Dick’s Beat Even The Market’s High Expectation

It was really no secret that Dick’s Sporting Goods (NYSE:DKS) was going to report a blowout quarter. The company is among a pantheon of retailers supported by COVID-related trends including stay-at-home, government stimulus, and eCommerce. While it was accepted the company would report a strong quarter and understood the figure would likely beat consensus there was still a question to be answered. Just how strong would Dicks’ results be?

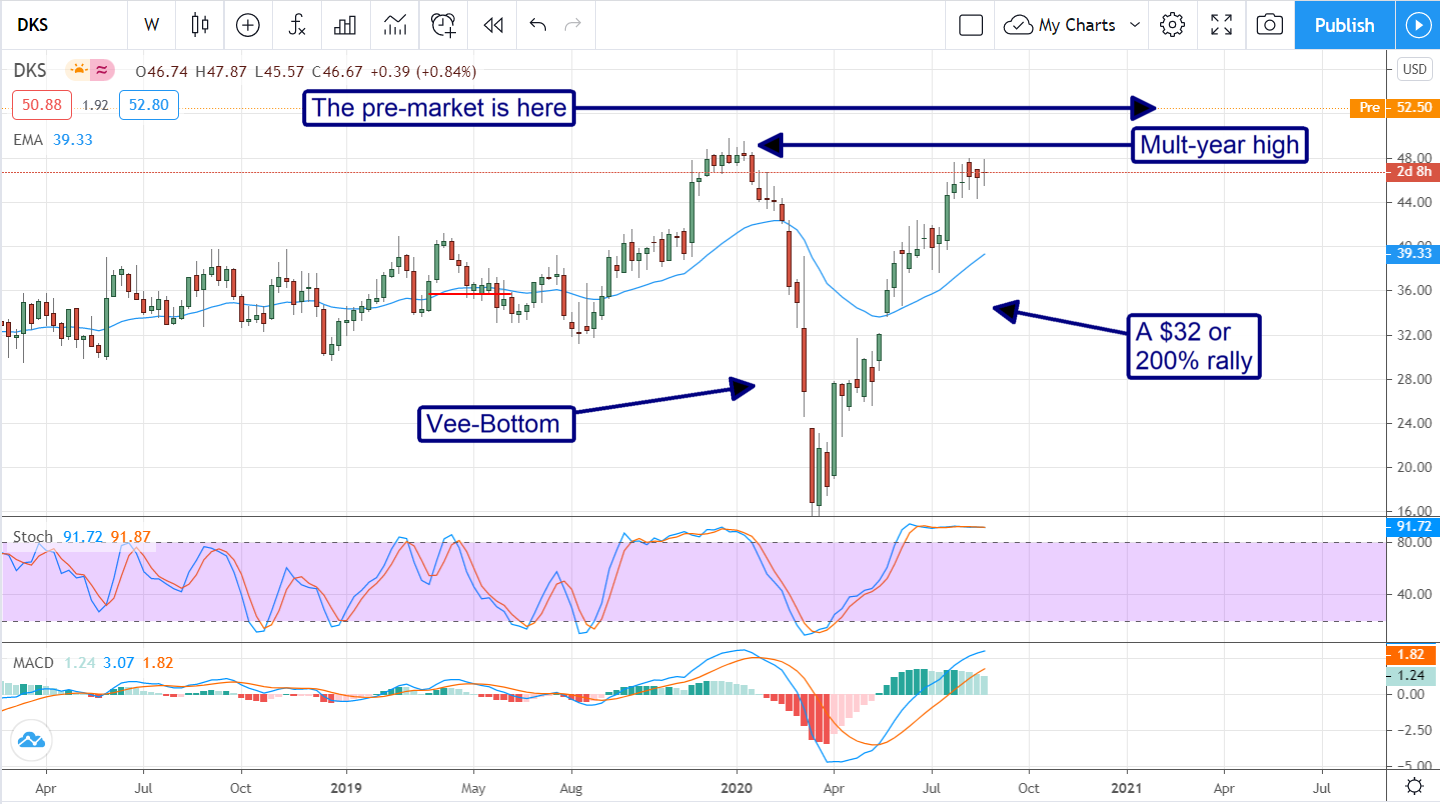

Well my friend, let me tell you. Dick’s Sporting Goods reported such a stunning quarter it sent shares skyrocketing. The company hit a home run that has shares breaking out of a Vee-bottom reversal to set a three-year high and this run is far from over.

Edward W. Stack, Chairman, and Chief Executive Officer said, "The favorable shifts in consumer demand that drove our strong comps during Q2 have continued into Q3 but have been partially offset by softness across key back-to-school categories because of the uncertain timing of a return to school and fall team sports. Taken together, through the first three weeks of Q3, our consolidated comp sales have increased by 11%, which demonstrates the strength of our diverse category portfolio."

Dick’s Reports A Smash Second Quarter

The top-line results are impressive to say the least. The company delivered 19.9% YOY topline growth on comps of 20.7%. To put this in perspective, the analysts had been expecting comps under 10%. Double the consensus is a big deal, it puts the entire year outlook into question again which means we’ll be seeing another burst of analysts chatter very soon. More impressive the bottom-line results. Both adjusted and GAAP earnings beat consensus by nearly $2.00 or more than 100%. Definitely enough to cancel out the 1st quarter loss.

"During this pandemic, the importance of health and fitness has accelerated and participation in socially distant, outdoor activities has increased. There has also been a greater shift toward athletic and active lifestyle products with people spending more time working and exercising at home," continued CEO Edward Stack.

The company’s strength lay in both its brick&mortar presence and eCommerce. The comps at brick&mortar locations increased double-digits while eCommerce surged nearly 200% YOY. In terms of net sales, eCommerce mored than doubled its contribution to the top-line growing from 12% last year to 30% of sales this year. I can say that I've used Dick's eCommerce services more than once over the past quarter.

The best news is that Dick’s did not suffer margin pressures related to the mix-shift like some other company’s have been reporting. In terms of margins, gross margin grew to 34.5% from 30% last year and operating margin to 14% from 6.2%. Both margins, needless to say, came in well above consensus.

Don’t Forget, Dick’s Sporting Goods Is A Dividend Grower

Investors shouldn’t forget that Dick’s Sporting Goods is a high-quality dividend payer with a robust outlook for future increases. Looking at the numbers, the payout ratio for the year is 38% of THIS QUARTER’s earnings. This puts them in good shape to pay and increase for the 9th consecutive time next spring. The company has some debt to be aware of but, as with the dividend payment, it is well in hand.

At the end of the quarter the company had over $1.1 billion cash, that’s up 10X from the same period last year, and there is no payments due. Inventories are down a bit from last year but only about 12% or $250 million so the company has ample liquidity to pay down some debt, improve the balance sheet, rebuild its inventory, and still have plenty of cash leftover.

Dick’s Is Breaking Out To New Highs, Double-Digit Gains Are In Store For Dicks

Dick’s second-quarter results and guidance for the 3rd has the stock breaking out of its Vee-bottom. In a technical sense, this is incredibly bullish due to the fact the Vee-bottom recovery was worth 200% gains for those trades savvy enough to buy at the bottom. Now that the company has proven its position in the new consumer paradigm it is poised to continue the rally with another possible $32 of upside or more.

My caution is this. The premarket action has prices gapping up to a three-year and trading right at a possible point of resistance. There is a good chance that, at least on an intraday basis, that prices will pull back to close the gap and/or find solid support before moving higher. That said, I would not expect too much from the pullback. If price action moves up from here I’d still be a buyer.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Like this article? Share it with a colleague.

Link copied to clipboard.