Energy exploration and drilling company Helmerich and Payne NYSE: HP stock has been on a strong rally up 112% for 2022. The largest offshore driller in the U.S. is in the boom cycle with a perfect storm breakout for crude oil prices. The supply-demand constraints are expected to continue and provide a strong improvement in spot contracts. The Company is a benefactor in rising energy prices and supply chain disruptions as renewals will be at higher spot and term contract rates. The Russia-Ukraine conflict also contributed to the lasting spikes in oil prices. Inflationary pressures are also impacting margins. The Company expects to bolster contracts through $30,000 per day to garner 50% gross margins, which haven’t been seen since 2014. The industry is clearly rebounding, and H&P expects to lead the way forward with its automation and Flex Rig fleet solutions. Prudent investors looking for exposure in the drilling and exploration segment can watch for opportunistic pullbacks in shares of Helmerich and Payne.

Q2 2022 Earnings Release

On April 27, 2022, H&P released its fiscal Q2 2022 results for the quarter ending in March 2022. The Company reported an earnings per share (EPS) loss of (-$0.17) excluding non-recurring items, beating consensus analyst estimates for a loss of (-$0.26), by $0.09. Revenues grew 57.9% year-over-year (YoY) to $467.6 million beating $449.63 million consensus analyst estimates. North American Solutions ended the quarter with 171 active rigs, up 10%. North American Solution revenue per day increased 7% to $24,500 per day with additional increases expected. The Board of Directors approved a $0.25 dividend. H&P CEO John Lindsay commented, "During the quarter our active North America Solutions rig count increased in line with expectations and exited the quarter at 171 rigs. The industry rig count increase in the March quarter continued to shrink the availability of super-spec rigs that have worked at some point in the last two years, compounding the pre-existing supply-demand constraints in the market. As we have previously noted, the value proposition H&P brings to its customers through technology-driven efficiency and wellbore quality combined with the current market dynamics is accelerating improvements in contract economics. Like our customers, we expect to have disciplined capex spending, consistent with current industry trends, and as a consequence, the underlying supply-demand tightness will likely persist. We believe these conditions could provide a pathway to achieve significant improvement in average spot contract revenues.”

Conference Call Takeaways

CEO Lindsay stated that the Company will maintain CapEx budget discipline just like its customers which is crucial for long-term health and sustainability. The pre-existing supply-demand constraints were compounded as the super spec rig count shrank in March. The Company expects to peak at 176 rigs by fiscal Q4 while keeping the original CapEx budget range between $250 million to $272 million. H&P front-loaded its rig count in 2022 as it did in the previous year. Spot contract economics are rapidly improving towards an excess of $30,000 per day. The Company needs to get these rates to garner a 50% gross margin which were last seen in 2014. International markets remain positive at a slower pace. He elaborated, “In our South American operations, Argentina and Colombia remain focus areas and we have begun to contract additional rigs in those countries. In the Middle East, our strategy and opportunity sets are a bit different. We have delivered some of the flex rigs we sold at not drilling and are moving forward with the strong business alliances we established with them. We are also actively pursuing opportunities to export some of our idle super spec capacity into the region. In fact, we plan to start moving a rig into our Middle East hub during the second half of 2022. While we're optimistic about our strategy in the Middle East, we're also keenly aware that this is a long play, and it will take time for opportunities to emerge and fully develop.”

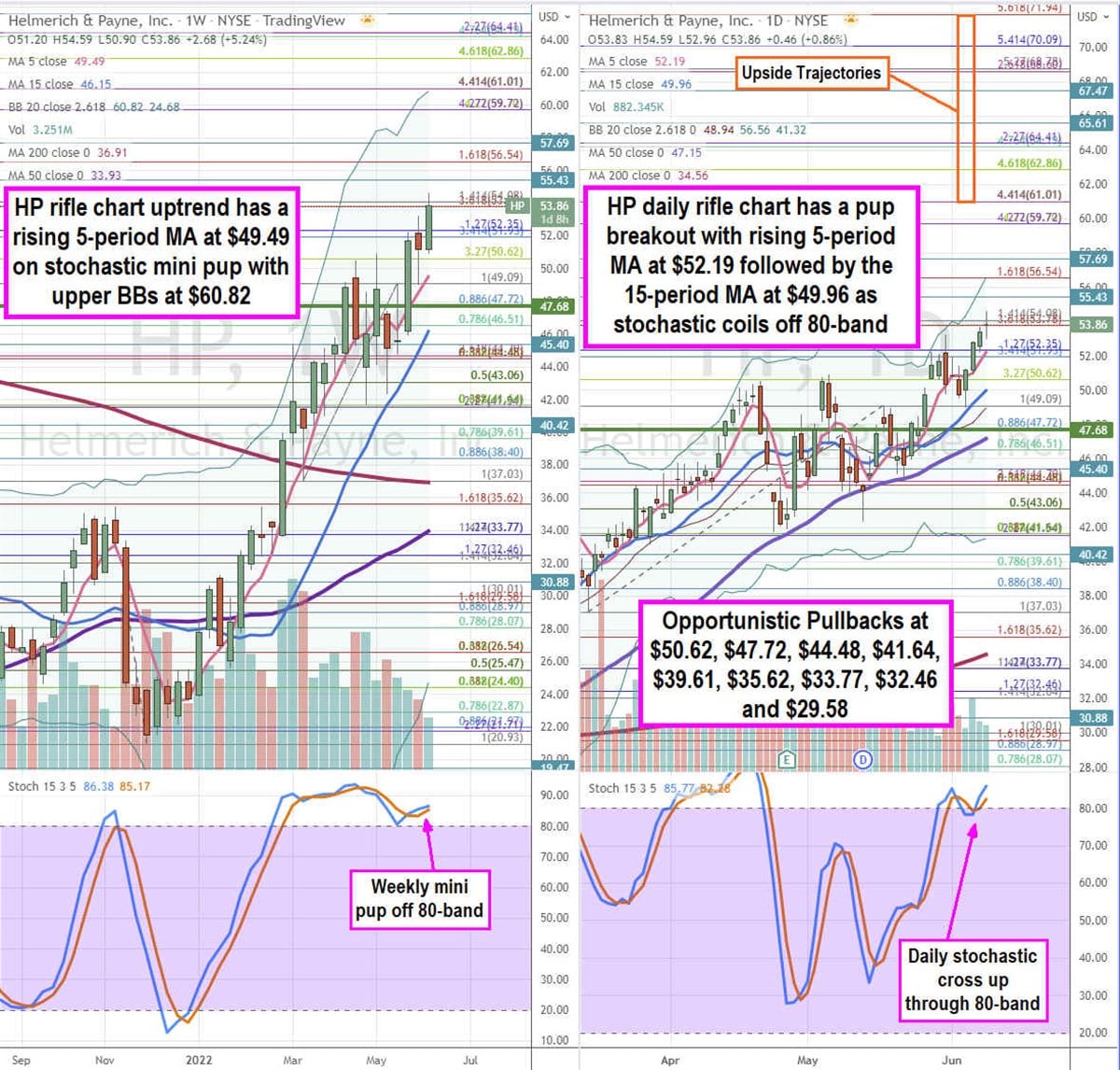

HP Opportunistic Pullback Levels

Using the rifle charts on weekly and daily time frames provides a precise view of the landscape for HP stock. The weekly rifle chart uptrend has a rising 5-period moving average (MA) support at $49.49 and a rising 15-period MA near the $46.51 Fibonacci (fib) level. The weekly stochastic cross-up off the 80-band. The daily 200-period MA support sits at $37.07 and weekly upper Bollinger Bands (BBs) at $60.82. The weekly market structure low (MSL) breakout triggered above the $47.68. The daily rifle chart pup breakout has a rising 5-period MA at $52.19 followed by the 15-period MA at $49.96 and 50-period MA at $47.15. The daily upper BBs sit at the $56.54 fib level and daily lower BBs sit at the $41.54 fib level. The daily stochastic crossed back up through the 80-band. Prudent investors shouldn’t chase entries and instead watch for opportunistic pullbacks at the $50.62 fib, $47.72 fib, $44.48 fib, $41.64 fib, $39.61 fib, $35.62 fib, $33.77 fib, $32.46 fib, and the $29.58 fib level. Upside trajectories range from the $61.01 fib level up to the $71.94 fib level.

Before you consider Helmerich & Payne, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and Helmerich & Payne wasn't on the list.

While Helmerich & Payne currently has a Hold rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

With the proliferation of data centers and electric vehicles, the electric grid will only get more strained. Download this report to learn how energy stocks can play a role in your portfolio as the global demand for energy continues to grow.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.