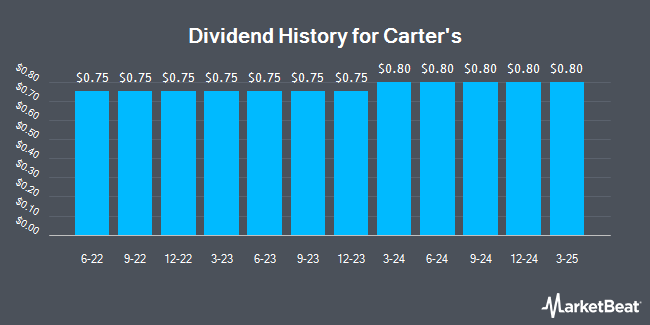

Carter's, Inc. (NYSE:CRI - Get Free Report) declared a quarterly dividend on Friday, February 21st, Wall Street Journal reports. Shareholders of record on Monday, March 10th will be given a dividend of 0.80 per share by the textile maker on Friday, March 28th. This represents a $3.20 dividend on an annualized basis and a yield of 7.75%. The ex-dividend date of this dividend is Monday, March 10th.

Carter's has raised its dividend by an average of 31.7% annually over the last three years. Carter's has a payout ratio of 80.2% indicating that its dividend is currently covered by earnings, but may not be in the future if the company's earnings decline. Equities analysts expect Carter's to earn $4.77 per share next year, which means the company should continue to be able to cover its $3.20 annual dividend with an expected future payout ratio of 67.1%.

Carter's Stock Performance

CRI stock traded down $0.85 during trading hours on Friday, reaching $41.30. The stock had a trading volume of 1,682,648 shares, compared to its average volume of 1,127,734. The company has a debt-to-equity ratio of 0.60, a current ratio of 2.21 and a quick ratio of 0.96. The stock has a 50-day simple moving average of $52.30 and a 200 day simple moving average of $57.93. The stock has a market capitalization of $1.49 billion, a PE ratio of 6.56, a price-to-earnings-growth ratio of 3.37 and a beta of 1.21. Carter's has a fifty-two week low of $40.76 and a fifty-two week high of $88.03.

Carter's (NYSE:CRI - Get Free Report) last announced its quarterly earnings results on Tuesday, February 25th. The textile maker reported $2.39 earnings per share for the quarter, topping analysts' consensus estimates of $1.87 by $0.52. Carter's had a return on equity of 27.15% and a net margin of 8.11%. The firm had revenue of $859.70 million for the quarter, compared to the consensus estimate of $835.82 million. During the same quarter in the previous year, the business earned $2.76 earnings per share. The business's revenue was up .2% compared to the same quarter last year. Analysts predict that Carter's will post 5.15 EPS for the current fiscal year.

Analyst Ratings Changes

A number of research firms have commented on CRI. Wells Fargo & Company reduced their price objective on shares of Carter's from $65.00 to $48.00 and set an "equal weight" rating for the company in a research report on Wednesday. Citigroup cut their price objective on shares of Carter's from $50.00 to $45.00 and set a "neutral" rating for the company in a research report on Wednesday. Finally, UBS Group decreased their target price on Carter's from $57.00 to $49.00 and set a "neutral" rating on the stock in a research report on Wednesday. One equities research analyst has rated the stock with a sell rating and four have assigned a hold rating to the company. According to data from MarketBeat, Carter's presently has an average rating of "Hold" and a consensus price target of $49.00.

Check Out Our Latest Report on CRI

About Carter's

(

Get Free Report)

Carter's, Inc engages in the business of brand marketing of young children's apparel. It operates through the following segments: the United States (US) Retail, US Wholesale, and International. The US Retail segment includes selling products through retail stores and ecommerce websites. The US Wholesale segment focuses on wholesale partners.

Recommended Stories

Before you consider Carter's, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Carter's wasn't on the list.

While Carter's currently has a Reduce rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Discover the 10 Best High-Yield Dividend Stocks for 2025 and secure reliable income in uncertain markets. Download the report now to identify top dividend payers and avoid common yield traps.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.