Things Not So Sweet At Hershey?

Chocolate maker Hershey (HSY) reported earnings this morning and shares are down hard because of it. The company reported revenue and earnings below Wall Street consensus sending shares down 3.0% in the premarket session. The news, a surprise for this staple-oriented Dividend Aristocrat, raises the question, is it time to sell Hershey?

It Pays To Dig A Little Deeper

The headlines for Hershey read like the company is in trouble, revenue, and earnings missed on the top and bottom lines. The reality is that Hershey while falling short of the analyst’s estimates, produced positive organic growth for the quarter and saw revenues rise by 1.0%. The miss, a mere $50 million, is worth less than 2.5% of total revenue and a drop in the bucket for this cash-flow giant.

Total sales were up 1.0% for the quarter driven in part by acquisition and organic sales. Organic sales rose 0.5% for the quarter while the addition of ONE Brands added another 0.8%. The strength was aided by price-realization, 2.8%, and offset by currency headwinds and volume.

Along with price-realization, Hershey experienced a notable improvement in margin. Margins expanded by 90 basis points because of efficiencies and inventory build-ups in preparation for the pandemic-related economic shut-down.

The company acknowledges the impact of COVID-19 but says the damage is modest. Because the length and severity of the pandemic is still unknown management declined to forecast what the future might bring. Guidance for 2020 was pulled but the long-term outlook of sustained growth in the range of 2-4% with EPS growth in the range of 6-8% was reaffirmed.

“Due to the rapidly, evolving situation and the high degree of uncertainty, the company does not believe that it can estimate the full financial impacts with reasonable accuracy, and therefore believes it is prudent to withdraw fiscal 2020 full-year guidance at this time. The company believes it has sufficient liquidity to satisfy its cash needs, as supported by access to bank lines of credit and an unsecured revolving credit facility. The company reaffirms its long-term financial objectives of net sales growth in the range of 2% to 4% and an increase in earnings per share of 6% to 8%.”

The Outlook Is Unchanged For This Reliable Dividend Payer

Despite the Q1 revenue and earnings miss both measures grew from the previous year. While below the company’s long-term guidance the 0.9% revenue and 2.5% EPS growth is a far-cry better than the -15% expected for the average S&P 500 company. Looking forward, the analyst’s community is still expecting growth this year and next with both in-line with company guidance.

Why this matters is the dividend. Hershey is a Dividend Aristocrat with over 30 years of dividend increases so any deviation from expectation would be a big blow to investor confidence. Today’s news included several bits of information that, along with business results, should reassure the market.

First and foremost, Hershey declared its regular quarterly distribution as expected and unchanged. Along with it, the company says it is well-capitalized to withstand the pandemic. Looking at the balance sheet and capital ratios I agree. Hershey’s debt-load is small and well-managed, the company has plenty of cash and ample credit to carry it for several quarters should business conditions worsen.

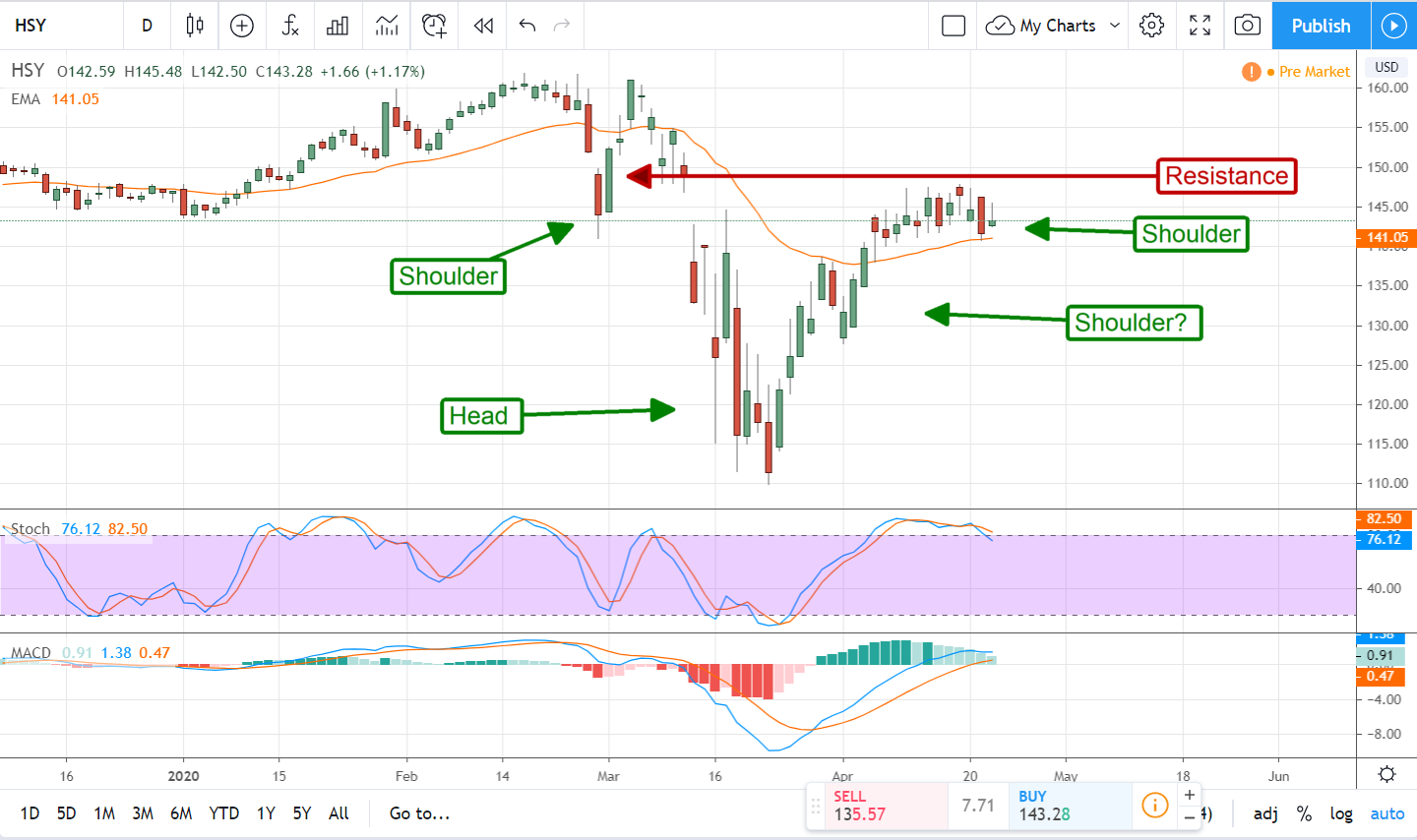

The Technical Outlook: Not Quite A Vee But A Recovery Is In Process

Over the past couple of weeks, I’ve spotted a number of Vee-shaped recoveries in-process. While not quite a Vee, this one is more like an exaggerated Head&Shoulders, there is recovery is in process. Hershey stock, after cratering more than 31%, has bounced back to reclaim most of its losses.

Price action has been consolidating above the short-term moving average which is a sign of bullishness. The indicators are bullish as well but there is a red flag, momentum is waning, and stochastic formed a bearish cross that signals resistance to higher prices.

Resistance is near the $146 level, consistent with a gap that formed during the panic-selling, and may keep prices from moving higher in the near-term. Patient investors may be able to get lower prices, possibly as low as $135 or $130. Longer-term, I believe the company’s strong cash position, the outlook for growth, and safe 2.0% yield are going to attract new buyers and drive this stock back up to retest the all-time high.

Before you make your next trade, you'll want to hear this.

MarketBeat keeps track of Wall Street's top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis.

Our team has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on... and none of the big name stocks were on the list.

They believe these five stocks are the five best companies for investors to buy now...

See The Five Stocks Here

Enter your email address and we'll send you MarketBeat's list of seven stocks and why their long-term outlooks are very promising.

Get This Free Report

Like this article? Share it with a colleague.

Link copied to clipboard.