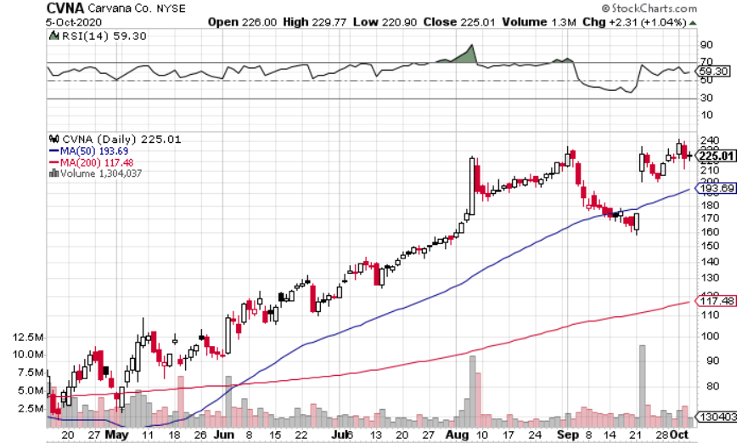

Back on September 2, I analyzed

Carvana NYSE: CVNA. At the time, it had just broken out to fresh all-time highs. While I liked the company,

I didn’t like the breakout for five reasons.

Well, as it happened, shares promptly plummeted by 30% in less than three weeks.

But then, right at the bottom, Carvana raised its Q3 guidance and shares got it all back – yes, all 30% – in one day.

CVNA’s price action since the gap-up has been strong, and shares look primed for another leg-up.

And that guidance that sent shares soaring?

A Record-Setting Quarter is in the Cards

Carvana said it expects to set several records in Q3: automobiles sold, revenue, gross profit per unit, and EBITDA.

The company is expecting break-even EBITDA, a welcome sight for a company that has recorded losses in every quarter since its IPO in 2017. Carvana reported an EBITDA loss of $69 million in Q2 2020.

Inspection Centers Give Way to Higher Capacity

Carvana’s biggest issue in Q2 was meeting elevated demand as the used car market has been hotter than expected.

Carvana – wisely, I might say, due to its debt and losses – took a conservative inventory management approach during the worst of the pandemic. The faster than anticipated recovery has forced Carvana to play catch-up.

On the Q2 call, CEO Ernie Garcia pointed out that inspection center capacity has been a constraint. But the company has taken steps to rectify the issue. Garcia said, “The facilities have a certain capacity, as we said, the nine that we have open now have nearly 500,000 units of facility capacity, but we have to staff those up to get access to that capacity. We'll open two more by the end of the year. That will add roughly an additional 100,000 units of facility capacity.”

Last month, I noted that Carvana had sold around 200,000 vehicles over the past four quarters, so the company should be good to go with 600,000 units of capacity.

At least for a little while…

Explosive Growth May Not Slow Anytime Soon

Amazon NASDAQ: AMZN… Tesla NASDAQ: TSLA… Carvana?

It might not be as far-fetched as it sounds. Carvana is an innovative and disruptive company and those are the types of companies that tend to see explosive revenue growth for longer than you expect.

Of course, the industry has to allow that growth. In Carvana’s case, its industry offers plenty of room for expansion. Piper Sandler Analyst Alexander Potter recently noted that, “Less than 1% of used car transactions take place online.”

That number is rising rapidly and it’s no wonder. In my last piece, I talked about how buying a used car is rarely a pleasant experience, but Carvana changes that.

And make no mistake about it: this is a massive market. There were 40 million used car transactions in the U.S. last year, totaling over $700 billion in sales. Carvana was responsible for less than one-half of one percent.

This is a highly fragmented market due to the nature of the brick-and-mortar used car business model. Carvana’s business model, on the other hand, is extremely scalable. Its long-term two million unit per year target may actually be a bit conservative.

The Verdict

It must be said: you’re going to need a strong stomach to buy-and-hold Carvana.

The September volatility was nothing new. After the company’s Q2 earnings report, shareholders endured a wild two days. Of course, shareholders ended up with a tidy net gain after those two days, but there were trying moments.

Carvana reports its Q3 earnings on November 6. I’d be surprised if shares surge as a record quarter is already priced in.

But you’re not buying Carvana in hopes of a 10% profit. You’re buying it in hopes that it turns into the next Amazon or Tesla and grows beyond belief. I think there’s a realistic chance that will happen. And if it does? You could be looking at a five or ten-bagger.

I’d focus on the big picture and look to get in sooner than later.

Before you consider Carvana, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Carvana wasn't on the list.

While Carvana currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Which stocks are hedge funds and endowments buying in today's market? Enter your email address and we'll send you MarketBeat's list of thirteen stocks that institutional investors are buying now.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.