BREAKING: Uber has made an offer to buy food delivery company Grubhub

Restaurant delivery service GrubHub (NASDAQ: GRUB) found itself in a sweet spot with unprecedented demand stemming from isolation mandates and stay-at-home orders to curtail the spread of COVID-19. The conditions for such a dramatic shift in the food delivery landscape couldn’t have been predicted or even made up. With only takeout and delivery channels open to restaurants, food delivery services like GrubHub, DoorDash, Postmates and UberEats (NASDAQ: UBER) much be making out like proverbial “bandits”, right? That would be the narrative as a pandemic play, however, GrubHub’s most recent earnings results underwhelmed investors as the Company continues to lose money in the best-case scenario of a pandemic backdrop. If they can’t make money now, what happens when demand reverts back to “normal” as states ease isolation restrictions? Investors should consider selling into the bullish headwinds before reality hits home on shares of GRUB.

Rollercoaster Price Action

Coming into 2020, shares of GRUB had recovered from its disastrous Q3 2019 earnings report that that literally halved the shares from $60.31 to $32.11 in October 2019. Thanks to well placed “takeover” rumors, shares were able to squeeze to highs of $59.56 before peaking and further collapsing with the (-35%) plunge in the S&P 500 (NYSEARCA: SPY) amid the coronavirus pandemic in February 2020. GRUB bounced off the $29.50 Fibonacci (fib) level to form a weekly market structure low (MSL) trigger buy above $40.99 as heading into the Q1 2020 March earnings release.

Q1 2020 Earnings Takeaways

GRUB reported Q1 2020 earnings for the quarter ending in March, with breakeven EPS, which was + $0.03-per share better than consensus analyst estimates of (-$0.03)-per share. Revenues were $363 million versus the $359.76 million consensus analyst estimates, up 12.1% year-over-year (YoY). Active diners were 23.9 million versus 19.3 million, up 24% YoY. Daily average grubs (DAGs) were 516, 300, up 1% YoY. Gross food sales were $1.6 billion versus 1.5% YoY, up 8%. While nationwide isolation mandates weren’t widespread until March, the results were pretty underwhelming. The Company did note that business top-line acceleration happened near the end of Q1 heading into Q2. However, revenue surge was offset by additional expenses seen as a reinvestment into the brand relationships by boosting rewards and restaurant relief promotions as well as distributing over 100,000 safety kits for its drivers. These initiatives helped stimulate over $150 million in food sales for partner restaurants in the quarter. However, instead of building good will, the “fine print” in the GRUB’s relief program reads more like a hollow PR gimmick leaving a bad taste in the mouths of consumers and restaurant partners.

Behind GrubHub’s $100 Million Commission Deferment PR Gimmick

GRUB announced it would defer collection of up to $100 million in commissions to provide financial relief for independent restaurants in its network. What comes off a charitable voluntary initiative in “collaboration” with mayors of various cities, reads like a payday loan in fine print. Restaurants that apply are only granted a deferment on marketing commission fees, which exclude delivery and processing fees. While the total commissions and fees can range upwards of 33% of the order receipt (IE: 20% marketing, 10% deliver, 3.05% + $0.30 processing), how much of the marketing fee is deferred is ambiguous. Restaurants that accept deferment must also agree to at least a one-year platform agreement. The deferment is only a short-term suspension of fees during a relief period ending March 29th, at which point collection efforts begin two-weeks after the conclusion of the relief period. Seriously? Competitor DoorDash took the opportunity to offer a 30-day commission-free delivery period for new restaurants and discounting existing restaurants on their subscription service. UberEats waived delivery fee for customers taking a jab at GrubHub’s insistence that emergency delivery fee caps would end up costing consumers an extra $5-to-$10 per delivery if passed.

Emergency Delivery Fee Caps

GRUB blamed the emergency legislation enacted in San Francisco, Seattle and a handful of other jurisdictions that placed a delivery fee cap for restaurants for an uncertain climate. In Bay area, the emergency order placed a 15% fee cap delivery companies can charge restaurants during the COVID-19 pandemic.

The Best it Gets

The COVID-19 pandemic has caused a surge across all metrics, further accelerated with aggressive promotions like the $10 of $30 order deals. This growth will likely continue into Q2, but as geographies return to “normal” lifestyles, a reversion has to be expected. As with many of the pandemic plays, the revenue spikes are contained to the vacuum that undoubtedly will revert from “the best it gets” conditions. This is why shares of GRUB reacted to the release with an initial spike to $51.51 in after-hours only to sell-off to $43.26 the following day. Shares managed to rally back towards the monthly 5-period moving average (MA) resistance.

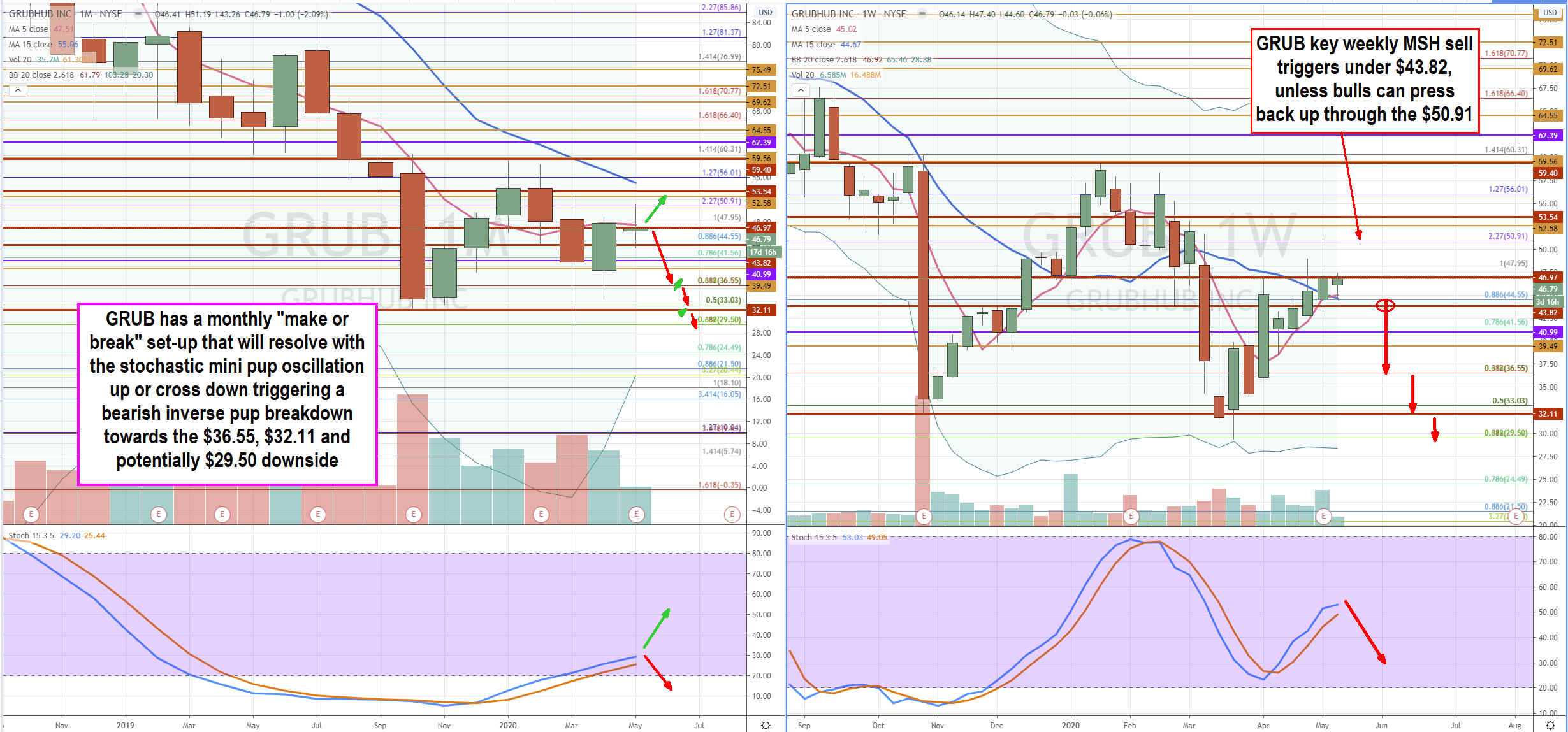

Bearish Trajectory Scenario

Using the rifle charts on a monthly and weekly time frame provides a broader view of the landscape for GRUB shares. The monthly chart is in a “make or break” composed of a rising stochastic versus a 5 and 15-pd MA downtrend. The resolution is determined by the crossover down on the stochastic oscillator triggering an inverse pup breakdown or a continued rising stochastic towards 80-band that crosses the 5-period MA up through the 15-pd MA reversing the trend into an uptrend. The weekly rifle chart is attempting a bullish stochastic mini pup but having problems breaking the $47.95 fib overlapped with the monthly 5-pd MA. If the weekly candle closes under the $44.55 fib, then a potential market structure high can trigger under the $43.82 level, which sets up a downward trajectory towards the $36.55 fib, $33.03 fib and $29.50 fib. The caveat would be if the bulls were able to squeeze GRUB back up through the prior weekly candle high above $50.91 fib. Otherwise, investors should consider using the $45 to $50 range to trim exposure but be aware of the trap door potential collapse under $43.82 and keep stops in place utilizing the aforementioned trajectories.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Looking for the next FAANG stock before everyone has heard about it? Enter your email address to see which stocks MarketBeat analysts think might become the next trillion dollar tech company.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.