Food and beverage maker Campbell Soup Company (NYSE: CPB) shares have been in decline since peaking out at height of the pandemic as the food stockpiling phenomenon surged demand. Shares appear to be setting up for a breakdown underperforming the benchmark S&P 500 index NYSEARCA: SPY. The advent of COVID-19 vaccines nearing FDA approval further hammers the proverbial nail in the coffin for its shares. While the Company has acknowledged that the pandemic panic buying demand of its products is an outlier, it has also taken the opportunity to invest in various growth drivers to offset the inevitable top-line reversion that’s coming. The results of the initiative could produce a higher “new normal” baseline unveiling a value situation for prudent investors to scoop up oversold shares at opportunistic pullback levels. The advent of further rollbacks is a potential heading into the winter months regardless of vaccine approvals.

Q4 FY 2020 Earnings Release

On Sept. 3, 2020, Campbell released its fiscal fourth-quarter 2020 results for the quarter ending July 2020. The Company reported an earnings-per-share (EPS) profit of $0.63 excluding non-recurring items versus consensus analyst estimates for a profit of $0.53, a $0.10 EPS beat. Revenues grew 4.2% year-over-year (YoY) to $2.11 billion beating analyst estimates for $2.07 billion for the quarter. Total soup growth was 52% YoY driven by 30% increase in consumption attributed to consumer behavior trends related to COVID-19 and retailers replenishing inventory levels. Household penetration improved by over 5% YoY gaining 6.4 million households across all demographics with continued gains in the Millennial consumers. Marketing expenses grew by over 112% YoY as the Company “disproportionately invested” in marketing messages to younger consumers underscoring new usage ideas and summer recipes.

Conference Call Takeaways

Campbell CEO, Mark Clouse, provided color behind the numbers. Organic sales, adjusted EBIT and adjusted EPS all grew by double-digits. Notably, organic sales rose 12% YoY. The Company sees an opportunity for further inventory replenishment in 1st half fiscal 2021, the critical soup season. Cost savings continued with $45 million in the quarter stemming from the Snacks integration. Marketing and COVID-19 expenses rose but helped drive adjust EPS growth by 50% to $0.63 per share. Concentration on household penetration and retention of new consumers and younger consumers has been a priority during the pandemic. Total household penetration rose 4% YoY with “strong sustained repeat of 71% of these new households.” Consumer behavior trends included quick scratch cooking, at-home dining, online shopping and continued focus on value in a challenging economic environment. Clouse summed it up perfectly, “regardless of the duration of COVID-19 environment, we expect to retain a sizable portion of these households driven by these sustained behaviors even as the environment normalizes over time.” The Company expects to come out of the pandemic in a stronger position as new consumers become aware of the brand and products.

Forward Guidance

COVID-19 uncertainty prohibited forecasting full-year fiscal 2021, but the Company provided Q1 fiscal 2021 EPS in the range of $0.88 to $0.92 versus $0.89 analyst estimates. Revenues are expected to grow 5% to 7% YoY to the $2.29 billion to $2.34 billion range versus $2.28 consensus analyst estimates. This caused shares to collapse from the $51s to $45s, where it has fluctuated in a five-point range for months. As the heavy soup months approach in the pandemic backdrop, prudent investors can monitor shares for opportunistic pullbacks to gain exposure during a shakeout.

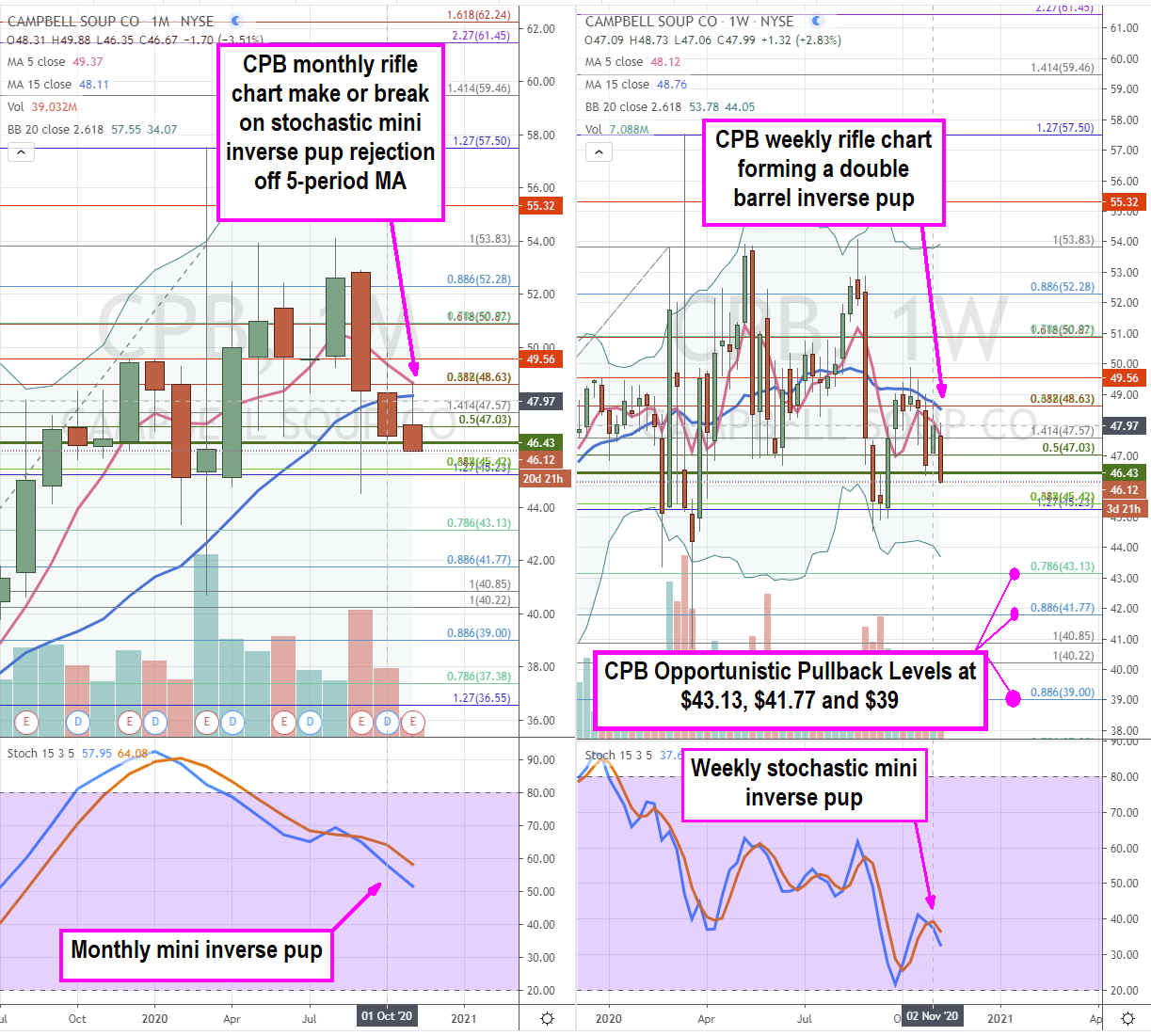

CPB Opportunistic Pullback Levels

Using the rifle charts on the monthly and weekly time frames provides a broader view of the landscape for CPB stock. The monthly rifle chart has a make or break turning into a potential breakdown on the stochastic mini inverse pup. This formed as shares rejected off the falling monthly 5-period moving average (MA) at the $48.63 Fibonacci (fib) level. Even uglier is the weekly rifle chart which is forming a double-barrel inverse pup breakdown comprised of the stochastic mini inverse pup and moving average inverse pup falling below the previous market structure low (MSL)buy trigger above the $46.43. Prudent investors can scale in at opportunistic pullback levels at the $43.13 fib, $41.77 fib and the $39 fib. Scaling in at these levels also makes the 4% to 5% annual dividend attractive for long-term investors. The advent of further rollbacks as COVID-19 cases rise is a potential catalyst for shares to coil off the bargain pullback levels.

Before you consider Campbell Soup, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Campbell Soup wasn't on the list.

While Campbell Soup currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Just getting into the stock market? These 10 simple stocks can help beginning investors build long-term wealth without knowing options, technicals, or other advanced strategies.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.