Netflix Today

$909.05 +7.01 (+0.78%) (As of 12/20/2024 05:45 PM ET)

- 52-Week Range

- $461.86

▼

$941.75 - P/E Ratio

- 51.45

- Price Target

- $807.70

Netflix Inc. NASDAQ: NFLX is the world's largest subscription-based streaming video service, boasting more than 280 million global subscribers. The company added 8 million net new subscribers in its second quarter of 2024 while increasing average revenue per user (ARPU) by 5%. The company’s market capitalization is hovering around the $300 million mark. With nearly everyone connected to a Netflix account somehow, the question arises whether the consumer discretionary sector giant can continue to grow. Here are four growth drivers that can help pave the way for Netflix to reach its first trillion-dollar market cap.

1) International Subscriber Growth

The United States and Canada are saturated with over 84 million subscribers. Assuming each subscriber enables two people in their household to access the service, that’s over 168 million users out of a combined 375 million people in the U.S. and Canada. With over eight billion people in the world, there’s more growth to be had internationally. The company is trying to reach untapped markets in Asia and Africa. The ARPU in the United States and Canada was $17.71 up 7% YoY. In the EMEA, ARPU sank 1% YoY to $10.80. In Latin America, ARPU fell 3% YoY to $8.28. Asia Pacific saw ARPU fall 6% YoY to $7.17.

Much More Room to Grow Internationally

Netflix had 94 million subscribers in the Europe, Middle East and Africa (EMEA) region. Latin America ended Q2 2024 with 49.2 million subscribers. Asia Pacific had 50.3 million subscribers. Netflix's business is surprisingly seasonal, as new TV and streaming device purchases result in an uptick in membership. Historically, the fourth quarter has its "greatest streaming membership growth." It's worth noting that its cost of revenues fell to 54% of total revenue, down from 57% in the year-ago period.

2) Advertising

Ad-supported programming has unlocked Netflix's growth in terms of growing its audience and adding a source of revenue beyond the core subscription model. Ad-supported tiers are a gateway to the Netflix universe. It has also allowed Netflix to offer their services as part of bundles with competitors like Comcast Co. NASDAQ: CMCSA owned Peacock, Warner Bros. Discovery Inc. NASDAQ: WBD Max and The Walt Disney Co. NYSE: DIS Disney+ and Hulu. This enables Netflix to poach subscribers on its competitor streaming services. Netflix has seen a 150% increase in upfront ad sales commitments in 2024.

Its global ad-supported tier membership has climbed to over 40 million subscribers. Netflix has seen 45% of new sign-ups join through its ad-supported tiers where it’s available. Its lowest-priced subscription tier is the Standard with Ads, which is $6.99 per month. They are limited to 15 downloads and simultaneous streaming on two devices. Ad-supported tiers also provide the potential for conversion to ad-free premium memberships. ARPU for ad-supported tier members generally equals premium tier members, as ad revenues make up the difference.

AdTech Platform is Being Built

Netflix enables private 1:1 marketplace deals through various adtech platforms, including The Trade Desk Inc. NASDAQ: TTD, Alphabet Inc. NASDAQ: GOOGL, Google's Display & Video 360, and Microsoft Co. NASDAQ: MSFT. The company plans to launch its adtech platform by the end of 2025.

Netflix’s Strategy: Boosting Revenue with Free Ad-Supported Tiers

Ad-supported tiers are still in the rollout stage. Advertising commitments are a steadier and more predictable form of revenue than monthly memberships. There is speculation that Netflix may be planning to introduce free ad-supported tiers in parts of Asia and Europe. This will surge viewership and provide more eyeballs for advertisers, driving up membership and advertising revenues. Currently, there is no trial or free tier membership plan for Netflix.

3) Margin Expansion

Netflix has been expanding its margins solidly. In 2017, Netflix only generated a 7% operating margin, which improved to 27.2% in Q2 2024. The company has $4.8 billion available on its stock buyback plan. Thinning out the outstanding shares can improve its EPS and accelerate its market cap when the stock rises.

Fixed-Cost Content Licensing Model

Netflix has been able to expand margins with its fixed-cost licensing model. Netflix usually pays a rate that is comprised of the cost of production and a 30% premium, which is half what traditional TV licensing deals cost. They tend to cover production costs and a 60% to 70% premium.

Password sharing crackdowns, rising membership prices, and ad-support tiers have been instrumental in expanding Netflix’s margins.

4) Video Games

Netflix has been growing its offering of video games and interactive content for the past several years. The goal has been to enhance its core streaming service and increase subscriber engagement. The video-game element especially caters to mobile app users who can access it through a single Netflix app rather than downloading separate apps. Video games are a value-added service meant to help lower churn. Netflix is inching towards cloud gaming, which would allow for more complex games that are streamed directly to various devices. Netflix plans to develop games in-house to expand the brand and deepen audience engagement, creating cross-platform experiences. Of course, they would sell in-game advertising as well.

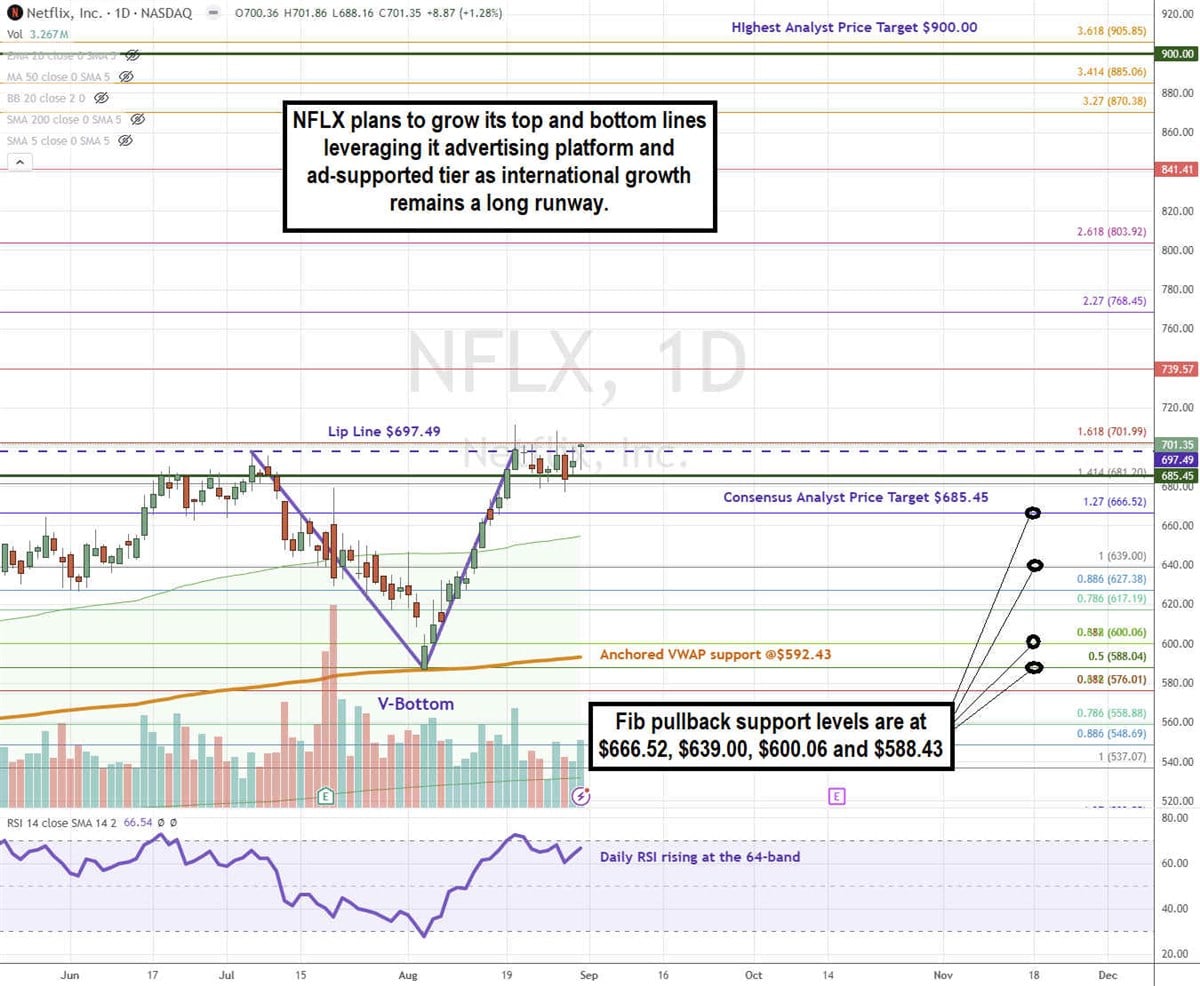

NFLX Stock Formed a V-Bottom Pattern

A V-bottom pattern is formed when a stock sells off sharply to a bottom and then rises sharply back to where it started selling off the lip line. The lip line either remains a double top or becomes a support after the stock breaks out.

NFLX formed a V-bottom lip line at $697.49 on July 5, 2024, before sinking to a swing low near the $588.04 Fibonacci (fib) support, which also overlapped with the anchored VWAP support. NFLX surged back up to retest the neckline, making higher highs for 11 consecutive trading days, peaking at $711.33 on Aug. 20, 2024. Shares have since fallen back under the lip line, chopping sideways as the daily RSI also chops around the 64-band. Fib pullback support levels are at $666.52, $630.00, $600.06, and $588.43.

Netflix’s average consensus price target is $685.45, and its highest analyst price target sits at $900.00. The daily anchored VWAP support sits at $592.43.

Actionable Options Strategies

Since NFLX is trading above the consensus analyst price target, looking for pullbacks is prudent. NFLX bulls can enter on pullbacks using cash-secured puts with trail stops under the $537.07 fib support. A wheel strategy can be implemented upon being assigned shares and writing covered calls to generate income.

Before you consider Netflix, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Netflix wasn't on the list.

While Netflix currently has a "Moderate Buy" rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Just getting into the stock market? These 10 simple stocks can help beginning investors build long-term wealth without knowing options, technicals, or other advanced strategies.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.