As uncertainty around the regional banking industry continues to proliferate, an opportunity arises. In times of increased market stress, correlations tend towards 1, opening the potential to buy some of the highest quality regional banks in the United States for a steep discount.

Bank of Hawaii NYSE: BOH and Cullen Frost Bankers NYSE: CFR are rock-solid banks that have declined 28% and 22% since the beginning of March, respectively. In this article, we'll review the opportunity these two stocks pose and how exposed they are to the new areas of risk that regional banks face.

The Biggest Regional Bank Risks Right Now

The rapid rise in interest rates from near-zero to over 4.5% in a year created massive losses for any bank that bought US treasuries in the last ten years. To note, bond prices drop when yields rise.

Massive bond portfolio losses, coupled with significant uninsured deposit exposure, led to the failure of Silicon Valley Bank and Signature Bank. The mismatch between the assets and liabilities of these banks led their startup-concentrated deposit base to withdraw their money in fear of failure quickly.

As a result, the market closely scrutinizes the stickiness of deposits and the health of every bank's bond portfolio. The uncertainty led to a 27% decline in the SPDR S&P Regional Banking ETF NYSE: KRE since the start of March.

Regardless of their liquidity, regional banks nationwide are seeing deposit outflows pile up as depositors seek the safety of money market funds and large money center banks like JPMorgan NYSE: JPM.

But this crisis creates an opportunity to buy high-quality banks at a significant discount to historical average valuations.

Let’s take a look at two such opportunities.

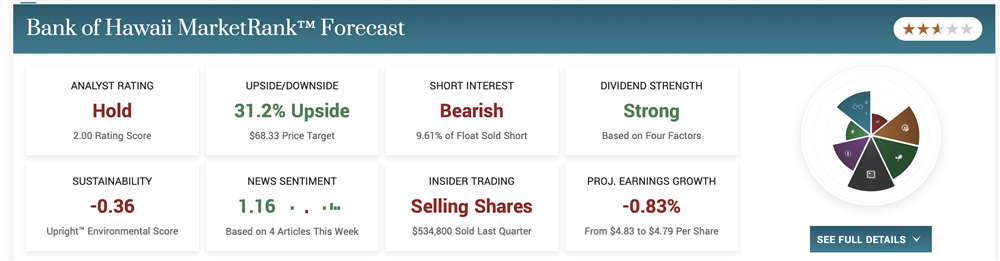

Bank of Hawaii (BOH)

The Bank of Hawaii is the second-largest bank in Hawaii, accounting for 33% of the island's total deposits. The bank is a hedge fund favorite and is seen as one of the higher-quality regional banks in the US.

It has achieved a consistent return on equity of about 15% for the past ten years, well above the industry average of 9-10%. And in a time when customers are worrying about the creditworthiness of their banks rather than the inverse, the bank is rated Aa3 by Moody's for long-term deposits, the highest rating in the US and Hawaii.

Despite BOH's reputation as a high-quality regional bank, the stock is down 31% since the start of March, dropping more than the regional bank index. And this is primarily because the bank has significant unrealized losses in its securities portfolio, one of the issues that led to Silicon Valley Bank's demise.

As we know, unrealized losses on hold-to-maturity (HTM) securities aren’t reflected in the income statement. In this way, tangible equity, the preferred method of measuring a bank’s value, can misrepresent value. But there’s a reason HTM securities aren’t ordinarily marked to market: because banks don’t intend to sell them and receive face value at maturity.

So a problem only arises if a bank is forced to sell these securities for some reason and realize a loss like Silicon Valley Bank did.

The primary question to ask when analyzing a post-SVB bank with significant HTM losses is if they have the liquidity to hold these securities to maturity.

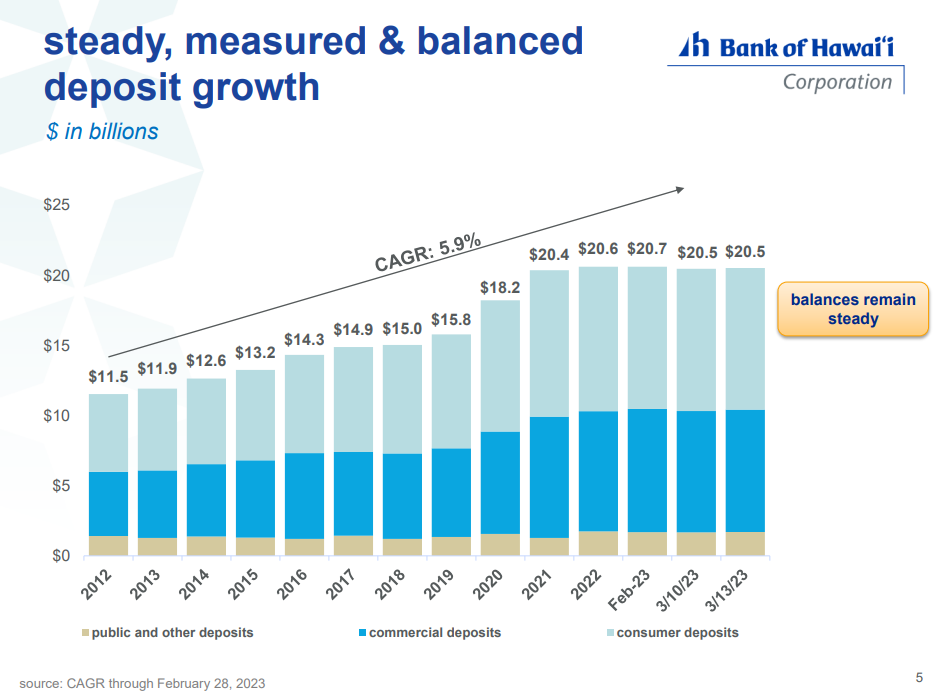

Bank of Hawaii has high-quality, sticky deposits, with 92% concentrated in Hawaii. The best evidence of this is BOH’s recent investor presentation, which has data up to March 13, three days following the failure of SVB, which should show how much its depositors reacted to anxiety in the banking sector.

As you can see from the chart below, the bank lost just $200 million in deposits following the events of SVB, accounting for less than 1% of its total deposits.

Compare this to First Republic Bank, which had to arrange emergency capital infusions from big banks and borrow tens of billions of dollars from the Federal Reserve at an overnight rate of 4.75%.

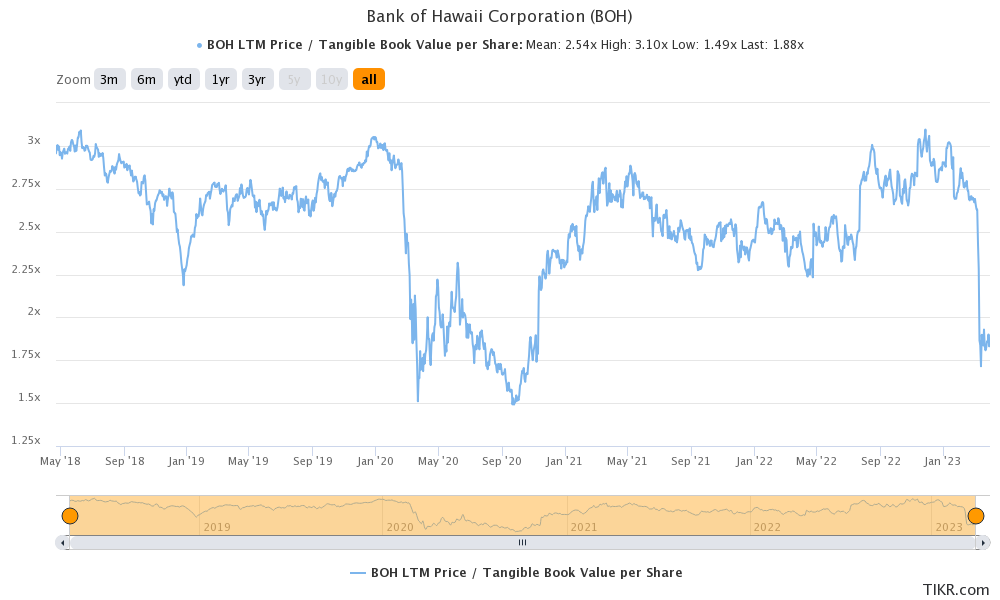

The stock is trading at the low end of its historical valuation range, at 1.8x tangible book value, which isn't far from its COVID lows. The stock tends to trade closer to a 2.5x multiple.

Cullen Frost Bankers (CFR)

Cullen Frost Bankers NYSE: CFR owns Frost Bank, a Texas-based bank with a storied history. The bank was the only large Texas bank to survive without bailouts or mergers after the Texas banking crisis in the 1980s. It also didn’t accept TARP money following the Great Financial Crisis in 2008.

Suffice it to say that Frost Bank has a very conservative culture, allowing it to survive for 155 years running.

Owing to its risk-averse nature, the bank has consistently achieved roughly 10% return on equity over the last decade, compared to Bank of Hawaii's 15%. The lower returns aren't a result of writing bad loans but simply writing fewer loans than the rest of the industry, as its loan-to-assets ratio is just 33%, whereas Bank of Hawaii's is 54%.

Frost is a dividend aristocrat, hiking its dividend for 29 consecutive years, even during the financial crisis. The stock currently yields a healthy 3.3%.

The bank hasn't published any press releases about how its deposits have changed post-SVB, so we can't tell if they've had significant outflows. However, even if the bank were to see substantial outflows, it's one of the most liquid banks in the industry. If Frost were to fail due to a bank run, the banking sector would have far deeper problems than the SVBs of the world.

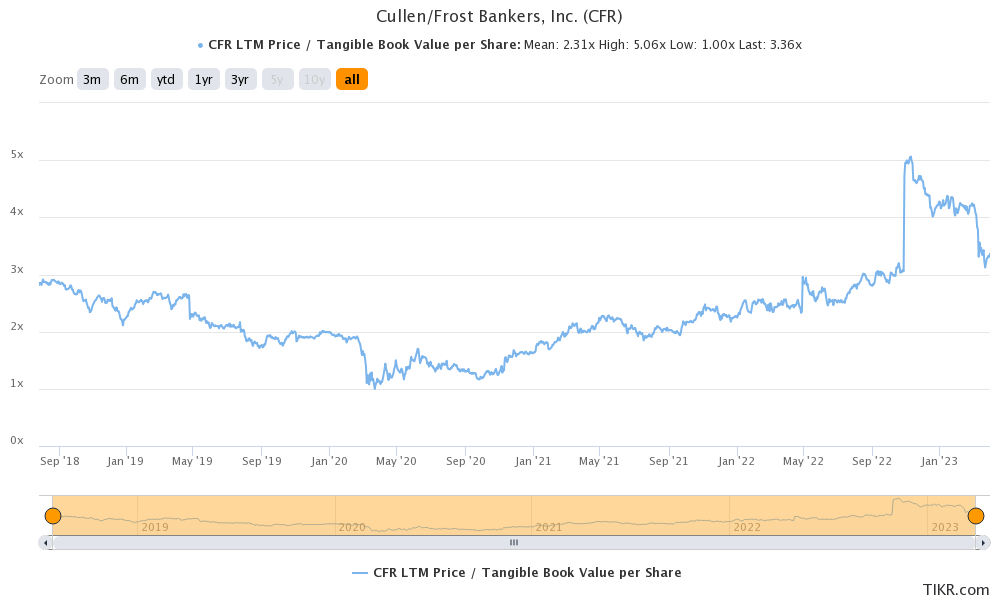

The stock is down 20% since the beginning of March, meaning its valuation multiple has compressed a bit, albeit not as dramatically as other regional banks. The stock trades richly at 3.3x tangible book, but on a relative basis, it's quite a bit lower than its peak multiple of 5x at the end of 2022.

Bottom Line

Looking forward, the upcoming barrage of bank earnings reports in the second half of April is one of the biggest catalysts for the sector in years. The reports will clarify the biggest winners and losers when it comes to deposit outflows and inflows.

Before you consider Cullen/Frost Bankers, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Cullen/Frost Bankers wasn't on the list.

While Cullen/Frost Bankers currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Robotics and automation are rapidly becoming essential infrastructure across healthcare, manufacturing, logistics, and many other industries.

"Physical AI" is coming to the United States, and there are four ways that investors can gain exposure to this new robotics revolution. Plus, learn which seven companies are most positioned to benefit as intelligent robots enter the workforce.

Get This Free Report