The Invesco VRDO Tax-Free ETF holdings spread out the risk associated with any particular bond or issuer. Directly investing in individual bonds carries higher risks since one bad decision could result in some degree of loss due to default. Investing through a fund helps mitigate this potential issue. Municipal bond funds also allow for lower minimums than purchasing individual bonds; however, for funds like PVI, fund fees come into play, so consider these when selecting your investments.

Common Terms Related to Bonds

Bonds of all types have a common language. Take a look at some common terms you may want to familiarize yourself with before purchasing municipal bonds:

- Face value (also called par value): This is the amount of money the bond will be worth at maturity. The face value also sets the value that establishes the base for interest or coupon payments.

- Coupon rate: This is the interest rate the bond issuer pays to the bondholder. The coupon rate is based on the face value of the bond, expressed as a percentage. If interest rates rise before the bond matures, the coupon rate remains the same as when the bond is purchased. If a $1,000 bond offers a 5% coupon rate, every bondholder will receive $50 coupon payments regardless of the price they paid for the bond.

- Coupon dates: These dates let the bondholder know when the issuer will make interest (or coupon) payments, usually annually or semi-annually.

- Maturity date: The maturity date is when the bond is said to mature. The issuer pays the bond owner the bond's face value.

- Issue price: The issue price is the original market price the bond is sold for. If the bond sells above its face value, the "issue" is said to be selling at a premium. If the bond sells below its face value, the "issue" is said to be selling at a discount.

How is a Bond's Interest Rate Determined?

So how much do municipal bonds pay? Two factors set the interest rate of a bond. The first is the bond issuer's credit rating, which you may be familiar with if you've ever sought a bank loan. Just like a corporation, government entities have credit ratings.

Those with a poor credit rating will have bonds that trade at a discount since prospective buyers will assess the potential risk of the entity defaulting and the price they pay for holding the bond. Bond investing is about security. If a municipal bond has a yield that seems too good to be true, it may indicate an underlying problem.

The other factor determining a bond's interest rate is the maturity length. Generally, the longer a bond issuer asks you to hold it before maturity, the more it will dictate a higher interest rate. However, this reflects normal market conditions with a yield curve that shows long-term rates as higher than short-term rates. Investors may see higher interest rates on short-term bonds when the yield curve flattens or inverts.

Example of Investing in a Municipal Bond

Investing in a municipal bond is similar to investing in any other debt instrument, including a treasury bond. The primary difference between the two is that municipal bonds usually have the backing of local or state governments and may come with certain tax breaks or other benefits.

One example of investing in a municipal bond is the Washington State Public Works Board (below) 30-year zero coupon bond. This bond was issued in 2018 with an initial face value of $10,000. The coupon rate for this bond is 0%, meaning you will receive no interest payments until maturity. Instead, you'll receive the full face value at the maturity date, plus accumulated interest for each year held.

The main benefit of this type of zero-coupon bond is that it provides a safe and secure investment option with minimal risk since it has the backing of the government agency. You also get tax incentives for buying it, including an exemption from federal taxes on part or all of your income.

When investing in a municipal bond like the Washington State Public Works Board 30-year zero coupon bond, remember that you'll receive your return only when it matures. You cannot sell it before maturity unless both parties agree on a sale price. Additionally, inflation can reduce its buying power over time, so consider inflation risk when determining how much to invest in these bonds.

How to Invest in a Municipal Bond

Municipal bonds can be one of the safest investments because of the full faith and credit of the issuing government backing them. Still, take a few steps when researching and investing in municipal bonds to make sure you're making an informed decision.

Step 1: Determine your investment needs.

Deciding which level of risk you can handle will help you decide what type of municipal bond you should invest in. Think about whether you're investing for steady income or capital gains. If you're looking for steady income, opt for one with an attractive coupon rate.

Step 2: Research bonds and their issuers.

Compare them to determine which one is best suited for your investment needs. Look at their financials and ensure they have a good standing with credit rating agencies such as Moody's or S&P Global Ratings.

The bond issuer's credit rating plays a huge role in determining the bond's interest rate. Always aim for bonds issued by entities with high credit ratings to minimize risk.

Step 4: Compare yields.

Compare different yields offered by different issuers and look for any call features that may increase or decrease their value over time. Also, find out if any penalties are associated with early redemption of the bond before it matures.

Step 4: Read all documents.

When investing in a municipal bond, read all disclosure documents carefully before signing any contracts or agreements. Doing so will help ensure you understand all the terms associated with your investment.

Step 5: Look into tax benefits.

Municipal bonds often come with tax benefits, such as exemption from federal taxes on part or all of your income from the bond. Make sure to research and consider these benefits when determining the overall return on your investment.

Pros and Cons of Investing in Municipal Bonds

Municipal bonds offer numerous benefits to you as an investor.

Pros

The benefits include:

- Tax-exempt status: Interest earned from municipal bonds is exempt from federal taxes and, in some cases, state taxes. The tax-exempt status makes them an attractive option for high-income earners who want to reduce their tax burden.

- Low risk: Government entities issue muni bonds, which have the power to levy taxes to repay bondholders. If you're looking for reliable income streams, municipal bonds can provide a low-risk investment opportunity.

- Diversification: Municipal bonds also offer diversification benefits because they are not directly connected to other markets like stocks or corporate bonds.

- Steady income: With regular interest payments, municipal bonds can provide a steady income stream.

Cons

In general, muni bonds are considered a safe investment, but they have drawbacks:

- Interest rate risk: When interest rates rise, bond prices fall. Since bond prices are inversely related to interest rates, a rise in rates causes the present value of future cash flows to decrease, causing bond prices to fall. You may lose money if you must sell your bond before it matures.

- Credit risk: Even though local or state governments back these bonds, there's still a chance that the issuer could default on its payments. It is known as credit risk, so you should research the issuer's financials and credit rating before investing in their bond.

- Liquidity risk: Municipal bonds are less easily tradable than other types of securities, which means there may be a lack of buyers or sellers when you need to sell your bond. This could cause you to receive less than what you originally invested.

- Inflation risk: If inflation rises, you may receive less return when your bond matures than you originally invested.

- Low returns: Muni bonds often carry lower interest rates than other investments, like stocks. If you're looking for higher returns, you may have better choices than muni bonds.

- High fees: Municipal bond funds charge fees and commissions, which can further reduce your potential return on investment.

Muni Bonds: A Safer, Tax-Friendly Option

Municipal bonds can be an excellent investment if you're looking for a low-risk, tax-advantaged option. They offer steady income and diversification benefits but come with some drawbacks and risks, though they may not provide the highest returns. Ultimately, research before investing in municipal bonds to ensure you'll get the best possible returns.

FAQs

You now know the ins and outs of municipal bonds and their many advantages, but you might still have a few questions remaining. We tackle some below.

What is the downside of municipal bonds?

The downside of municipal bonds is that they can carry lower interest rates than other investments, such as stocks, and may have higher fees or commissions. They also come with some risks, such as interest rate risk and credit risk. They can also suffer from low liquidity and inflation. Additionally, municipal bonds may not be able to provide the same level of returns as other investments.

How do you make money off municipal bonds?

The most common way to make money from tax-free municipal bonds is by investing in them directly. When you buy a bond, you essentially lend money to the issuer in exchange for an agreement to pay back the principal plus interest by a certain date. The better the issuer's creditworthiness, the higher the return on your investment will be. You can also explore strategies to get even more out of your municipal bond investments by using bond ladders — purchasing several different bonds that have staggered maturity dates — or another municipal bond strategy to increase your returns.

What is a municipal bond in simple terms?

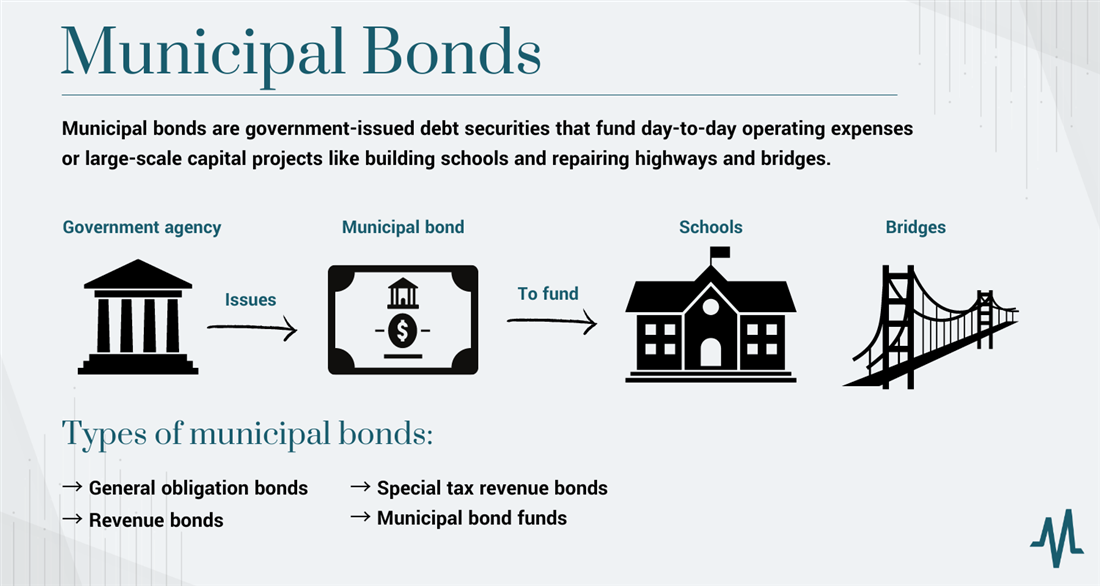

A municipal bond is a debt security issued by a government or public body at the municipal level. When you purchase a municipal bond, you effectively loan money to the issuer in exchange for a promise of repayment with interest at predetermined intervals. These bonds are generally very safe investments, and the interest paid is usually exempt from federal taxes. You can use the funds from the sale of the bonds to finance public works projects such as roads, bridges, schools and hospitals.