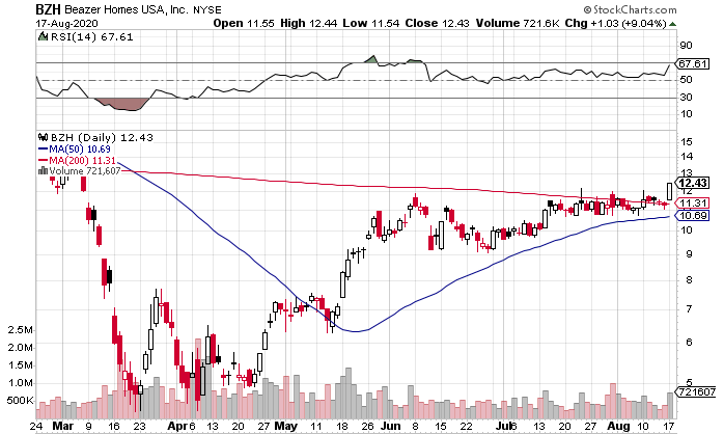

After basing for two-and-a-half months,

Beazer Homes NYSE: BZH broke out on above-average volume yesterday. Shares of the homebuilder bounced between $9 and $12 a share between early June and mid-July. But the price action tightened over the past month, with shares stuck between the high-$10s and the low-$12s. Over this period, volume also dried up.

The breakout came on above-average volume, particularly compared with the past two-and-a-half months. Furthermore, shares closed just a penny shy of yesterday’s highs and the breakout took shares firmly above the 200-day moving average, where they had stalled out previously.

But Beazer Homes offers more than just a pretty chart. Its also trades at an attractive multiple in a hot industry.

Builder Confidence at Highest Level in 35-year History

According to the National Association of Home Builders/Wells Fargo Housing Market Index, builder confidence in the newly built, single-family home market jumped 6 points to 78 in August.

The index is now at the highest number in its 35-year history, matching the record level of December 1998. Back in April 2020, the index had plummeted all the way to 30, but it has quickly recovered as the work-from-home trend has led to a mass exodus to the suburbs.

Mortgage Rates Are At All-Time Lows

Mortgage rates are under 3% for the first time ever, providing another tailwind for homebuilding demand.

You have millions of millennials who are renting apartments in cities, and now seeing:

a) It’s a great time to buy a home with the low cost of borrowing.

b) The work-from-home trend appears sustainable and if they move out of the city, they likely won’t have to commute to the office every day in the future.

And in the case of interest rates, it’s hard to see rates shooting up any time soon. While sub-3% rates may not last for long, rates should remain at historically attractive levels for at least the next couple of years.

But Lumber Costs are High

NAHB Chairman Chuck Fowke had this to say on rising lumber costs:

“The V-shaped recovery for housing has produced a staggering increase for lumber prices, which have more than doubled since mid-April. Such cost increases could dampen momentum in the housing market this fall, despite historically low-interest rates.”

The cost increases have not just been due to increasing demand – but also decreasing supply. Many mills shut down in April and May due to the pandemic and did not expect to see the quick homebuilding recovery.

With all that said, the higher lumber prices seem temporary; they should fall back in line once suppliers have a chance to adjust to the higher demand.

Beazer is Coming Off a Strong Q3 2020

Beazer recently reported results for the period ending June 30, 2020 (Q3 for Beazer).

Here are some of the highlights:

- Homebuilding revenue increased 10% yoy to $532.5 million, with closings up 8% and ASP up 3%.

- Adjusted EBITDA increased 40% yoy to $54 million.

- Beazer’s June sales pace was its best in a decade.

- Guidance calls for adjusted EBITDA to be up 5-10% yoy for the full-year fiscal 2020.

Very Reasonable Valuation

Beazer is trading at around 9x projected 2020 earnings and around 10x projected 2021 earnings. It is trading at just .18x projected 2020 sales and .19x projected 2021 sales.

Furthermore, the company has recorded a total of just over $360 million in operating cash flow over the past eight quarters, an average of around $45 million per quarter.

Keep in mind – this is a company with a market-cap of under $400 million.

But It’s Not all Sunshine and Rainbows

The hot industry… The strong recent numbers… The impressive guidance… The high single-digit P/E.

It sounds too good to be true.

Well, here’s the issue with BZH:

It has a little over $1 billion in long-term debt.

However, the company is well-positioned to pay that debt off. On the Q3 earnings call, Vice President David Goldberg said, “We have no significant maturities until 2025 and our clearly defined deleveraging path includes $50 million term loan repayments in each of the next three years. After our upcoming September repayment, we will have just over $100 million remaining on our goal of bringing our total debt below $1 billion.”

And with over $400 million in liquidity, more than $150 million of unrestricted cash, and nothing outstanding on its revolver, Beazer shouldn’t have trouble satisfying its repayment obligations. And again, BZH has an excellent operational outlook.

Don’t Let the Debt Scare You

In a perfect world, Beazer would have less debt on the books. But if that were the case, it would be likely be trading at a substantially higher valuation.

Bottom line, Beazer is a screaming buy when you consider the strong fundamentals, hot industry, and bullish price action.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Wondering what the next stocks will be that hit it big, with solid fundamentals? Enter your email address to see which stocks MarketBeat analysts could become the next blockbuster growth stocks.

Get This Free Report