Starting a 401(k), cultivating an investment strategy that balances risk and reward and taking advantage of corporate incentives to save are all ways to "catch up" on the road to retirement at 40. Read on to learn how to invest for retirement at age 40 when you have little to no investments.

Can You Still Save Enough for Retirement?

Before considering if saving enough for retirement at age 40 is possible, define what "enough" is. As a general rule, retirement experts recommend that you have "eight to 10 times your salary available to you once you enter retirement," according to a report by CBS News. If you earn an annual household income of $70,000, you'll want between $560,000 and $700,000 in combined investments, cash and assets to retire comfortably.

Many investors set out to save for retirement with the idea that they must accumulate $1 million before they retire. Is it possible to retire a millionaire when you have no retirement savings at 40?

While retiring a millionaire is possible when you begin investing at 40, it may require a more aggressive investment strategy.

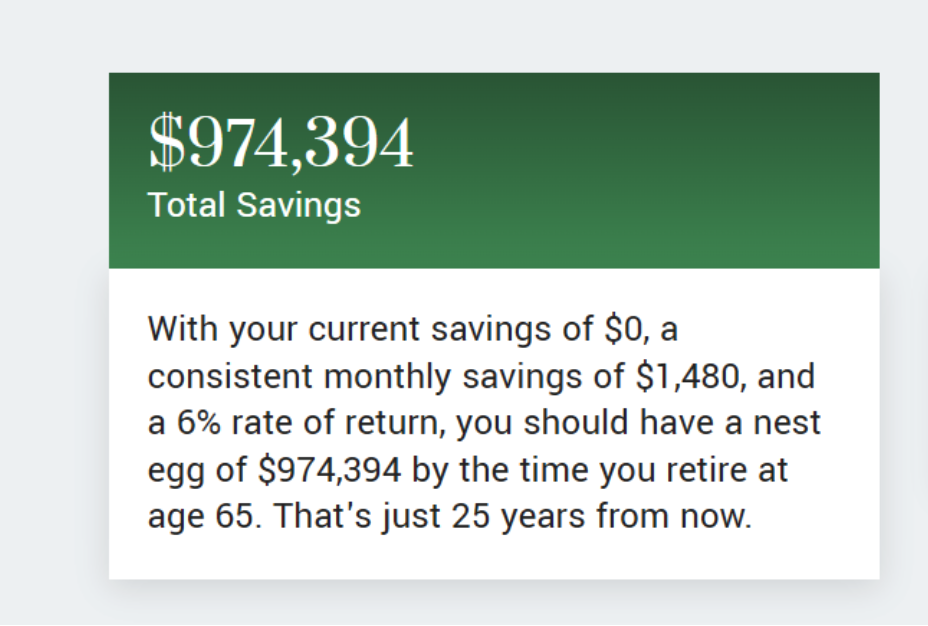

For example, a 40-year-old with $0 in investments would need to consistently invest $1,800 each month in an investment vehicle that returned an average of 6% annually to retire at 65 with $1 million in savings. Investing less than $1,500 per month in the same vehicle makes it impossible to retire a millionaire, showcasing the importance of investing as early as possible.

Thankfully, you may not need to be a millionaire to retire comfortably, especially if you plan to work past age 65 or live in an area with a lower cost of living.

Image: With $0 in savings, you'll need to invest at least $1,500 a month to retire as a millionaire.

Image: With $0 in savings, you'll need to invest at least $1,500 a month to retire as a millionaire.

How to Start Saving for Retirement at 40

While beginning retirement savings at 40 is more challenging than starting at a younger age, retiring is possible even if you begin investing late. However, to make up for the time factor, you must create a solid plan before you start. The following are crucial steps when deciding how to plan for retirement in your 40s with no savings.

Assess Your Retirement Goals and Financial Situation

Assessing your retirement goals and current financial situation are crucial first steps when starting retirement savings at 40. These two steps set the foundation for an achievable and realistic plan and show how aggressively you'll need to save to get there.

Begin by calculating your net worth, the difference between your total assets (savings, investments and property) and your liabilities (like debts and loans). Your net worth provides an overall snapshot of your current financial situation. Even if you don't have investments like stocks or ETFs, you could have pension funds, a bit of emergency savings or property that puts you in a better position than you originally thought.

Once you've compiled your holdings, compare them to your retirement goals and timeline. Consider current savings compared to your household income and spending, assuming you'll take about 4% of total retirement savings annually. This will give you an idea of how much you'll need to invest annually to meet your goals.

Build a Solid Retirement Investment Portfolio

After assessing your current retirement savings, consider how much you can invest annually. Think about when you would like to retire, how much you'll need to sustain your lifestyle given your savings and how much volatility you'll be able to withstand given your timeline to help you decide which assets to put your investment capital in.

Building a retirement investment portfolio involves considering many factors, especially if you currently have no savings at 40. MarketBeat's retirement calculator is an invaluable resource to determine how much you'll need to invest per month to meet your goals, which can guide your investment choice. For example, if you have more personal assets, you may want to select more conservative assets to help you meet your retirement goal.

Get Your Company Match

If your work offers a 401(k) match program that you're not taking advantage of, you could be leaving literal free money on the table. Corporate 401(k) matches are employer contributions made to an employee's 401(k) retirement account based on your contributions. Your employer will match your contribution to a percentage until you invest a specific percentage of your yearly salary.

For example, a common match structure is a 50% match on employee contributions up to 6% of their salary. In other words, if an employee contributes 6% of their salary to their 401(k), the employer will contribute an additional 3% of the employee's salary. This 3% comes from the employer's holdings and offers a free incentive to encourage you to save for retirement. Consult with your human resources department to learn more about if your company offers a 401(k) match, as starting a 401(k) at 40 can be an excellent first step toward retirement.

Get Out of High-Interest Debt

You may have a negative net worth if you have high-interest debt. In these circumstances, it's usually a good idea to devote extra income to debt repayment before investing, reducing interest payments' bleed on your investment capital. MarketBeat's guide to lowering four of the most common types of debt can be a great place to begin if you're in high-interest debt.

Diversify Your Retirement Investments

In investing, "diversification" refers to dividing capital between multiple assets and asset classes to reduce the risk of sudden loss. After you begin saving for retirement, consider branching out to multiple assets that match your risk tolerance level.

Image: ETFs like the Schwab International Equity ETF NYSE: SCHF provide instant diversification to your portfolio by investing in multiple assets.

Balancing Risk and Reward: Retirement Investment Strategies for 40-Year-Olds

When determining how to invest for retirement at 40, one of the first things you'll need to consider is the preservation of capital. Financial experts usually recommend saving for retirement early because more years in the market means more years to ride out periods of economic downturn. If you invest in highly volatile assets at age 40 and the overall market decreases in value, you may lose money because you withdraw before your assets can recover.

The specific assets that you invest in will determine your portfolio volatility. The following are the most common assets you can invest in through your retirement account, organized from least volatile to most.

- Bonds: Bonds are fixed-income producing assets that act as loans to local governments, corporations or federal entities. They are low-volatility assets because they have insurance from the entities that issue them. However, they also produce the lowest overall rate of returns.

- Mutual funds and ETFs: Mutual funds and exchange-traded funds (ETFs) are both investment vehicles made up of a "bundle" of other assets, including stocks, currencies, bonds and more. Funds usually track a particular index, which means assets included in the funds follow a particular "theme" — for example, stocks from small-cap companies, companies that produce consumer staples or international companies. Funds are less volatile than individual stocks because they divide risk between sometimes hundreds of companies.

- Stocks: A stock is an individual unit of ownership in a publicly traded company. Stocks represent a higher risk, able to compound returns and eliminate them in a short period. Forty-year-old investors should be wary of putting retirement funds into individual stocks, especially those issued by companies with less market history.

Image: Volatile stocks like Tesla Inc. NASDAQ: TSLA showcase the risk that 40-year-olds may take when buying shares.

As you invest for retirement, you'll create a diversified mix of assets like the ones listed above to balance risk and capital preservation.

How to Choose a Diversified Retirement Fund at 40

Now that you understand how to save for retirement in your 40s, it's time to dive into the market. Follow these basic steps to make your first buy toward retirement and start a plan for the future.

Step 1: Choose an investment account.

Before selecting assets, you'll need to open an investing account. The best account for your needs will vary depending on your employment status. To take advantage of a 401(k) match program, you'll typically need to open an account through your employer's broker. You'll also need to choose from your employer's pre-selected investment assets, which usually include bonds and mutual funds.

If you're exploring independent retirement options like IRAs, you have more freedom regarding where to open and what assets to invest in. For example, some IRAs allow you to invest in alternative assets like gold while taking advantage of tax benefits. Consider asset purchase freedom, fees and tax benefits before selecting a retirement account type.

Step 2: Explore available assets.

The account type you choose will dictate available assets. Explore your investment options and choose a few that match your risk tolerance level. If you're investing through an employer-sponsored account, your HR department can make recommendations from the broker's advising team.

Step 3: Place a buy and plan annual contributions.

After exploring your retirement account options, place a buy order. If you're working through an employer's 401(k), you can set automatic contributions to withdraw from your paychecks. If investing independently, you must link a bank account or other funding method before placing a buy order.

Plan how much you can contribute to your monthly and yearly retirement account according to account limits and employer match limits. If you can max out your 401(k) match, you may want to divert excess funds to another tax-advantaged account like an IRA.

Step 4: Continue contributions and monitor progress.

Continue contributing according to your plan and check on your progress, but don't get too obsessed with day-to-day movements. You can assess investment movements once a year, re-assessing asset allocation needs simultaneously.

Investing for Retirement at 40: It's Never Too Late

While the internet is full of anecdotes of individuals who were broke at 40 and a millionaire at 50, investors beginning saving at 40 should err on the side of caution when selecting assets. If you plan to retire at 65, investing at 40 will leave you with 25 years in the market compared to the 40 years a 25-year-old will have. Concentrating a larger percentage of your assets into low-cost mutual funds and ETFs may help you better preserve funds and retire on schedule.

FAQs

Ready to start saving for retirement? Get a few last-minute answers to common questions below.

What is the best investment at the age of 40?

The best investment at 40 will depend on your goals. Low-cost mutual funds can be a strong choice if you're like most 40-year-olds and are investing for retirement. If you already have retirement investments and you're focused on capital preservation, scaling down stock investments to bonds can help provide peace of mind as you approach retirement. Consulting with a financial planner or advisor is the best way to create an ideal asset mix for your situation.

How much should a 40-year-old have in retirement?

The general recommendation is that 40-year-olds should have about three times their household income in retirement savings. In other words, earning an annual household income of $65,000 means you should have about $195,000 in retirement savings by age 40.

How much should a 40-year-old have in investments?

You should have at least three times your household income's value in your total investments at age 40. If you have less than this, catch-up contributions and additional savings vehicles like IRAs can help you get closer to your retirement goal.

Before you consider Match Group, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Match Group wasn't on the list.

While Match Group currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.