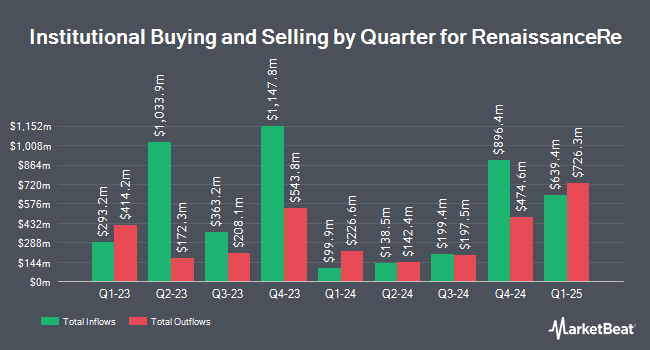

Earnest Partners LLC trimmed its holdings in shares of RenaissanceRe Holdings Ltd. (NYSE:RNR - Free Report) by 2.7% in the fourth quarter, according to its most recent Form 13F filing with the SEC. The institutional investor owned 578,702 shares of the insurance provider's stock after selling 16,057 shares during the period. Earnest Partners LLC owned about 1.11% of RenaissanceRe worth $143,987,000 as of its most recent SEC filing.

A number of other large investors have also recently added to or reduced their stakes in RNR. Barclays PLC boosted its stake in RenaissanceRe by 57.1% in the 3rd quarter. Barclays PLC now owns 22,923 shares of the insurance provider's stock worth $6,244,000 after purchasing an additional 8,333 shares during the period. World Investment Advisors LLC acquired a new position in RenaissanceRe in the 3rd quarter worth approximately $16,176,000. Wilmington Savings Fund Society FSB acquired a new position in RenaissanceRe in the 3rd quarter worth approximately $405,000. Tidal Investments LLC boosted its stake in RenaissanceRe by 2.6% in the 3rd quarter. Tidal Investments LLC now owns 9,236 shares of the insurance provider's stock worth $2,516,000 after purchasing an additional 232 shares during the period. Finally, GAMMA Investing LLC boosted its stake in RenaissanceRe by 22.9% in the 4th quarter. GAMMA Investing LLC now owns 1,179 shares of the insurance provider's stock worth $293,000 after purchasing an additional 220 shares during the period. 99.97% of the stock is currently owned by institutional investors.

RenaissanceRe Stock Performance

NYSE:RNR traded up $3.93 during mid-day trading on Tuesday, hitting $241.82. 517,730 shares of the company's stock traded hands, compared to its average volume of 428,541. The firm has a 50 day moving average of $238.07 and a two-hundred day moving average of $251.67. RenaissanceRe Holdings Ltd. has a 12 month low of $208.98 and a 12 month high of $300.00. The firm has a market capitalization of $11.85 billion, a price-to-earnings ratio of 6.91, a price-to-earnings-growth ratio of 2.09 and a beta of 0.29. The company has a current ratio of 1.42, a quick ratio of 1.42 and a debt-to-equity ratio of 0.19.

RenaissanceRe (NYSE:RNR - Get Free Report) last announced its earnings results on Wednesday, April 23rd. The insurance provider reported ($1.49) earnings per share for the quarter, missing the consensus estimate of ($0.32) by ($1.17). RenaissanceRe had a net margin of 15.99% and a return on equity of 23.41%. The business had revenue of $3.44 billion for the quarter, compared to the consensus estimate of $3.36 billion. During the same quarter in the previous year, the company earned $12.18 EPS. RenaissanceRe's revenue for the quarter was up 7.6% compared to the same quarter last year. On average, equities analysts forecast that RenaissanceRe Holdings Ltd. will post 26.04 earnings per share for the current fiscal year.

RenaissanceRe Increases Dividend

The firm also recently announced a quarterly dividend, which was paid on Monday, March 31st. Investors of record on Friday, March 14th were paid a dividend of $0.40 per share. This is an increase from RenaissanceRe's previous quarterly dividend of $0.39. The ex-dividend date of this dividend was Friday, March 14th. This represents a $1.60 annualized dividend and a yield of 0.66%. RenaissanceRe's dividend payout ratio is presently 5.10%.

Wall Street Analysts Forecast Growth

A number of equities analysts recently commented on RNR shares. Wells Fargo & Company decreased their price objective on shares of RenaissanceRe from $277.00 to $271.00 and set an "overweight" rating for the company in a research note on Thursday, April 10th. Jefferies Financial Group dropped their target price on RenaissanceRe from $266.00 to $265.00 and set a "hold" rating on the stock in a research report on Friday, April 11th. Morgan Stanley raised RenaissanceRe from an "equal weight" rating to an "overweight" rating and upped their target price for the stock from $235.00 to $275.00 in a research report on Friday. JMP Securities reaffirmed a "market perform" rating on shares of RenaissanceRe in a research report on Thursday, April 24th. Finally, Keefe, Bruyette & Woods upped their target price on RenaissanceRe from $279.00 to $282.00 and gave the stock an "outperform" rating in a research report on Tuesday. Two investment analysts have rated the stock with a sell rating, four have given a hold rating and six have assigned a buy rating to the company's stock. Based on data from MarketBeat, the stock presently has a consensus rating of "Hold" and an average price target of $282.60.

Read Our Latest Stock Analysis on RenaissanceRe

About RenaissanceRe

(

Free Report)

RenaissanceRe Holdings Ltd., together with its subsidiaries, provides reinsurance and insurance products in the United States and internationally. The company operates through Property, and Casualty and Specialty segments. The Property segment writes property catastrophe excess of loss reinsurance and excess of loss reinsurance to insure insurance and reinsurance companies against natural and man-made catastrophes, including hurricanes, earthquakes, typhoons, and tsunamis, as well as winter storms, freezes, floods, fires, windstorms, tornadoes, explosions, and acts of terrorism; and other property class of products, such as proportional reinsurance, property per risk, property reinsurance, binding facilities, and regional U.S.

Read More

Before you consider RenaissanceRe, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and RenaissanceRe wasn't on the list.

While RenaissanceRe currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Discover the 10 Best High-Yield Dividend Stocks for 2025 and secure reliable income in uncertain markets. Download the report now to identify top dividend payers and avoid common yield traps.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.