After completing one of the deepest V-shaped moves in the market,

Crocs NASDAQ: CROX has been relatively quiet over the summer.

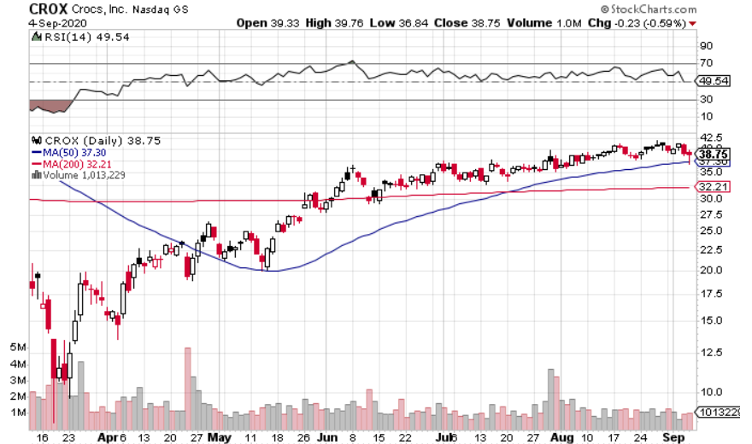

Shares mostly made higher highs and lower lows as the summer progressed, but the rate of increase was noticeably slower than it was in the spring. But with Crocs, that’s not a bad thing. After going from around $8 a share to $36 a share in less than three months, CROX needed to take a breather.

The Chart Says Buy

On Friday, Crocs shares bounced off the 50-day moving average, closing near the day’s highs.

CROX dipped – along with the rest of the market – on Thursday and Friday. The good news is that volume was light on both days for Crocs.

Looking longer-term, the 50-day moving average crossed over the 200-day moving average a month-and-a-half ago, a bullish sign.

Now is a good time to get into Crocs from a technical standpoint.

I liked the valuation on Crocs a little over two months ago. One earnings report and a 10% higher share price later – and I like it even more.

Q2 Was Better Than Expected

Q2 was, all things considered, a very solid quarter for Crocs, as the footwear company beat expectations and built on its past success.

Revenue was down 6% on a constant-currency basis to $331.5 million, but beat analyst estimates for $249.6 million. Adjusted earnings surged 71.2% to $1.01 per share, blowing away analyst estimates of 14 cents per share and the 59 cents per share reported in Q2 2019.

The revenue numbers, while down from a year-ago, look even better when you consider the industry’s Q2 performance. According to NPD group, footwear sales declined 26% yoy in Q2. Dress shoes fared even worse, declining 71% yoy. The pandemic has led customers to increasingly seek out comfortable shoes, though this shift had started prior to the pandemic.

Crocs’ foam clog shoes have been a beneficiary of the shift, and sales of them increased 10% yoy in Q2.

E-Commerce Sales Surged

Crocs’ e-commerce business grew 67.7% in Q2, marking Crocs’ 13th consecutive quarter of double-digit e-commerce growth.

E-commerce accounted for 56% of Crocs’ Q2 sales, up from 33% in Q2 2019.

Crocs’ management acknowledges that e-commerce may see a drop-off as its brick-and-mortar stores re-open – certainly as a percentage of sales – but the 13 consecutive quarters of double-digit growth show that Crocs’ e-commerce business isn’t solely benefiting from pandemic tailwinds.

It is built to last.

Asia Showed Improvement

Asia was Crocs’ weakest region in Q1 2020, with sales dipping 28.1% yoy.

In Q2, revenue still decreased in Asia, 21% yoy, but the decline was a significant improvement.

The improvement shouldn’t come as much of a surprise, as Crocs noted improving week-over-week sales in China and Korea on its Q1 earnings call. Those two countries saw revenue growth in Q2, though the increase was more than offset by declines in Japan, India, and much of Southeast Asia.

Crocs believes it can return to revenue growth in Asia in 2021.

Valuation Looks Even Better

Even though Crocs shares are a bit more expensive than they were a little over two months ago, the valuation is even more attractive due to an improving outlook. Crocs’ forward P/E is around 20 and the company should see both top and bottom line growth over each of the next two years – and perhaps beyond 46. Riley recently upgraded Crocs, boosting its price target from $35 to $46. I think shares have even more upside than that.

Crocs is a company that is doing fine under very difficult circumstances. Once the pandemic ends and things go back to normal, Crocs has big growth potential.

Low Downside

Earlier, I stated that CROX is a buy right now. If you get in, consider placing a stop-order just below Friday’s lows. That would give you a downside of around 5%.

The beauty with Crocs is you can combine a decent ceiling with a tight stop-order placed in a logical place – you’re not forced to draw an arbitrary line in the sand.

Before you consider Crocs, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Crocs wasn't on the list.

While Crocs currently has a Moderate Buy rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Almost everyone loves strong dividend-paying stocks, but high yields can signal danger. Discover 20 high-yield dividend stocks paying an unsustainably large percentage of their earnings. Enter your email to get this report and avoid a high-yield dividend trap.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.