The Analysts Are Cautious, But Should You Be?

Kimberly-Clark (KMB) reported earnings earlier this week to little fanfare. The company reported stellar top and bottom-line results, driven by viral-induced demand, but gave an uncertain outlook for the year. The worst news is the company suspended the buyback plan for the remainder of the second quarter, a move that may foreshadow liquidity issues later in the year. The question now is, are the analysts right to be cautious or are new highs in store for this near-Dividend King.

“The company is temporarily suspending its share repurchase program effective April 24, 2020, for at least the remainder of the second quarter to enhance flexibility in the current environment. The company will continue to monitor the environment and further assess its share repurchase program later in the year."

The Results, The Results Speak For Themselves

Kimberly-Clark is a consumer products company with a primary focus on paper products. Products range from toilet paper to paper towels, personal care, and every need in-between. Thinking about the pandemic, the rush to pantry-load, and which products have been the least available (toilet paper and paper towels, etc) I’d have to say this company is well-positioned for today’s market.

Organic sales surged 11.7% in the first quarter to beat the analyst’s consensus. The strength is due in large part by volume sales, up 8%, with those results padded by higher pricing and product mix. Revenue in the top three product segments (personal care, consumer tissue, and K-C professional all showed growth over the prior year. Regarding margin, margins expanded 180 basis points due to operational efficiencies put in place to counter the impact of the pandemic.

Guidance for the year was pulled due to the virus but I am not concerned. As of this time, Kimberly-Clark is outperforming expectations and positioned to maintain its leadership position over the course of the crisis. If anything, based on Q1 results and the expected timeline for the pandemic, Kimberly-Clark’s current guidance is light. If the cure takes as long as the experts say and there is a second wave this fall (like the experts say) stay-at-home and social-distancing trends will support this company’s revenue growth long into the future.

A Cautious View From UBS And They Aren’t The Only Ones

Just a day after Kimberly-Clark released its Q1 results analysts at UBS came out with a note of caution. The analyst, Steven Strycula, sees product trends returning to normal as the pantry-load effect wears off. He also sees a number of factors impacting profitability but says the ultimate result is still unknown. Ironically, Mr. Strycula upped the price target while maintaining his sell-rating so take the warning with a grain of salt.

"With a greater % of the global population spending more time at home, we expect C-Tissue demand to remain above pre-COVID levels in FY20, but we assume personal care volume trends to normalize in the coming months once pantry load is depleted. We expect delays in restructuring project and sales demand to boost FY20 free cash flow. The key unknown is margin, specifically how commodity deflation tailwinds and product mix nets against FX risk and plant over time,"

The analyst’s community is, generally, neutral on this stock. Of the 16 analysts currently rating KMB, 7 rate the stock a hold but the bias is bullish. There are only 3 analysts with a bearish rating, the remainders are a buy or a strong buy. Notably, the consensus price target has been on the rise over the past month so the community has been warming up to the stock. At today’s prices, the consensus target leaves about 4.25% upside but doesn’t include the dividend or the technical outlook.

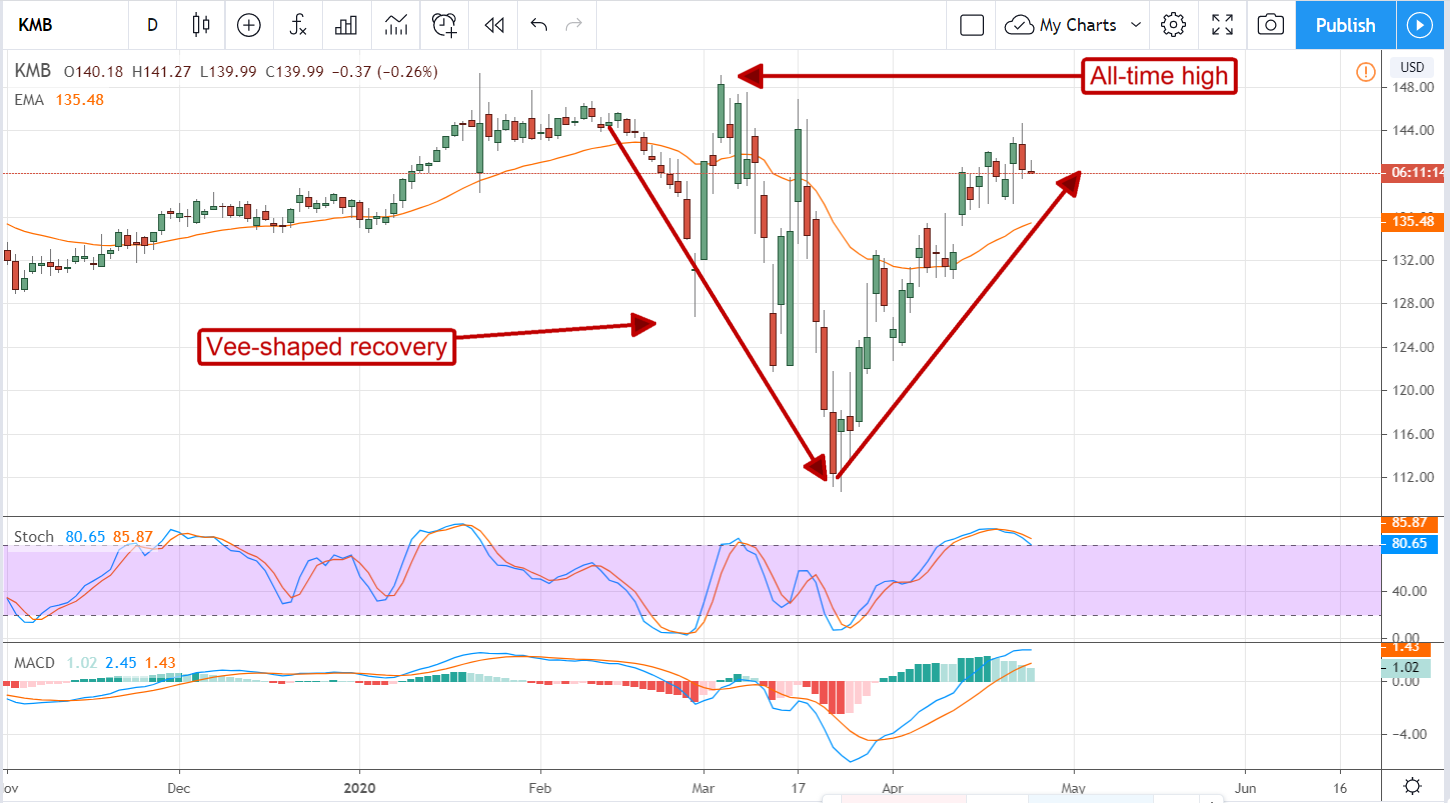

The Technical Outlook: A Vee-Shaped Recovery For This High-Yield Dividend Payer

To quickly touch base on Kimberly-Clark’s dividend, the dividend is attractive and safe. The company is a prince of dividend payers with 47 years of regular distribution increases. While not enough to declare this stock a Dividend King it is enough to alleviate most fears the payment will be affected by the pandemic. After 47 years, Kimberly-Clark has proven its ability to manage the business and the dividend. Those factors, the market-beating 3.05% yield and the safety of the payment, coupled with this year’s results should be enough to drive this stock to a new high.

Looking at the charts, Kimberly-Clark is in the process of forming a very nice Vee-shaped bottom. The stock still has resistance to overcome but, once done, the path to new all-time highs will be clear. Resistance is at the $144 level and will likely be tested within the next few trading days. If the market fails to overcome resistance investors should expect price action to fall back and retest for support along the short-term moving average. Longer-term, I expect the analysts to continue warming to this stock and, when they do, fuel the rally to new all-time highs.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Looking to profit from the electric vehicle mega-trend? Enter your email address and we'll send you our list of which EV stocks show the most long-term potential.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.