerance for risk opens up opportunities for potentially higher returns through investments that carry more volatility, such as stocks or growth-oriented assets.

Conversely, a shorter time horizon often necessitates a more conservative approach. If your goals are approaching soon, capital preservation becomes more important to ensure your funds are available when needed. A conservative approach focuses on protecting the principal and may involve allocating a larger portion of your portfolio to more stable investments like bonds or cash equivalents.

What Does My Current Savings Look Like?

Your current savings and investment plan will also majorly determine where you may want to consider putting your capital. Higher savings provide a greater buffer against potential investment losses and financial setbacks. If you have substantial savings, you may have a higher risk tolerance because you have the financial resources to absorb short-term fluctuations in your investment portfolio without compromising your immediate financial needs or goals.

On the other hand, if your current savings are limited, you may have a lower risk tolerance. With limited savings, the preservation of capital becomes more important, as any significant investment losses could substantially impact your financial stability and ability to meet your basic household needs.

How to Translate Risk Tolerance into an Investment Strategy

Once you know how much risk you're prepared to tolerate as an investor, you can use this information to create an investment strategy. Assets like stocks, bonds and ETFs all require investors to take on varying levels of risk in return for varying reward potential. Additionally, individual stocks and ETFs are considered safer than others, with blue-chip options retaining value better in times of volatility.

Asset Allocation for Risk Tolerance

The most straightforward way to account for risk tolerance is to divide your investment capital between multiple categories of assets strategically. The three major assets most investors hold in their portfolios are stocks (shares of ownership in individual companies), bonds (a type of debt security issued by companies and government) and cash (fiat currency). ETFs, mutual funds and other investment vehicles are primarily made up of these three major assets.

Stocks tend to have a higher risk and reward potential than bonds, which are riskier than holding cash. Diversifying your assets and adjusting your allocation over time will help you mitigate the inherent risks of participating in the stock market.

The following is a sample allocation you might use when constructing a portfolio:

| |

Aggressive portfolio

|

Moderate portfolio

|

Conservative portfolio

|

|

Stocks

|

80% to 90%

|

70% to 80%

|

40% to 50%

|

|

Bonds

|

10% to 20%

|

20% to 30%

|

40% to 60%

|

|

Cash

|

0% to 10%

|

10% to 20%

|

10% to 20%

|

Changing Risk Tolerance and Asset Allocation

Risk tolerance is a dynamic characteristic, meaning your risk tolerance will likely change over time. If managing risk tolerance over the years sounds too complicated, know that many investment brokerages have created unique solutions to take management off the shoulders of individual investors.

For example, the Vanguard Target Retirement 2050 Fund (NYSE: VFIFX) is an actively managed mutual fund aimed at investors who want to retire in the year 2050. Fund managers adjust the fund's asset allocation depending on how close investors in the fund are to retirement. Solutions like these can make managing the road to retirement easier for new investors.

FAQs

The following are a few last-minute answers to questions about determining risk tolerance.

How do you measure investment risk tolerance?

You can measure risk tolerance by considering your investment timeline and your goals. For example, if you want to save money for a discretionary purchase in a taxable brokerage account and have another account with retirement funds, you could invest in more volatile assets. However, if you're investing through a retirement account like a 401(k), you may want to choose more conservative assets.

How do you know your risk tolerance?

You can learn your investing risk tolerance by examining your current investment holdings and goals. You may be more risk tolerant if you have many years before retirement or have a fully fleshed-out investment portfolio. If you're nearing retirement, you may be more risk-averse and prefer investing in less volatile assets like bonds.

How can a financial planner determine the investment risk tolerance of an investor?

A financial planner can help determine risk tolerance using both quantitative methods (like risk tolerance questionnaires) and personal financial investigation. Financial planners are market professionals that take your income, financial goals and other personal details into account to create an ideal asset mix for your level of investment risk tolerance.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

If a company's CEO, COO, and CFO were all selling shares of their stock, would you want to know?

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.