Let's take a deep dive into the factors that shape the investment potential of American Airlines by exploring industry dynamics, financial health, operational resilience and market sentiment to answer the question: Is American Airlines a good stock to buy?

Overview of American Airlines

Headquartered in Fort Worth, Texas, American Airlines Group Inc. NYSE: AAL (aka “American”) is a major U.S. airline that employs 130,000 team members around the world and carries more than 200 million passengers annually to over 350 destinations in 60 countries. American has undergone various mergers and expansions to become one of the biggest airlines in revenue and passenger miles flown, and its fleet is the largest in the world–comprising 953 mainline aircraft from Boeing and Airbus. The company has also been involved in ongoing efforts to modernize and streamline its operations.

American commenced trading on the New York Stock Exchange in 1939. In 1940, it was the first carrier to offer an invite-only private airline lounge, the Admiral's Club, at New York's LaGuardia Airport. The airline began offering trans-Atlantic service in 1945 and also created the first airline loyalty program called AAdvantage in 1981. American is a founding member of the Oneworld alliance, which allows it to collaborate with other major international carriers.

American’s main competitors are Delta Air Lines Inc. NYSE: DAL and United Airlines Holdings Inc. NYSE: UAL, and to a somewhat lesser degree, Alaska Air Group Inc. NYSE: ALK, JetBlue Airways Co. NYSE: JBLU, Southwest Airlines Co. NYSE: LUV, Spirit Airlines Inc. NYSE: SAVE and Air Canada NYSE: AC.

Latest American Airlines stock news

Asking yourself the question, “Should I buy American Airlines stock?” You must pay attention to the news.

After posting a loss of $545 million for Q3 2023 (the carrier’s first loss since the first quarter of 2022), American adjusted its profit forecast for the year to between $2.25 and $2.50 a share, down from the previous July estimate of $3 to $3.75. The airline blamed higher fuel prices and rising labor costs due to recent agreements with its unions to avoid strikes by pilots, flight attendants and ground workers.

These contracts, which will provide its employees with improved work rules, new benefits and pay raises, will cost the airline over $3 billion annually, with $1.8 billion going to pilots, $1.2 to flight attendants and $800,000 to ground workers. American anticipates breaking even during Q4.

On the positive side, along with its peers, American has been benefiting from a resurgence in travel demand after weathering a significant storm during the COVID-19 pandemic, which caused its revenues to fall as low as $17.33 billion in 2020 (from its 2019 revenue of $45.77).

In 2021, American saw an impressive 72.36% increase in revenue to $29.88 billion, then up another 63.88% to $48.97 billion in 2022. For the 12 months ending September 30, 2023, its revenue was $52.9 billion (a 17.04% increase year-over-year).

Challenges in the airline industry

The valuation of American Airlines Group Inc. is tied to the performance of the aviation industry as a whole, which faces numerous complex and dynamic challenges on an ongoing basis.

Intense competition

Every industry and business has its fair share of competition, but the battle among airlines (both legacy and low-cost carriers) is fierce, and the resulting price wars can squeeze profit margins.

Fuel Price volatility

Since fuel constitutes a significant portion of their operating costs, airlines are highly sensitive to fluctuations in oil prices, and sudden price spikes can significantly impact profitability.

Economic downturns

The airline industry is cyclical and tends to be affected by economic downturns. Business and leisure travel may decline during economic contractions, leading to lower demand for airline services.

Global events and crises

Pandemics, natural disasters, terrorist attacks and geopolitical tensions can severely impact the airline industry. We recently saw how devastating these effects can be when the COVID-19 lockdowns shut down airline travel for months, leading to catastrophic losses for airlines worldwide. In addition, government policies, trade tensions, and currency fluctuations can all affect an airline’s bottom line.

Regulatory challenges

The airline industry is heavily regulated by rules related to safety, security and environmental standards and failing to meet those standards will result in penalties and restrictions. In addition, any regulatory changes can impact operational costs and require substantial investments in compliance. For example, as emissions regulations become stricter, airlines are upgrading their fleets to cleaner and more fuel-efficient aircraft, and societal expectations for sustainability are causing a shift in overall business practices.

Capacity management

Balancing supply and demand is a constant challenge for many industries, and airlines are no exception, as overcapacity can lead to lower ticket prices and reduced profitability. At the same time, undercapacity may result in missed revenue opportunities.

Labor costs and unionization

Labor is a significant expenditure for airlines as it takes many people to keep things running smoothly. And, as American learned through its recent agreements, negotiations with labor unions can significantly impact operating expenses. But if an airline cannot keep the peace, its employees may strike, which would disrupt operations and lead to even greater financial losses in the long run.

High capital expenditure

Planes are expensive to purchase and maintain, and meeting safety and environmental standards often requires a good chunk of capital. Many airlines must take on debt to expand and upgrade their fleets.

Technology disruptions

While aircraft design and operations innovations can improve efficiency, disruptions like cybersecurity threats and technical glitches can pose risks. For example, in December 2022, a several-day computer outage at Southwest Airlines impacted over 16,000 flights. It cost the airline more than $800 million in refunds and compensation, and the company is still trying to recover from the resulting reputation fallout.

Customer expectations and experience

With the power of social media constantly growing stronger, an unhappy customer can instantly reach a large audience and affect overall company sentiment and confidence. As such, all companies, especially those in extremely competitive industries like airlines, must bring their customer service A-game daily.

This can look like additional customer service staff and training in conflict resolution, automation to facilitate faster responses to customer issues or providing more perks to ease the pain of travel disruptions or inconveniences.

Weather

Severe weather can cause flight delays and cancellations, translating to additional airline expenses in refunds, vouchers and/or reimbursements.

While American Airlines is a widely held and recognized company, it is not a blue chip stock. In general, American Airlines stock prices have been on a rollercoaster, and it hasn't been a great stock for long-term investors over the past decade as it has underperformed its peers and the benchmark S&P 500 index.

Even so, is AAL a good stock to buy now? To help you answer that question, let's take a look at American's financial breakdowns.

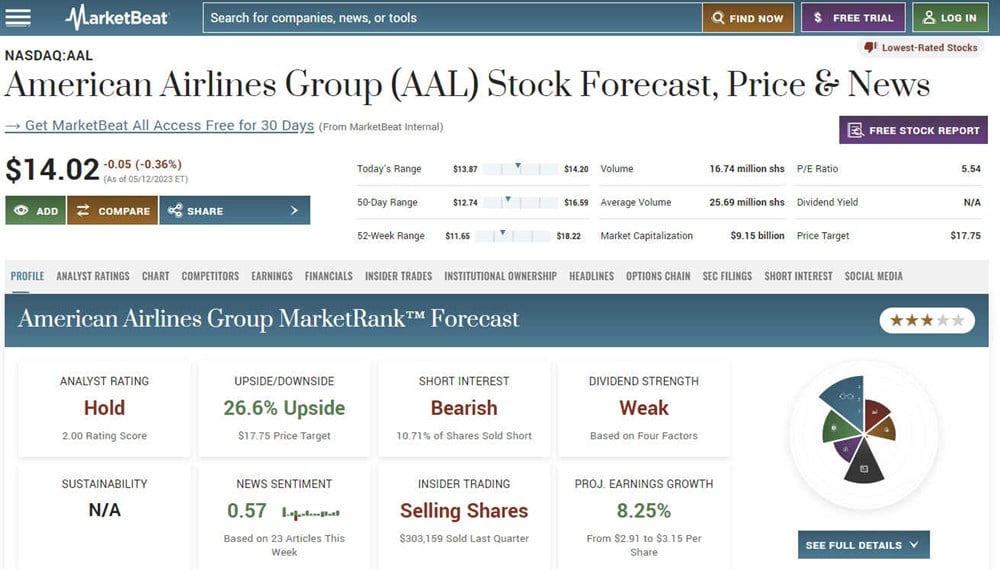

American Airlines Group Inc. NYSE: AAL was trading at $12.72 at the start of 2023, and as of November 30, its shares were trading at $12.23, making them down almost 1% YTD. The consensus rating for American stock is currently a "hold" according to 18 analysts. The average 12-month price prediction is $17.50, with a high price target of $29 and a low price target of $10.

The stock hit an all-time high of $59.34 in November 2006. Then, in March 2009, the global financial crisis and bear market decreased the price to a low of $2.50 per share.

American stock has significantly underperformed the S&P 500 benchmark index, which has a 10-year performance of 163.7%, as of December 29, 2023, compared to American's 10-year performance of down (44.15%) during the same period, with its lowest share price hitting $9.04 on March 15, 2020, just at the onset of the COVID-19 pandemic. The company's five-year performance is down (59.1%) and its one-year performance is up 1.4%.

Balance sheet

American Airlines had a weak but improving balance sheet by the end of 2023.

As of September 30, it had $65.7 billion in total assets and $70.8 billion in total liabilities, resulting in a net negative asset balance of $5.1 billion and a negative book value. The company expects 2023 free cash flows of $3 billion, which will be used moving forward to pay down a large portion of the debt. It has $10.6 billion in cash and short-term investments, $30.3 billion in operating property and equipment, $2 billion in accounts receivable and $29.7 billion in long-term debt.

Valuation

As of December 29, 2023, American Airlines stock is trading at the low range of its historical forward price/earnings (P/E) at 6.2 and price/sales (P/S) at 0.19.

Its weak balance sheet and high debt levels remove its valuation, but rising free cash flow can offset portions of the debt as it gets paid down. The MarketRank™ Forecast suggests a 27.3% upside price target of $17.50.

Future American Airlines outlook

American has ambitious plans: new CFO Devon May is on a mission to reduce the company's debt by $15 billion by 2025 through naturally occurring amortization and expected free cash flows. The company is off to a good start. By the end of September, American had already shrunk its debt levels by more than $10 billion from its peak in mid-2021.

The company doesn't have immediate problems with bond maturities as it hasn't ever defaulted on any of its debts. Its 6.5% senior secured notes, 9.25% senior secured notes and 11% senior secured notes, issued in 2022, are due in 2025. It has a Ba2 rating from Moody's and a BB rating from Fitch.

American — along with the entire airline industry — is eager to put the pandemic woes behind it. However, International Air Transport Association (IATA) director general Willie Walsh warns that capacity will be lower than anticipated due to a lack of parts availability and new plane delivery delays. He thinks that capacity will stay constrained until 2025 and may even be longer.

American has strongly emphasized ESG by investing in sustainable aviation fuel (SAF), which is cleaner burning and made from renewable resources, and incorporating new technology. Furthering this commitment, the airline has set another ambitious goal: to achieve net-zero greenhouse gas emissions by 2050.

Is AAL stock a buy or sell?

Now that you have read a comprehensive analysis of American Airlines, it should be easier to answer the question: AAL stock: buy or sell? But navigating these challenges requires strategic planning, operational efficiency, and adapting to external factors beyond airlines' control. Successful carriers often implement robust risk management strategies and stay agile in response to industry dynamics.

So, is American Airlines a good stock to buy now? Time will tell if American will be able to power through all the headwinds and come out profitable.

FAQs

To help you answer the question “Is AAL buy or sell?”, look at some frequently asked questions.

Is American Airlines a good investment now?

To answer this question, ask yourself if you could tolerate a 50% or more loss. Because while American Airlines is a well-known and widely held stock, it has vastly underperformed benchmark indexes like the S&P 500.

The cyclical nature of the airline industry, rising fuel prices, labor shortages, heavy sector competition and American's heavy debt load are all concerning–especially if you are seeking a stable growth stock or an income stock, as AAL doesn't pay dividends. It usually does not make the upgraded stocks list in the travel segment, nor will it become a meme stock mover.

If you bought AAL stock 10 years ago, you would still be down 26.25% compared to the S&P 500 index, which rose 152.9% (November 30, 2023). If you're a "glass is half full" investor, you may see this as upside potential and an excellent time to get into the stock. If you are more conservative, you may look at its historical stock price trend and not be willing to take the risk.

What are the best airline stocks to buy now?

Most airline stocks have predominantly underperformed the S&P 500, but American Airlines has been one of the worst performers, with a 10-year stock performance down 44.15% compared to the S&P 500, which was up 163.7%. During that same period, United Airlines was up 9.88%, Delta Air Lines was up 39.3%, Southwest Airlines was up 56.11% and Delta and Southwest pay a dividend. Although a consideration, it's important to remember that past performance does not indicate future returns.

What is the future of American Airlines stock?

American Airlines stock has been in a monthly descending triangle pattern, formed by connecting a diagonal trendline of the lower highs and a horizontal trendline of the flat bottom. AAL will break out of the triangle above its monthly 20-period exponential moving average (EMA) resistance at $15.62 to rise into the $20s range or break down through the $8.25 flat trendline bottom, falling towards the $5.50 range. Its earnings performance will be the primary catalyst in determining where the stock will go, whether toward an American Airlines buy or sell.

Before you consider American Airlines Group, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and American Airlines Group wasn't on the list.

While American Airlines Group currently has a "Hold" rating among analysts, top-rated analysts believe these five stocks are better buys.